PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043896

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043896

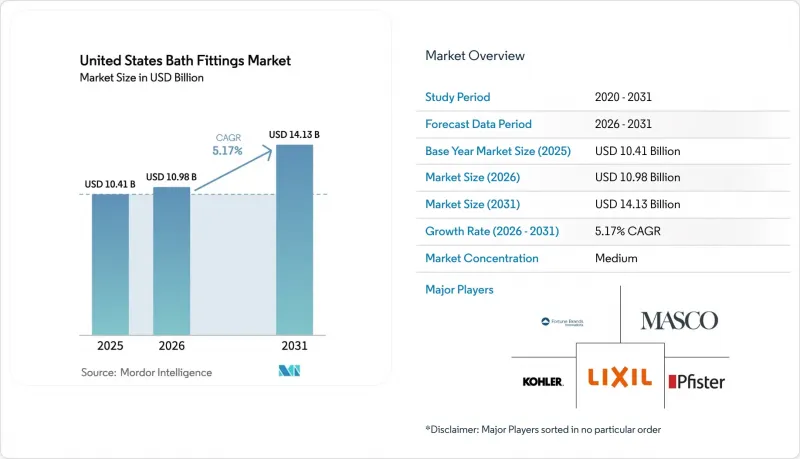

United States Bath Fittings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States bath fitting market size was valued at USD 10.41 billion in 2025 and estimated to grow from USD 10.98 billion in 2026 to reach USD 14.13 billion by 2031, at a CAGR of 5.17% during the forecast period 2026-2031.

The United States bath fitting market is supported by an aging housing stock that requires systematic fixture replacement, which keeps demand resilient even when construction cycles soften. Regulatory scrutiny also matters, as the EPA's draft WaterSense 2.0 specification proposed in December 2024 to lower lavatory faucet maximums from 1.5 to 1.2 GPM was paused in February 2025 for a consumer-choice review, adding uncertainty to product roadmaps while signaling further tightening ahead . State-level standards remain active, with California enforcing 1.8 GPM shower limits that catalyze early adopter replacement cycles and create product differentiation for adaptable flow configurations. Construction activity continues to shape installation volume, as 2025 housing starts of 1.36 million units and completions of 1.50 million units influence specification timing and the mix of fittings specified for multifamily and single-family deliveries .

United States Bath Fittings Market Trends and Insights

Remodeling and Replacement Cycle Sustains Faucet, Shower, and Fitting Upgrades

A large share of United States owner-occupied homes predates 1980, which means plumbing systems often face age-related leaks, corrosion, and compliance gaps that trigger steady replacement demand independent of new construction cycles. Even when interest rates were elevated in 2025, leading building-product manufacturers reported only a minor moderation in home improvement activity, which underscores the stickiness of functional bath upgrades anchored in safety, compliance, and water savings. EPA's 2014 lead-free thresholds and ongoing WaterSense labeling discipline have set clearer compliance baselines, nudging homeowners and contractors to prioritize certified fittings when tackling replacements. Local code enforcement at point-of-sale inspections, especially in jurisdictions emphasizing flow and backflow standards, further channels upgrade toward compliant faucet, shower, and valve assemblies. Utilities that combine leak notifications with rebates for efficient fixtures also shorten decision cycles for households sitting on aging plumbing, which supports a durable aftermarket for the United States bath fitting market across economic conditions. Together, these structural factors keep the United States bath fitting market well supplied with replacement-driven opportunities that are less sensitive to short-term changes in building permits.

New Residential Construction and Household Formation Bolster Bath Fitting Demand

United States housing starts totaled 1.36 million units in 2025, and completions reached 1.50 million, which supported a steady cadence of fixture installations across single-family and multifamily projects despite a mixed permitting backdrop. Within the mix, multifamily starts rose 16.6% year over year, while single-family starts contracted by 7.0% in 2025, which guided specification patterns toward mid-tier and code-forward products that are common in higher-density housing. Household formation momentum added 1.2 million net new households in 2024, which sustained baseline bath fitting requirements per unit across the new supply pipeline. Builders and developers increasingly specify WaterSense-labeled faucets and low-flow showerheads to meet certification objectives and unlock utility incentives, tightening the feedback loop between code ambition, rebate programs, and product selection in the United States bath fitting market. Category leaders also report growing sales of sustainable offerings that align with conservation codes and design expectations, which indicates that efficient fixtures continue to capture wallet share even when budgets are guarded. These dynamics, combined with localized distribution and inventory strategies, concentrate near-term upside in metro corridors with active multifamily pipelines and certification-linked project playbooks.

Skilled Labor Shortages and Installer Capacity Bottlenecks Delay Projects

Installer availability remains a pinch point across many metro areas, which stretches project timelines and pushes contractors to triage higher-margin jobs first. Capacity gaps delay discretionary upgrades and slow throughput in complex retrofits that require coordination among plumbers, electricians, and inspectors, which tempers the pace of premium fitting adoption in the United States bath fitting market. Manufacturers are engineering products to reduce install time and maintenance burden, such as self-powered faucets and flush platforms paired with gear-driven ceramic cartridges that outlast conventional solenoids in high-traffic settings. Brands are also investing in trade training and loyalty programs to increase installer proficiency and reduce callbacks, which helps with the smooth adoption of connected and code-intensive categories. As new product platforms integrate electronics and mixing technologies, field training and simplified connection architecture remain critical to overcoming labor bottlenecks and sustaining category growth.

Other drivers and restraints analyzed in the detailed report include:

- WaterSense and State Flow Standards Accelerate Efficient Retrofits

- Offline Retail and Showroom Coverage Supports Premium Upselling

- Strict Flow Caps Constrain High-Flow/Wellness Products in Drought States

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Faucets dominated with 32.71% of 2025 revenue, yet they are projected to grow at only 4.9% CAGR through 2031, while showerheads and systems are expected to advance at 6.54% CAGR over the same period. This mix reflects how the United States bath fitting market has pivoted toward wellness-oriented remodels and specification-grade commercial upgrades that favor multi-function showers and integrated valve controls. Homeowners and facility managers value digital presets, thermostatic safety, and consistent temperature delivery, which support upgrades beyond commodity faucet swaps in the United States bath fitting market. Smart shower controllers and water-saving modes are gaining visibility through design showcases and trade events, and the feature sets cater to both performance and conservation tendencies in water-stressed regions. Drainage and waste fittings are also part of the conversation as local codes encourage gray water readiness in some jurisdictions, which increases interest in compliant assemblies and installation practices for system-level efficiency.

System-level orchestration is reshaping how buyers evaluate bath solutions since coordinated suites across faucets, showers, and valves command higher attachment and streamline maintenance. Leading brands are extending ecosystem approaches to unify control, conserve water, and simplify installation, which helps differentiate offerings in mid-to-premium price bands in the United States bath fitting market. In commercial projects with strict hygiene and uptime requirements, touchless activation paired with thermostatic mixing creates safety and operational benefits that align with facility protocols. Because building owners often prefer predictable service intervals and standardized parts across floors or properties, comprehensive shower systems and matched faucet lines help compress service complexity and reduce stock-keeping units. As multi-function showers gain traction, faucet categories continue to refresh with sensor and voice-enabled options, but relative growth tilts toward configurations that deliver an integrated experience.

Chrome-plated brass captured 41.94% of the share in 2025, and while it remains cost-advantaged and familiar with installers, it is projected to trail stainless steel's 6.21% CAGR through 2031 as stainless gains from compliance and corrosion resistance advantages. Tighter enforcement of lead content thresholds under standards such as NSF/ANSI 372 has made stainless steel attractive for public projects and coastal installations, since it avoids dezincification concerns associated with some brass alloys in aggressive water conditions. In marine air or high-chloride municipal water, 316-grade stainless resists pitting and stress corrosion, which reduces warranty exposure and lifecycle costs for owners and operators. This performance edge aligns with the United States bath fitting market's drift toward durable, code-forward materials that satisfy both environmental and safety criteria under city and state rules.

Coating technologies are also advancing the appeal of premium metals, with PVD finishes extending scratch and tarnish resistance beyond standard electroplated chrome. That durability helps justify higher price points in commercial venues and upscale residential projects, where abrasion and cleaning chemicals can degrade lesser finishes. As fixture lifespans stretch under stricter water treatment and maintenance regimens, owners value material and finish integrity that preserves appearance and performance. Stainless steel's ability to bridge cost of ownership, compliance comfort, and aesthetic versatility positions it to keep taking incremental share within the United States bath fitting market over the forecast period .

The United States Bath Fitting Market Report is Segmented by Product Type (Faucets, Showerheads & Systems, Bathtub & Spa Fittings, Toilet Fittings, and Drainage Fittings), Material (Chrome-Plated Brass, Stainless Steel, Plastic, and Other Metals), End User (Residential, Commercial, and Institutional), Distribution Channel (B2C and B2B), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Fortune Brands Innovations (Moen, House of Rohl)

- Masco Corporation (Delta, Brizo, Peerless)

- Kohler Co.

- LIXIL (American Standard, Grohe)

- Pfister (ASSA ABLOY)

- Hansgrohe USA

- TOTO USA

- Sloan Valve Company

- Zurn Elkay Water Solutions

- Gerber Plumbing Fixtures (Globe Union)

- Chicago Faucets (Geberit)

- Symmons

- Speakman

- Bradley Corporation

- California Faucets

- Newport Brass (Brasstech)

- Kingston Brass

- Waterworks

- Watts Water Technologies

- Fluidmaster

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Remodeling and replacement cycle sustains faucet, shower, and fitting upgrades

- 4.2.2 New residential construction and household formation bolster bath fitting demand

- 4.2.3 WaterSense and state flow standards accelerate efficient retrofits

- 4.2.4 Offline retail and showroom coverage supports premium upselling

- 4.2.5 Legionella/scald risk management drives thermostatic mixing valves in institutions

- 4.2.6 Insurer-led leak-detection incentives expand smart shutoff adoption

- 4.3 Market Restraints

- 4.3.1 Skilled labor shortages and installer capacity bottlenecks delay projects

- 4.3.2 Strict flow caps constrain high-flow/wellness products in drought states

- 4.3.3 Patchwork compliance (federal, state, and standards) raises cost-to-serve

- 4.3.4 Weak existing-home sales and financing costs temper mid-market R&R

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Faucets

- 5.1.2 Showerheads & Systems

- 5.1.3 Bathtub & Spa Fittings

- 5.1.4 Toilet Fittings & Accessories

- 5.1.5 Drainage & Waste Fittings

- 5.2 By Material

- 5.2.1 Chrome-Plated Brass

- 5.2.2 Stainless Steel

- 5.2.3 Plastic (ABS, PVC)

- 5.2.4 Other Metals (Bronze, Copper)

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Institutional (Education, Government)

- 5.4 By Distribution Channel

- 5.4.1 B2C

- 5.4.1.1 Multibrand Stores

- 5.4.1.2 Exclusive Stores

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B (Direct & Project Sales)

- 5.4.1 B2C

- 5.5 By Geography

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 South

- 5.5.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Fortune Brands Innovations (Moen, House of Rohl)

- 6.4.2 Masco Corporation (Delta, Brizo, Peerless)

- 6.4.3 Kohler Co.

- 6.4.4 LIXIL (American Standard, Grohe)

- 6.4.5 Pfister (ASSA ABLOY)

- 6.4.6 Hansgrohe USA

- 6.4.7 TOTO USA

- 6.4.8 Sloan Valve Company

- 6.4.9 Zurn Elkay Water Solutions

- 6.4.10 Gerber Plumbing Fixtures (Globe Union)

- 6.4.11 Chicago Faucets (Geberit)

- 6.4.12 Symmons

- 6.4.13 Speakman

- 6.4.14 Bradley Corporation

- 6.4.15 California Faucets

- 6.4.16 Newport Brass (Brasstech)

- 6.4.17 Kingston Brass

- 6.4.18 Waterworks

- 6.4.19 Watts Water Technologies

- 6.4.20 Fluidmaster

7 Market Opportunities & Future Outlook

- 7.1 Touchless retrofits in K-12, higher-ed, and healthcare washrooms (hygiene + water savings)

- 7.2 Aging-in-place adaptations (thermostatic mixing, grab bars, anti-scald showers) in residential

- 7.3 Insurer-partnered leak detection and auto-shutoff bundles for high-loss ZIP codes