PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043907

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043907

Thailand Car Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

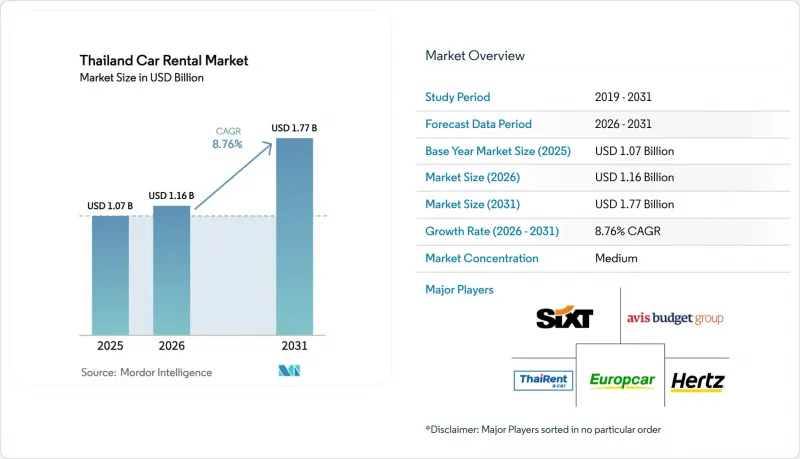

The Thailand car rental market size was valued at USD 1.07 billion in 2025 and is estimated to grow from USD 1.16 billion in 2026 to reach USD 1.77 billion by 2031, at a CAGR of 8.76% during the forecast period (2026-2031).

Sustained visa-free entry for major source markets, rapid expansion of low-cost carriers into secondary airports, and accelerated fleet electrification together underpin the long-run growth profile of the Thailand car rental market. At the same time, the sector faces near-term turbulence from a sharp fall in Chinese group tourism, tightening fleet-financing rules, and rising vehicle acquisition costs. Operators are therefore rebalancing toward domestic travelers and long-term corporate subscriptions, deploying digital booking platforms to capture price-sensitive demand, and adding battery electric vehicles (BEVs) to meet government sustainability incentives. Competitive intensity is rising as peer-to-peer platforms and ride-hailing-linked rental schemes squeeze traditional operators' margins and force them to invest in differentiated service models.

Thailand Car Rental Market Trends and Insights

Tourism Rebound & Visa-Free Schemes

Thailand's permanent visa-waiver for China, India, and Russia, introduced in 2025, removed a long-standing friction that deterred short-stay travelers. Chinese independent visitors recovered to over 75% of pre-pandemic levels in 2025, boosting multi-day car-hire demand beyond coach-based itineraries. Indian and Russian tourists accounted for around 4.4 million arrivals in 2025 and gravitated toward multi-destination road trips across beach and cultural circuits. The shift toward spontaneous, last-minute digital reservations rewards operators with real-time fleet visibility and flexible pick-up options.

Rise of Digital Booking & Price-Comparison Platforms

Digital booking apps such as Drivemate and Houpcar, along with aggregators embedded in super-apps like Grab and Traveloka, captured 63.16% of the Thailand car rental market transactions in 2025 and are growing at a 9.28% CAGR through 2031. Transparent price discovery pressures margins but vastly enlarges reach, prompting incumbents to integrate application programming interfaces (APIs) that feed real-time rates to multiple portals. Operators differentiate via doorstep delivery, bundled insurance, and loyalty perks, yet must streamline cost structures to remain competitive against asset-light digital platforms.

Rising Fleet Acquisition & Maintenance Costs

The 2026 excise-tax overhaul slashed BEV rates to 2% while lifting taxes on large ICE engines to 50%, inflating upfront prices for conventional cars and forcing rental firms to weigh accelerated electrification against capital constraints. Semiconductor shortages extend delivery lead times, prolonging fleet age and raising maintenance bills. New central-bank supervision of auto leasing since December 2025 has tightened credit standards, lifting borrowing costs for smaller operators. Balancing fiscal incentives with liquidity needs becomes critical for mid-tier companies.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Low-Cost Carriers to Secondary Airports

- Surge in Chinese Self-Drive Tourism

- Competition from Ride-Hailing and Super-Apps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Online reservations accounted for 63.16% of the Thailand car rental market size in 2025 and are projected to grow at a 9.28% CAGR through 2031, driven by metasearch engines and peer-to-peer listings that expose live prices across dozens of operators. Apps embed seamless e-wallet payments, one-click insurance, and user ratings, raising expectations for transparency and convenience. Offline desks still capture last-minute walk-ins at major airports, but their growth lags as mobile-first travelers favor the immediacy of smartphone bookings. Operators experiment with dynamic pricing and loyalty partnerships to retain direct-channel traffic amid aggressive aggregator discounting.

Thairung Group's acquisition of Drivemate and the immediate infusion of a BEV fleet validated the strategic pivot toward asset-light supply and digital discovery. Super-apps extend reach into food delivery and fintech ecosystems, converting everyday users into rental customers through cross-promotion. Elderly travelers and first-time visitors still value face-to-face service for complex insurance questions, sustaining a residual role for staffed counters. Nonetheless, digital share gains appear durable, underpinning automated check-out kiosks and contactless vehicle handovers in high-volume locations.

Short-term hires accounted for 71.26% of Thailand's car rental market share in 2025, driven by leisure-centric traffic at Bangkok, Phuket, and Chiang Mai airports. Daily rates remain the yield driver, yet seasonal volatility exposes cash flow to swings. In contrast, long-term rentals and monthly subscriptions bundled with maintenance and roadside support are set to grow at a 9.41% CAGR through 2031. Multinationals adopt pay-as-you-use fleets to hedge against ownership costs and align with sustainability mandates by swapping ICE units for BEVs.

Corporate accounts prize predictable budgeting and nationwide service coverage, pushing operators to offer fleet portals with usage analytics and centralized billing. Demand also stems from remote-work professionals choosing flexible car access over ownership. Subscription providers optimize asset utilization by redeploying idle corporate cars into weekend leisure pools, smoothing revenue seasonality. For traditional daily-rental players, entering long-term contracts requires re-engineering maintenance operations and credit-risk assessment frameworks.

The Thailand Car Rental Market Report is Segmented by Booking Type (Online and Offline), Rental Duration (Short-Term and Long-Term), Application (Leisure/Tourism and Commuting/Business), Vehicle Class (Economy and Mini, and More), Propulsion (Internal Combustion Engine and More), and Rental Channel (Airport and Downtown/Off-airport). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- The Hertz Corporation

- Thai Rent A Car

- Chic Car Rent

- Enterprise Holdings

- Sixt SE

- Drive Car Rental

- Q.C. Leasing (Thrifty)

- Siam Rent A Car

- Europcar Mobility Group

- Sunny Cars

- Bizcar Rental

- Avis Budget Group

- Budget Thailand

- National Car Rental

- Yesaway Car Rental

- ASAP Car Rental (K.B. Auto)

- Zuzuche

- Rent Connected

- EcoCar Rent

- ADA Car Rental

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tourism Rebound & Visa-Free Schemes

- 4.2.2 Rise of Digital Booking & Price-Comparison Platforms

- 4.2.3 Expansion of Low-Cost Carriers to Secondary Airports

- 4.2.4 Surge in Chinese Self-Drive Tourism

- 4.2.5 Government EV-Rental Purchase Incentive Programme

- 4.2.6 Blockchain-Based Deposit & Damage-Tracking Systems

- 4.3 Market Restraints

- 4.3.1 Rising Fleet Acquisition & Maintenance Costs

- 4.3.2 Competition From Ride-Hailing & Super-Apps

- 4.3.3 Stricter Fleet-Financing & Consumer-Loan Rules

- 4.3.4 Sparse Charging Infrastructure for EV Rentals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Booking Type

- 5.1.1 Online

- 5.1.2 Offline

- 5.2 By Rental Duration

- 5.2.1 Short-term

- 5.2.2 Long-term

- 5.3 By Application

- 5.3.1 Leisure / Tourism

- 5.3.2 Commuting / Business

- 5.4 By Vehicle Class

- 5.4.1 Economy & Mini

- 5.4.2 Compact & Mid-size

- 5.4.3 SUV & MPV

- 5.4.4 Luxury & Premium

- 5.5 By Propulsion

- 5.5.1 Internal-Combustion Engine (ICE)

- 5.5.2 Hybrid Electric Vehicle (HEV)

- 5.5.3 Battery Electric Vehicle (BEV)

- 5.6 By Rental Channel

- 5.6.1 Airport

- 5.6.2 Downtown / Off-airport

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 The Hertz Corporation

- 6.4.2 Thai Rent A Car

- 6.4.3 Chic Car Rent

- 6.4.4 Enterprise Holdings

- 6.4.5 Sixt SE

- 6.4.6 Drive Car Rental

- 6.4.7 Q.C. Leasing (Thrifty)

- 6.4.8 Siam Rent A Car

- 6.4.9 Europcar Mobility Group

- 6.4.10 Sunny Cars

- 6.4.11 Bizcar Rental

- 6.4.12 Avis Budget Group

- 6.4.13 Budget Thailand

- 6.4.14 National Car Rental

- 6.4.15 Yesaway Car Rental

- 6.4.16 ASAP Car Rental (K.B. Auto)

- 6.4.17 Zuzuche

- 6.4.18 Rent Connected

- 6.4.19 EcoCar Rent

- 6.4.20 ADA Car Rental

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment