PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044001

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044001

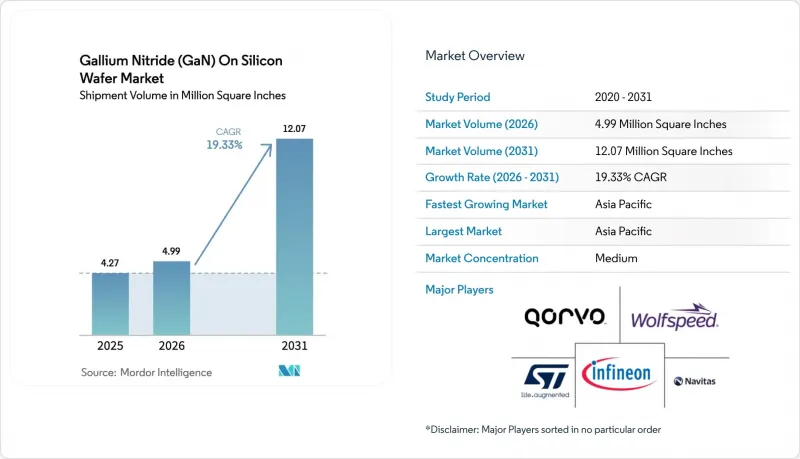

Gallium Nitride (GaN) On Silicon Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Gallium Nitride (GaN) on Silicon Wafer market size is expected to increase from 4.27 million square inches in 2025 to 4.99 million square inches in 2026 and reach 12.07 million square inches by 2031, growing at a CAGR of 19.33% over 2026-2031.

Robust migration from legacy silicon toward wide-bandgap designs is enabling higher switching frequencies, elevated thermal conductivity, and power densities above 3 kW per cubic inch. Original equipment manufacturers are fast-tracking 200 mm GaN-on-Si qualification in response to 800-volt electric-vehicle traction inverters, mandated USB-C Power Delivery 3.1 fast-charging rules, and satellite-based 5G non-terrestrial network rollouts. Competitive pressure is intensifying as integrated device manufacturers, foundries, and fabless start-ups secure design wins in fast-charging adapters, data-center power supplies, and lidar drivers, while government subsidies in North America and Europe accelerate 300 mm pilot lines and compress commercialization timelines.

Global Gallium Nitride (GaN) On Silicon Wafer Market Trends and Insights

Maturing 200 mm GaN-on-Si Fabrication Lines

Multiple device makers qualified 200 mm GaN-on-Si wafers during 2025, cutting die costs and enabling higher unit volumes. Infineon began customer sampling of 300 mm GaN power devices in late 2025 and targets production by end-2026. Innoscience plans to scale to 20,000 wafers per month on 8-inch lines by 2025 and reach 70,000 by 2030. Navitas and PSMC completed 200 mm qualification in fourth-quarter 2025 and will ramp production in first-half 2026. These moves shorten lead times, support dual-sourcing, and spur adoption in automotive, industrial, and consumer segments. The Gallium Nitride (GaN) on Silicon Wafer market benefits from cost parity with super-junction silicon as scale economies improve.

Falling Epi-Wafer Costs Due to Higher MOCVD Throughput

Tool vendors have released multi-wafer planetary reactors that raise throughput by up to 60%, lowering epitaxial costs by roughly one-third within two years. Veeco's Propel platform processes eight 200 mm wafers per run with in-situ metrology for tighter process control. AIXTRON's G5+C handles 19 wafers per cycle, reducing cycle time and boosting yield. Lower costs open consumer applications such as USB-C adapters and wireless chargers that were previously bill-of-materials sensitive. Fabless firms can now bid for high-volume designs, expanding the Gallium Nitride (GaN) on Silicon Wafer market footprint across entry-level price points.

Threading Dislocations Impacting Yield Beyond 8 inch

Heteroepitaxial growth on silicon introduces threading dislocations, which degrade the breakdown voltage and increase leakage. Dislocation densities of 1X108 cm-2 to 5X108 cm-2 persist at 200 mm, trimming yields by up to 20% in early lots. Longer thermal gradients at 300 mm worsen edge stress and bow, extending qualification and capex. Device makers are adding graded AlGaN buffers and in-situ nitride interlayers, yet the learning curve slows the Gallium Nitride (GaN) on Silicon Wafer market ramp.

Other drivers and restraints analyzed in the detailed report include:

- Surge in 800 V Electric-Vehicle Powertrain Architectures

- Mandatory USB-C PD 3.1 240 W Fast-Charging Adoption

- Limited Availability of 8 inch GaN Growth Tools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 150 mm format accounted for 53.92% of shipments in 2025 as mature epitaxial recipes and depreciated tool bases supported attractive economics. However, the 200 mm tier is projected to register a 20.37% CAGR through 2031, providing 35-45% die cost savings once yield curves mature. onsemi secured dual-source 200 mm capacity through partnerships with Innoscience and GlobalFoundries, with samples due in first-half of 2026. The Gallium Nitride (GaN) on Silicon Wafer market therefore pivots toward 200 mm as mainstream, while 100 mm remains limited to research and low-volume defense needs.

Infineon's customer sampling of 300 mm GaN in October 2025 underscores an aggressive scaling roadmap aimed at automotive and industrial volumes. imec's 300 mm pilot line integrates GaN with advanced CMOS to target single-chip power-management ICs. Early success will depend on mitigating wafer bow and threading dislocations. If process control succeeds, Gallium Nitride (GaN) on Silicon Wafer market size advantages at 300 mm could replicate historical silicon cost curves and accelerate commoditization.

GaN-on-silicon held 57.49% of 2025 volume and is forecast to grow at 19.78% through 2031, anchored by compatibility with 200 mm and 300 mm silicon fabs and shared precursor supply chains. This cost leadership underpins high-volume consumer and automotive applications, reinforcing dominance within the Gallium Nitride (GaN) on Silicon Wafer market. GaN-on-silicon carbide, despite superior thermal conductivity, remains niche for military radar and satellite transponders where performance trumps a four-fold price premium.

GaN-on-sapphire continues to serve the optoelectronics industry, especially micro-LEDs and ultraviolet emitters. Native GaN substrates deliver the lowest dislocation densities but are cost-prohibitive beyond small research lots. Consequently, market participants allocate R&D to superlattice buffer innovations that raise GaN-on-silicon reliability and extend its addressable voltage up to 1,200 V, keeping the Gallium Nitride (GaN) on Silicon Wafer market share firmly in silicon's corner.

The Gallium Nitride (GaN) On Silicon Wafer Market Report is Segmented by Wafer Diameter (100 Mm, 150 Mm, and 200 Mm), Substrate Type (GaN-On-Silicon, GaN-On-Silicon Carbide, and More), Device Application (Power Electronics, Radio-Frequency Devices, and More), End-Use Industry (Automotive and EV, Aerospace and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Volume (Square Inches).

Geography Analysis

Asia-Pacific accounted for 62.53% of 2025 volume and is slated to grow at a 20.27% CAGR through 2031. China backs Innoscience's plan to reach 70,000 wafers per month over five years, while Taiwan explores GaN-CMOS integration for mobile and automotive products. Japan leverages decades of compound semiconductor expertise at ROHM, Toshiba, and Mitsubishi Electric, whereas South Korea targets data center and 5G power modules. India offers incentives for pilot lines, but commercial output remains embryonic, so the Gallium Nitride (GaN) on Silicon Wafer market continues to center on East-Asian ecosystems.

North America benefits from USD 52 billion in CHIPS and Science Act funding. MACOM secured preliminary support for a GaN-on-SiC RF line, highlighting the federal commitment to the security of wide-bandgap supply. U.S. foundries collaborate with fabless start-ups to build automotive-grade GaN devices, while Canada advances Arctic surveillance radar programs. Mexican assembly sites co-locate with electric-vehicle plants, extending regionalization advantages within the Gallium Nitride (GaN) on Silicon Wafer market.

Europe advances through EUR 43 billion in EU CHIPS Act resources and EUR 8.1 billion in IPCEI microelectronics grants, funneling capital to Infineon's 300 mm pilot line and Fraunhofer wide-bandgap projects. France heads an IPCEI cluster on ultra-wide-bandgap materials, and the United Kingdom focuses on RF devices for satellite links. ASML in the Netherlands explores lithography tooling for GaN patterning, while Italy promotes STMicroelectronics' MasterGaN platform. Outside the core triad, South America, the Middle East, and Africa remain nascent, with isolated renewable-energy pilots using GaN in Brazil and the United Arab Emirates.

- Wolfspeed Inc.

- Qorvo Inc.

- NXP Semiconductors N.V.

- Infineon Technologies AG

- STMicroelectronics N.V.

- Renesas Electronics Corporation

- Efficient Power Conversion (EPC) Corp.

- Transphorm Inc.

- Toshiba Electronic Devices and Storage Corp.

- ROHM Co., Ltd.

- Navitas Semiconductor Corp.

- Innoscience (Suzhou) Technology Co., Ltd.

- MACOM Technology Solutions Holdings Inc.

- ON Semiconductor Corp.

- GaN Systems Inc.

- Power Integrations Inc.

- Skyworks Solutions Inc.

- Mitsubishi Electric Corp.

- Sumitomo Electric Industries Ltd.

- Integra Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value-Chain Analysis

- 4.3 Technological Outlook

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Market Drivers

- 4.5.1 Maturing 200 Mm GaN-on-Si Fabrication Lines

- 4.5.2 Falling Epi-Wafer Costs Due To Higher MOCVD Throughput

- 4.5.3 Surge In 800 V EV Powertrain Architectures

- 4.5.4 Mandatory USB-C PD3.1 240 W Fast-Charging Adoption

- 4.5.5 Rising Deployment Of Satellite-Based 5G NTN Backhaul

- 4.5.6 Government Incentives For Wide-Bandgap Fabs (CHIPS, EU IPCEI)

- 4.6 Market Restraints

- 4.6.1 Threading Dislocations Impacting Yield Beyond 8 Inch

- 4.6.2 Limited Availability Of 8 Inch GaN Growth Tools

- 4.6.3 IP Cross-Licensing Barriers Among IDMs and Foundries

- 4.6.4 Thermal Mismatch Induced Wafer Bow At ?200 mm

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Wafer Diameter

- 5.1.1 100 mm (4 inch)

- 5.1.2 150 mm (6 inch)

- 5.1.3 200 mm (8 inch)

- 5.2 By Substrate Type

- 5.2.1 GaN-on-Silicon

- 5.2.2 GaN-on-Silicon Carbide

- 5.2.3 GaN-on-Sapphire

- 5.2.4 Native GaN (Bulk)

- 5.3 By Device Application

- 5.3.1 Power Electronics

- 5.3.2 Radio-Frequency Devices

- 5.3.3 Optoelectronics (LED and Laser)

- 5.3.4 Other Applications

- 5.4 By End-Use Industry

- 5.4.1 Automotive and EV

- 5.4.2 Aerospace and Defense

- 5.4.3 Renewable Energy and Storage

- 5.4.4 Consumer Electronics

- 5.4.5 Telecommunications

- 5.4.6 Industrial Power Systems

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Taiwan

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East

- 5.5.6 Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Wolfspeed Inc.

- 6.4.2 Qorvo Inc.

- 6.4.3 NXP Semiconductors N.V.

- 6.4.4 Infineon Technologies AG

- 6.4.5 STMicroelectronics N.V.

- 6.4.6 Renesas Electronics Corporation

- 6.4.7 Efficient Power Conversion (EPC) Corp.

- 6.4.8 Transphorm Inc.

- 6.4.9 Toshiba Electronic Devices and Storage Corp.

- 6.4.10 ROHM Co., Ltd.

- 6.4.11 Navitas Semiconductor Corp.

- 6.4.12 Innoscience (Suzhou) Technology Co., Ltd.

- 6.4.13 MACOM Technology Solutions Holdings Inc.

- 6.4.14 ON Semiconductor Corp.

- 6.4.15 GaN Systems Inc.

- 6.4.16 Power Integrations Inc.

- 6.4.17 Skyworks Solutions Inc.

- 6.4.18 Mitsubishi Electric Corp.

- 6.4.19 Sumitomo Electric Industries Ltd.

- 6.4.20 Integra Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment