PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043968

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043968

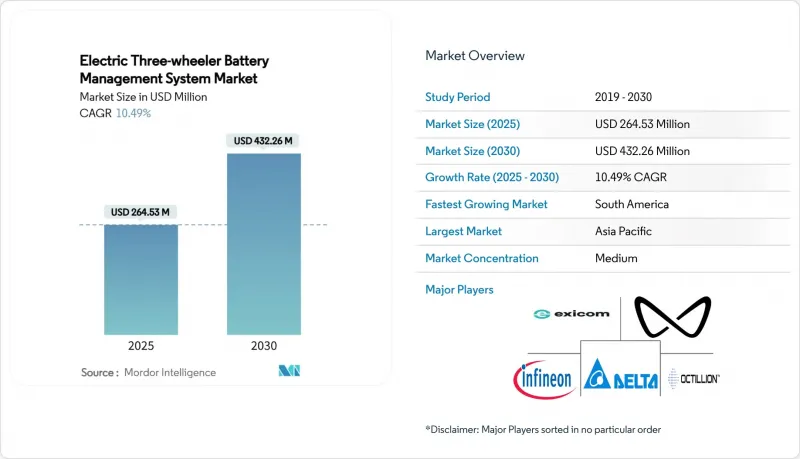

Electric Three-wheeler Battery Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Electric three-wheeler battery management system market size reached USD 264.53 million in 2025 and is forecast to advance at a 10.49% CAGR to USD 432.26 million by 2030.

Strong policy incentives, falling lithium-ion prices and the switch to wireless BMS architectures underpin this expansion of the Electric three-wheeler battery management system market. Wireless designs remove bulky harnesses, allow modular packs and cut assembly time, helping suppliers win orders from cost-sensitive three-wheeler manufacturers. Asia Pacific leads volumes, India's subsidy-driven penetration jump is decisive, while Brazil's pro-EV framework opens a fast-growth frontier. Integrated circuits consolidate functions on a single chip, and communication interface ICs grow quickest as edge-AI and over-the-air updates become mainstream in the Electric three-wheeler battery management system market. Competitive intensity rises because semiconductor giants, niche BMS specialists and AI start-ups all target wireless design wins.

Global Electric Three-wheeler Battery Management System Market Trends and Insights

Mainstream EV-Policy Push and Purchase Incentives

Government incentive structures fundamentally reshape three-wheeler electrification economics, with India's EMPS 2024 demonstrating how targeted subsidies accelerate BMS demand beyond organic market forces. Thailand's EV3.5 package exemplifies this trend, offering THB 25,000-100,000 subsidies based on battery capacity while mandating local assembly requirements favoring integrated BMS solutions. The policy framework creates artificial demand spikes that strain BMS supply chains while simultaneously driving standardization requirements. California's Zero Emission Vehicle program, targeting 35% of US EVs by 2030, establishes regulatory precedents that influence global three-wheeler adoption patterns, particularly in urban delivery applications with minimal range anxiety concerns.

Rapid Lithium-Ion Cost Decline and LFP Shift

Lithium Iron Phosphate battery costs approaching USD 85 per kWh enable three-wheeler total cost of ownership parity within 2 years, fundamentally altering BMS design priorities from cost optimization to performance differentiation. CATL's Shenxing PLUS technology, achieving 205 Wh/kg energy density with 4C charging capabilities, demonstrates how LFP chemistry advances eliminate traditional energy density disadvantages while maintaining thermal stability benefits crucial for tropical three-wheeler operations. The chemistry shift creates BMS differentiation opportunities through LFP-specific fuel gauging algorithms that address flat discharge curve challenges and hysteresis effects. Cost declines also enable secondary-life applications where retired three-wheeler batteries retain 70-80% capacity, creating new revenue streams for BMS providers who can manage degraded cell performance and safety monitoring in stationary storage applications.

Semiconductor Supply-Chain Volatility

Automotive-grade semiconductor shortages create cascading effects throughout BMS supply chains, with lead times extending beyond 52 weeks for specialized battery monitoring ICs that require ISO 26262 certification and automotive temperature range compliance. The volatility forces BMS manufacturers to maintain higher inventory levels, increasing working capital requirements while creating competitive advantages for vertically integrated suppliers with captive semiconductor capacity. Supply constraints also drive design-for-manufacturability initiatives where BMS architectures migrate toward commodity components and software-defined functionality to reduce dependence on specialized ICs. This shift creates opportunities for companies like Infineon and STMicroelectronics, which can provide integrated solutions combining power management, communication, and safety functions on single chips.

Other drivers and restraints analyzed in the detailed report include:

- OEM Migration to In-House Wireless BMS

- Standardization of CAN-FD protocols in India

- Cyber-Security Vulnerabilities in Low-Cost BMS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated Circuits maintain market leadership with 41.26% share in 2024, benefiting from the consolidation of multiple BMS functions onto single chips that reduce system complexity while improving reliability through reduced interconnections. Temperature Sensors and Fuel-Gauge devices experience steady demand growth driven by thermal management requirements in tropical climates and LFP-specific state-of-charge algorithms that address flat discharge curve challenges. Communication Interface ICs emerge as the fastest-growing component segment at 27.43% CAGR through 2030, reflecting the industry's migration toward wireless architectures and edge-AI capabilities that require sophisticated data processing and transmission functions.

The component landscape shifts toward system-on-chip solutions where traditional discrete components integrate into multifunctional ICs that combine battery monitoring, balancing, communication, and safety functions. Infineon's TLE9012DQU exemplifies this trend, providing comprehensive Li-ion battery monitoring and balancing capabilities in a single package optimized for automotive applications. Microcontrollers gain importance as BMS systems incorporate predictive algorithms and machine learning capabilities for battery health estimation and fault prediction. Cut-off FETs and Drivers maintain stable demand as safety-critical components that cannot be easily integrated due to power handling requirements and thermal considerations.

Centralized systems maintain a 38.17% share in 2024, while wireless cable-less topologies accelerate at a 31.08% CAGR, indicating a fundamental shift toward modular architectures that eliminate complex wiring harnesses while enabling flexible battery pack configurations. The wireless transition addresses key pain points in three-wheeler manufacturing where space constraints and cost pressures favor simplified assembly processes that reduce labor requirements and potential failure points. Distributed topologies serve niche applications requiring granular cell-level monitoring, while modular systems bridge the gap between centralized cost advantages and distributed flexibility benefits.

NXP's Ultra-Wideband wireless BMS demonstrates how advanced communication protocols overcome traditional wireless limitations, including interference susceptibility and latency concerns that previously restricted wireless adoption in safety-critical applications. The topology evolution creates competitive dynamics where traditional wired BMS providers must develop wireless capabilities or risk market share erosion to specialized wireless solution providers. Battery swapping applications particularly favor wireless topologies that enable rapid pack exchanges without connector wear concerns, supporting the growth of service-based mobility models where battery ownership separates from vehicle ownership.

The Electric Three-Wheeler Battery Management System Report is Segmented by Component (Integrated Circuits and More), Topology (Centralized, Modular, Distributed, and Wireless), Communication Technology (Wired CAN and More), Battery Chemistry (LFP, NMC, and Lead-Acid), Application (Passenger Carrier and More), Sales Channel (OEM-Fitted and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific dominated 2024 revenue with a 64.72% share as India's penetration rose from 5% to an expected 26-28% by fiscal 2026, catalysed by subsidy clarity and local-content rules. Domestic cell factories in Tamil Nadu and Gujarat secure supply and cut logistics costs, lowering pack prices by USD 12 kWh. China, even after an 8% dip to 320,000 units in 2023, remains the technology pacesetter. CATL's Shenxing PLUS and BYD's blade battery push global benchmarks, compelling regional BMS suppliers to upgrade thermal models or risk obsolescence.

North America and Europe show steady, policy-driven adoption. The US federal tax-credit debate injects uncertainty, but California's 35% ZEV target anchors demand. Fleets insist on ISO 26262 and ISO/SAE 21434 compliance, elevating cybersecurity and functional safety as ticket-to-play attributes. In Europe, the Battery Regulation enforces state-of-health reporting at each transaction, forcing cloud-linked BMS architectures. Circular-economy rules foster secondary-life revenue stacking that the Electric three-wheeler battery management system market increasingly internalises.

Middle East and Africa begin from a small base yet deploy electric delivery trikes for e-grocery ventures in Gulf cities. Government tenders bundle solar canopies with battery swapping, reducing grid stress. Temperature extremes demand derating algorithms that de-rate charge current above 45 °C ambient, a capability now standard on premium BMS firmware.

- Exicom Tele-Systems

- Delta Electronics Inc.

- Octillion Power Systems

- Infineon Technologies AG

- Mahindra Electric Mobility

- Piaggio Group

- Atul Auto Ltd.

- Kinetic Green Energy

- Saft (TotalEnergies)

- Trontek Batteries

- Lithium Balance A/S

- Sensata Technologies

- NXP Semiconductors

- Texas Instruments

- Renesas Electronics

- Panasonic Industry

- LG Energy Solution

- CATL

- Infineon Technologies

- BYD Co. Ltd.

- Bosch Mobility Solutions

- AVL List GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream EV-Policy Push and Purchase Incentives

- 4.2.2 Rapid Lithium-Ion Cost Decline and LFP Shift

- 4.2.3 OEM Migration to In-House Wireless BMS

- 4.2.4 Standardisation of CAN-FD Protocols in India

- 4.2.5 Edge-AI Prognostics for Swap-Ready Packs

- 4.2.6 Secondary-Life Battery Monetisation Models

- 4.3 Market Restraints

- 4.3.1 Semiconductor Supply-Chain Volatility

- 4.3.2 Limited Thermal Envelope in Tropical Use

- 4.3.3 Cyber-Security Vulnerabilities in Low-Cost BMS

- 4.3.4 Skills Gap in Tier-2 Retrofit Installers

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Component

- 5.1.1 Integrated Circuits

- 5.1.2 Cut-off FETs and Drivers

- 5.1.3 Temperature Sensors

- 5.1.4 Fuel-Gauge/Current-Measurement Devices

- 5.1.5 Microcontrollers

- 5.1.6 Communication Interface ICs

- 5.1.7 Other Components

- 5.2 By Topology

- 5.2.1 Centralized

- 5.2.2 Modular

- 5.2.3 Distributed

- 5.2.4 Wireless (Cable-less)

- 5.3 By Communication Technology

- 5.3.1 Wired CAN

- 5.3.2 Wired Ethernet

- 5.3.3 Wireless RF

- 5.4 By Battery Chemistry

- 5.4.1 LFP

- 5.4.2 NMC

- 5.4.3 Lead-acid

- 5.5 By Application

- 5.5.1 Passenger Carrier

- 5.5.2 Cargo/Load Carrier

- 5.6 By Sales Channel

- 5.6.1 OEM-fitted

- 5.6.2 Aftermarket/Retrofit

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Australia and New Zealand

- 5.7.4.6 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 South Africa

- 5.7.5.5 Egypt

- 5.7.5.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Exicom Tele-Systems

- 6.4.2 Delta Electronics Inc.

- 6.4.3 Octillion Power Systems

- 6.4.4 Infineon Technologies AG

- 6.4.5 Mahindra Electric Mobility

- 6.4.6 Piaggio Group

- 6.4.7 Atul Auto Ltd.

- 6.4.8 Kinetic Green Energy

- 6.4.9 Saft (TotalEnergies)

- 6.4.10 Trontek Batteries

- 6.4.11 Lithium Balance A/S

- 6.4.12 Sensata Technologies

- 6.4.13 NXP Semiconductors

- 6.4.14 Texas Instruments

- 6.4.15 Renesas Electronics

- 6.4.16 Panasonic Industry

- 6.4.17 LG Energy Solution

- 6.4.18 CATL

- 6.4.19 Infineon Technologies

- 6.4.20 BYD Co. Ltd.

- 6.4.21 Bosch Mobility Solutions

- 6.4.22 AVL List GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment