PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043987

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043987

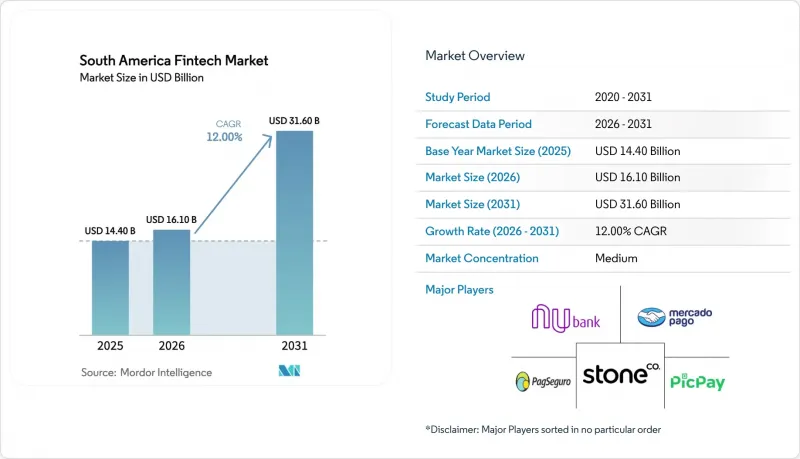

South America Fintech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The South America Fintech Market size is expected to grow from USD 14.40 billion in 2025 to USD 16.10 billion in 2026 and is forecast to reach USD 31.60 billion by 2031 at 12% CAGR over 2026-2031.

Digital payments led activity with a 45.0% share, while digital lending is set to expand at the fastest pace, with a 21.3% CAGR, as consumer credit and SME financing continue to scale. Retail users drove 68.6% of usage in 2025, and mobile applications accounted for 74.7% of interface interactions, underscoring a mobile-centric pathway for onboarding and engagement. Short-term headwinds persist from interchange caps, elevated interest rates, and FX controls that compress take rates and settlement economics, particularly in Brazil and Argentina. Competitive intensity is high as neobanks and embedded-finance platforms cross-sell credit, insurance, and investment products, illustrated by Nubank's 127 million customers and Mercado Pago's 72 million monthly active users across the region.

South America Fintech Market Trends and Insights

RTP Scale-Up and Features Propel Volume Growth

Real-time payments now anchor transaction growth across the South America fintech market, led by Brazil's Pix, which handled 63.4 billion transactions in 2024 as adoption approaches ubiquity among adults. Pix's 24/7 availability and rapid settlement underpinned a surge to 163 million registered users by late 2024, while new features such as Pix Automatico and contactless tap-to-pay expanded use cases for subscriptions and point-of-sale payments. Peru's interoperable rails, anchored by Yape and PLIN, support merchant acceptance in urban retail and micro-commerce. Early cross-border pilots linking Pix with neighboring markets are shortening settlement windows and reducing FX spreads for remittance and e-commerce corridors in the South America fintech market. Platform adoption has been reinforced by large ecosystems, with Mercado Pago enabling instant disbursements to its 72 million monthly active users and StoneCo reporting a 95% year-over-year increase in Pix transactions among MSMB clients in early 2025. Regulatory clarity supports scale, including Brazil's interoperability mandates and ongoing instant payment initiatives in Chile and Colombia for mid-2026 timelines, as well as enhanced KYC and biometric checks in response to elevated APP fraud reports.

Open Finance Data Portability Unlocks Credit and Advisory

Brazil's open finance system records more than 43 million active user consents and processes over 1.5 billion API calls weekly, placing it among the largest initiatives globally by transaction volume. Central bank directives require data sharing across transactional, credit, and investment domains for qualifying institutions, enabling third parties to price unsecured, payroll-linked, and secured credit using verified account and salary flows. Nubank's secured-lending portfolio rose 133% year over year in 2025, assisted by consented access to income and account data that tightened underwriting and collection performance. Chile's CMF issued General Rule No. 514 in July 2024 to require standardized APIs by July 2026, and Colombia published a draft decree in June 2025 to extend coverage beyond banking into insurance and pensions. Argentina's Executive Decree No. 353 of 2025 formalized an open finance system with BCRA oversight and consent-based data sharing, further lowering barriers to multi-product financial advice in the South America fintech market. Despite momentum, differing data field standards and nascent cross-border interoperability raise integration costs and complexity for smaller providers.

High Customer Acquisition Costs and Low Financial Literacy as Structural Growth Barriers

High customer acquisition costs, coupled with persistently low financial literacy across several South American markets, continue to constrain fintech scalability. Despite rapid digital adoption, consumer onboarding still requires significant marketing spend, offline verification, and education-driven engagement. This raises blended CAC and depresses lifetime value economics, particularly in underbanked and rural segments. The challenge is structural and long-duration, pushing fintechs to invest in financial education, agent-assisted onboarding, and data-led personalization to improve conversion and retention.

Other drivers and restraints analyzed in the detailed report include:

- Embedded Finance in E-Commerce and Super Apps

- Dollar-Linked Savings and Stablecoin Adoption

- FX Controls, Settlement Frictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital payments captured 45.1% of the South American fintech market share in 2025, underpinned by rails such as Brazil's Pix and Argentina's Transferencias 3.0, which have lowered acceptance costs for consumers and merchants. Within the segment mix, digital lending is forecast to expand at a 21.3% CAGR between 2026 and 2031, highlighting acceleration in the South American fintech market as thin-file underwriting scales through open-finance data and embedded-credit channels. Lenders now combine consented bank data with marketplace and logistics histories to assess repayment behaviour for consumer and MSMB borrowers, compressing approval times while lifting acceptance rates for previously underserved cohorts. Nubank's secured-lending portfolio grew 133% year over year in 2025, aided by access to verified salary deposits and account flows that strengthened origination quality and collections. Mercado Libre's fintech arm scaled credit issuance to USD 11 billion by Q3 2025, using marketplace transaction data and delivery touchpoints to calibrate revolving balances, delinquency, and pricing.

Momentum in investment and insurance adjacencies has supported a more complete proposition for retail and MSMB users. Mercado Pago's assets under management doubled year over year to USD 15.1 billion in Q3 2025 as money-market products were bundled into daily-wallet experiences with attractive benchmark-linked yields. Neobanks and payments platforms have introduced targeted protection products for small businesses, embedding coverage options into onboarding and checkout flows to increase attach rates over time. As providers expand into lending at scale, compliance standards linked to data protection and AML have increased fixed costs and favoured players with robust governance and capital, reinforcing consolidation dynamics in the South American fintech market. On balance, the South America fintech industry continues to shift from single-product payments toward multi-product financial services, with credit-led monetization driving the next leg of growth, where consented data support underwriting and collections.

The South America Fintech Market Report is Segmented by Service Proposition (Digital Payments, Digital Lending and Financing, Digital Investments, Insurtech, Neobanking), End-User (Retail, Businesses), User Interface (Mobile Applications, Web/Browser, POS/IoT Devices), and Geography (Brazil, Peru, Chile, Argentina, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Nubank (Nu Holdings)

- Mercado Pago (Mercado Libre)

- PagSeguro (PagBank)

- StoneCo

- PicPay

- Inter&Co (Banco Inter)

- EBANX

- dLocal

- Uala

- C6 Bank

- Creditas

- Neon

- XP Inc.

- BTG Pactual (digital platforms)

- Getnet Brasil (Santander)

- Prisma Medios de Pago (Argentina)

- Naranja X (Argentina)

- Brubank (Argentina)

- MACH (Banco de Chile)

- Khipu (Chile)

- FPay (Falabella)

- Transbank (Chile)

- Yape (Peru)

- Plin (Peru)

- RecargaPay (Brazil)

- SumUp (Brazil)

- Dock (Brazil)

- Pismo (Brazil)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 RTP scale-up and features

- 4.2.2 Open finance data portability

- 4.2.3 Embedded finance in platforms

- 4.2.4 SoftPOS and low-cost acceptance

- 4.2.5 Dollar-linked savings via fintech

- 4.2.6 Tokenized deposits and CBDC

- 4.3 Market Restraints

- 4.3.1 High Customer Acquisition Costs and Low Financial Literacy

- 4.3.2 Fee caps squeeze economics

- 4.3.3 APP fraud on instant rails

- 4.3.4 FX controls, settlement frictions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Real-time payments infrastructure status

- 4.8 Merchant acceptance & QR interoperability landscape

- 4.9 Cash-in/Cash-out (CICO) and agent network coverage

- 4.10 Porter's Five Forces Analysis

- 4.10.1 Threat of New Entrants

- 4.10.2 Bargaining Power of Suppliers

- 4.10.3 Bargaining Power of Buyers

- 4.10.4 Threat of Substitutes

- 4.10.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Proposition

- 5.1.1 Digital Payments

- 5.1.2 Digital Lending and Financing

- 5.1.3 Digital Investments

- 5.1.4 Insurtech

- 5.1.5 Neobanking

- 5.2 By End-User

- 5.2.1 Retail

- 5.2.2 Businesses

- 5.3 By User Interface

- 5.3.1 Mobile Applications

- 5.3.2 Web / Browser

- 5.3.3 POS / IoT Devices

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Peru

- 5.4.3 Chile

- 5.4.4 Argentina

- 5.4.5 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Nubank (Nu Holdings)

- 6.4.2 Mercado Pago (Mercado Libre)

- 6.4.3 PagSeguro (PagBank)

- 6.4.4 StoneCo

- 6.4.5 PicPay

- 6.4.6 Inter&Co (Banco Inter)

- 6.4.7 EBANX

- 6.4.8 dLocal

- 6.4.9 Uala

- 6.4.10 C6 Bank

- 6.4.11 Creditas

- 6.4.12 Neon

- 6.4.13 XP Inc.

- 6.4.14 BTG Pactual (digital platforms)

- 6.4.15 Getnet Brasil (Santander)

- 6.4.16 Prisma Medios de Pago (Argentina)

- 6.4.17 Naranja X (Argentina)

- 6.4.18 Brubank (Argentina)

- 6.4.19 MACH (Banco de Chile)

- 6.4.20 Khipu (Chile)

- 6.4.21 FPay (Falabella)

- 6.4.22 Transbank (Chile)

- 6.4.23 Yape (Peru)

- 6.4.24 Plin (Peru)

- 6.4.25 RecargaPay (Brazil)

- 6.4.26 SumUp (Brazil)

- 6.4.27 Dock (Brazil)

- 6.4.28 Pismo (Brazil)

7 Market Opportunities & Future Outlook

- 7.1 Cross-border instant-payment corridors (e.g., Pix-enabled international flows and merchant-of-record use cases)

- 7.2 SME embedded finance for B2B trade (real-time FX, invoice financing, supply-chain payments)