PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043983

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043983

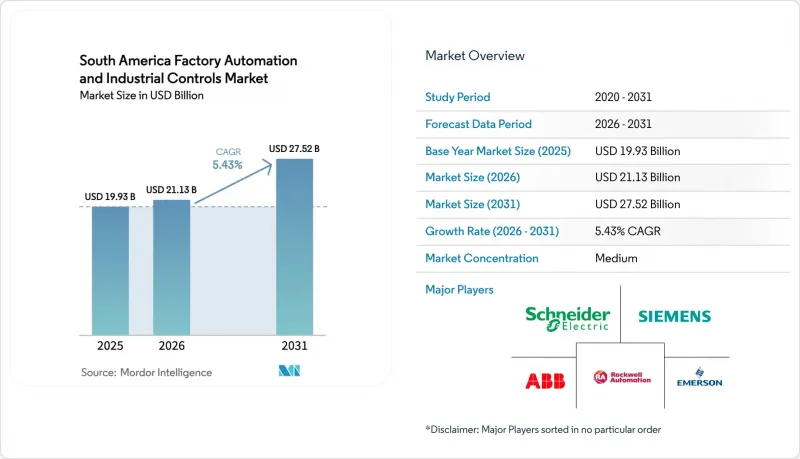

South America Factory Automation And Industrial Controls - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The South America Factory Automation And Industrial Controls Market size is expected to grow from USD 19.93 billion in 2025 to USD 21.13 billion in 2026 and is forecast to reach USD 27.52 billion by 2031 at 5.43% CAGR over 2026-2031.

Currency volatility and capital-expenditure caution among small and medium enterprises (SMEs) are muting headline growth, yet federal smart-factory grants in Brazil, rising near-shoring flows into Mexico, and export-driven pharmaceutical upgrades in Argentina are creating pockets of double-digit outlays. Vendors are pivoting from one-time hardware sales to outcome-based contracts that bundle predictive maintenance, managed cybersecurity, and remote commissioning. Cloud-native analytics and low-code orchestration are lowering the payback horizon for brownfield retrofits, while abundant renewable electricity in Brazil is attracting energy-intensive metals, pulp, and data-center projects that embed advanced process control from day one. Moderate competitive intensity, with the top five suppliers holding roughly 40% share, leaves room for regional specialists to win sector-specific deals in pulp-and-paper, mining, and chemicals.

South America Factory Automation And Industrial Controls Market Trends and Insights

Growing Adoption of Industry 4.0 and IIoT Ecosystems

Manufacturers are rolling out sensor networks, edge gateways, and cloud dashboards to close the visibility gap between shop-floor equipment and enterprise systems. Brazil's National IoT Plan subsidized connectivity hardware across 70 industrial parks in 2024, enabling real-time overall-equipment-effectiveness tracking. Mexico's tier-1 automotive suppliers added more than 12,000 IIoT endpoints during 2025 to satisfy just-in-time traceability rules. Argentina's pharmaceutical exporters deployed cold-chain sensors that meet World Health Organization pre-qualification, preventing batch losses after USD 22 million in temperature excursions during 2024. Chile's Codelco piloted low-latency wireless links for autonomous haulage, boosting ore recovery by 14% at El Teniente in 2025. These projects are accelerating demand for industrial Ethernet, 5G private networks, and edge compute that keep latency under ten milliseconds.

Government Incentives Accelerating Smart-Factory Investments

Tax credits, subsidized loans, and accelerated depreciation are compressing payback periods. Brazil's Nova Industria Brasil program earmarked BRL 300 billion (USD 60 billion) from 2024-2027, covering up to 40% of eligible automation spend. Argentina cut depreciation on control hardware to three tax years, unlocking USD 180 million in PLC and MES purchases during 2025. Colombia's Bancoldex extended USD 120 million in 4% loans for Industry 4.0 projects in 2025. Mexico's USMCA compliance rules now tie maquiladora tax benefits to proof of regional value content tracked by serialized HMI data. Such incentives are front-loading demand despite macro volatility.

High Upfront Capex and ROI Uncertainty for SMEs

SMEs supply 65% of manufacturing jobs yet account for only 28% of automation spend. Textile mills in Argentina postponed USD 95 million in PLC and vision upgrades during 2025 as peso depreciation distorted payback models. Vendors are countering with starter kits priced below USD 50,000 that bundle compact PLCs, HMIs, and six-month analytics subscriptions. Colombia's Bancoldex loans remain under-drawn because borrowers lack integration talent. Pay-per-use robotics in Mexican maquiladoras are easing balance-sheet stress, but contract complexity still deters late adopters.

Other drivers and restraints analyzed in the detailed report include:

- Cost-Pressure and Productivity Optimization Mandates

- Renewable-Power Advantages Attracting Power shoring to Brazil

- Severe Skilled-Labor Shortage for Advanced Automation Roles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial control systems accounted for 47.38% of the South America factory automation and industrial controls market share in 2025, anchoring large process plants. Yet software platforms are on course for a 7.32% CAGR and are projected to capture an expanded slice of the South America factory automation and industrial controls market size by 2031. Vendors are packaging low-code IIoT hubs, AI-driven predictive maintenance, and mobile HMIs that retrofit installed PLCs instead of replacing them. Machine-vision demand is climbing in automotive and pharmaceutical lines where zero-defect mandates prevail. Edge-ready 5G cores tested in Brazilian and Mexican factories during 2025 prove sub-ten-millisecond loop times, encouraging latency-sensitive closed-loop deployments.

Distributed control system incumbents, including Emerson's DeltaV and Honeywell's Experion, still dominate oil, gas, and chemicals but now offer modular configurations with 40% fewer engineering hours. PLC environments are migrating toward IEC 61131-3 compliance, easing cross-vendor code portability. MES and product lifecycle tools are merging, giving line engineers end-to-end digital threads. Mobile augmented-reality headsets that overlay maintenance steps are reducing mean-time-to-repair, especially in remote mines. As a result, the South America factory automation and industrial controls market is witnessing a shift in revenue mix from hardware to digital platforms without cannibalizing the core control install base.

Hardware represented 61.27% of 2025 revenue, yet replacement cycles are stretching from seven to ten years as predictive maintenance becomes mainstream. Services, however, are expanding at 8.07% CAGR, reflecting the appetite for remote diagnostics, cybersecurity patches, and performance guarantees that peg vendor revenue to asset uptime. The South America factory automation and industrial controls market size linked to services is widening as OEMs rebundle training, firmware, and analytics into subscription tiers.

ABB, Schneider Electric, and Siemens each added more than 1,200 regional service subscribers in 2025, while integrators such as Festo launched automation-as-a-service for SMEs, charging throughput-indexed fees that remove capex hurdles. Managed detection and response for operational-technology networks is emerging as its own category, spurred by a 47% rise in ransomware incidents targeting manufacturers during 2024-2025. Training centers in Sao Paulo and Mexico City graduated over 3,500 technicians last year, helping close, but not yet eliminate, the skills gap.

The South America Factory Automation and Industrial Controls Market Report is Segmented by Product Type (Industrial Control Systems, Field Devices, and More), Component Type (Hardware, Software, and More), End-User Industry (Automotive, Food and Beverages, and More), Deployment Mode (On-Premise, Cloud, and More), Enterprise Size (Large Enterprises, and SMEs), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Siemens AG

- ABB Ltd

- Rockwell Automation Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- General Electric Co.

- PTC Inc.

- Aveva Group

- Aspen Technology Inc.

- Bosch Rexroth AG

- Yokogawa Electric Corporation

- Omron Corporation

- FANUC Corporation

- Yaskawa Electric Corporation

- KUKA AG

- Festo SE and Co. KG

- Endress+Hauser Group Services AG

- WEG Industrias S.A.

- Danfoss A/S

- Beckhoff Automation GmbH & Co. KG

- Delta Electronics Inc.

- Advantech Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Industry 4.0 and IIoT Ecosystems

- 4.2.2 Government Incentives Accelerating Smart-Factory Investments

- 4.2.3 Cost-Pressure and Productivity Optimisation Mandates

- 4.2.4 Renewable-Power Advantages Attracting Powershoring to Brazil

- 4.2.5 Near-Shoring and Maquiladora Expansion Increasing Automation in Mexico

- 4.2.6 AI-Enabled Digital Twin Pilots Accelerating Brownfield Optimization

- 4.3 Market Restraints

- 4.3.1 High Upfront Capex and ROI Uncertainty for SMEs

- 4.3.2 Severe Skilled-Labor Shortage for Advanced Automation Roles

- 4.3.3 Local-Currency Volatility Causing Investment Deferral

- 4.3.4 Rising Cyber-Physical Attacks on Industrial Control Systems

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Industrial Control Systems

- 5.1.1.1 Distributed Control System (DCS)

- 5.1.1.2 Programmable Logic Controller (PLC)

- 5.1.1.3 Supervisory Control and Data Acquisition (SCADA)

- 5.1.1.4 Manufacturing Execution System (MES)

- 5.1.1.5 Product Lifecycle Management (PLM)

- 5.1.1.6 Human Machine Interface (HMI)

- 5.1.1.7 Enterprise Resource Planning (ERP)

- 5.1.2 Field Devices

- 5.1.2.1 Machine Vision

- 5.1.2.2 Industrial Robotics

- 5.1.2.3 Sensors and Transmitters

- 5.1.2.4 Motors and Drives

- 5.1.2.5 Relays and Switches

- 5.1.3 Automation Software Platforms

- 5.1.3.1 Edge and Cloud IIoT Platforms

- 5.1.3.2 AI-Powered Predictive Maintenance Suites

- 5.1.3.3 Low-Code Industrial Apps

- 5.1.4 Connectivity and Networking

- 5.1.4.1 Industrial Ethernet

- 5.1.4.2 5G Private Networks

- 5.1.4.3 Wireless Sensor Networks

- 5.1.1 Industrial Control Systems

- 5.2 By Component Type

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Food and Beverages

- 5.3.3 Oil and Gas

- 5.3.4 Chemical and Petrochemical

- 5.3.5 Power and Utilities

- 5.3.6 Pharmaceutical

- 5.3.7 Electronics and Electrical

- 5.3.8 Mining and Metals

- 5.3.9 Pulp and Paper

- 5.3.10 Other End-user Industries

- 5.4 By Deployment Mode

- 5.4.1 On-premise

- 5.4.2 Cloud

- 5.4.3 Hybrid

- 5.5 By Enterprise Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium Enterprises

- 5.6 By Country

- 5.6.1 Brazil

- 5.6.2 Mexico

- 5.6.3 Argentina

- 5.6.4 Chile

- 5.6.5 Colombia

- 5.6.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 ABB Ltd

- 6.4.3 Rockwell Automation Inc.

- 6.4.4 Schneider Electric SE

- 6.4.5 Emerson Electric Co.

- 6.4.6 Honeywell International Inc.

- 6.4.7 Mitsubishi Electric Corporation

- 6.4.8 General Electric Co.

- 6.4.9 PTC Inc.

- 6.4.10 Aveva Group

- 6.4.11 Aspen Technology Inc.

- 6.4.12 Bosch Rexroth AG

- 6.4.13 Yokogawa Electric Corporation

- 6.4.14 Omron Corporation

- 6.4.15 FANUC Corporation

- 6.4.16 Yaskawa Electric Corporation

- 6.4.17 KUKA AG

- 6.4.18 Festo SE and Co. KG

- 6.4.19 Endress+Hauser Group Services AG

- 6.4.20 WEG Industrias S.A.

- 6.4.21 Danfoss A/S

- 6.4.22 Beckhoff Automation GmbH & Co. KG

- 6.4.23 Delta Electronics Inc.

- 6.4.24 Advantech Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment