PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044015

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044015

5G Semiconductor Silicon Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

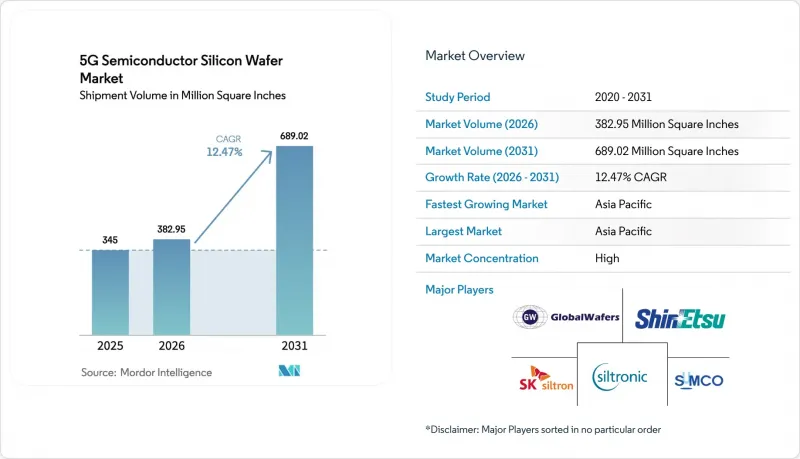

The 5G semiconductor silicon wafer market size is expected to grow from 345 million square inches in 2025 to 382.95 million square inches in 2026, and is forecast to reach 689.02 million square inches by 2031, at a 12.47% CAGR over 2026-2031. Sub-7-nanometer migration across smartphones, densification of urban 5G infrastructure, and sustained conversion to 300-millimeter substrates remain the structural growth engines for the 5G semiconductor silicon wafer market. Strong procurement from Asia-Pacific handset makers secures long-term foundry output, while North American and European onshoring programs diversify geographic supply without displacing the region's dominance. Tight substrate availability enables the top five wafer makers to push annual price escalators, and recent consolidation, such as Doosan's purchase of SK Siltron, intensifies the negotiating leverage of incumbents. Environmental restrictions on ultra-pure water usage and polysilicon price swings temper margin expansion but have not derailed capex programs that underpin the 5G semiconductor silicon wafer market's growth trajectory.

Global 5G Semiconductor Silicon Wafer Market Trends and Insights

Surging Mobile Data Traffic from 5G Smartphones

Global 5G handset shipments reached 1.2 billion in 2024 and are forecast to hit 1.5 billion by 2026, each premium device relying on sub-7 nanometer dies that consume materially larger wafer area. Flagship processors, such as Apple's A18 Pro with 19 billion transistors, demand silicon flatness below 0.3 micrometers to avoid EUV patterning defects. Foundries pre-book 300 millimeter capacity up to a year ahead, pushing substrate list prices 12%-15% higher year-on-year. Because a single sub-20 nanometer particle can kill an entire advanced die, customers increasingly shift to epitaxial-quality wafers with <0.01 defects per cm2, locking in premium contracts for the 5G semiconductor silicon wafer market.

Rapid Deployment of 5G Telecom Infrastructure

China installed 4.2 million 5G base stations by December 2024 and targets 5 million by end-2025, retaining mature-node demand for RF front-ends while digital baseband moves to 7 nanometers. European operators accelerated small-cell rollouts using Ericsson's RAN Compute systems that integrate 7 nanometer ASSPs. The densification wave multiplies required sites per square kilometer, lifting mixed-node wafer demand spanning 180 nanometers to 7 nanometers. Suppliers serving the 5G semiconductor silicon wafer market, therefore, schedule overlapping 200 millimeter and 300 millimeter production runs to hedge node volatility.

High Capital Expenditure for 300 mm Wafer Fabs

Building a greenfield 300 millimeter plant costs USD 10 billion-USD 20 billion, keeping new entry rare and reinforcing the oligopoly that underpins pricing power. GlobalWafers' USD 7.5 billion Texas project received USD 1.5 billion in U.S. grants, yet still faces a five-year ramp before revenue begins. SUMCO elected to close a legacy 200 millimeter line rather than reinvest, signaling that even incumbents exit sub-scale assets when payback periods lengthen. Resulting capacity staging in 50,000-wafer-per-month increments limits supply elasticity for the 5G semiconductor silicon wafer market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Advanced Node Chips in 5G Devices

- Adoption of Silicon Wafer Thinning for 5G mmWave Antenna Integration

- Supply Chain Disruptions of Semiconductor Grade Polysilicon

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 300 millimeter category held 59.32% of the market share in 2025 and benefits from a 13.23% CAGR, cementing its primacy through 2031. Each 300-millimeter wafer yields roughly 2.4X the die count of a 200-millimeter wafer, translating to 30%-35% lower unit fabrication cost once depreciation is absorbed. Leading fabs in Arizona, Pyeongtaek, and Ireland process only this diameter, ensuring locked-in baseline demand. The 5G semiconductor silicon wafer market size for 300 millimeter substrates will therefore scale faster than any other diameter set.

Although 200 millimeters remains indispensable for legacy RF, power, and MEMS, capital plans heavily favor 300 millimeter lines capable of ultra-thin grinding for chip-on-wafer-on-substrate packaging. Suppliers able to guarantee warp-free thinning below 50 micrometers capture premium contracts, while second-tier producers focus on stabilizing 200-micrometer service for automotive and industrial buyers. This bifurcation secures long-run growth and cushions cyclicality within the broader 5G semiconductor silicon wafer market.

The 5G Semiconductor Silicon Wafer Market Report is Segmented by Wafer Diameter (300 Mm and 200 Mm), Technology Node (Advanced Node, Mainstream Node, and Mature Node), End Application (Smartphones, Telecom Infrastructure, Fixed Wireless Access, and Industrial 5G), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Volume (Square Inches).

Geography Analysis

Asia-Pacific controlled 72.61% of the 5G semiconductor silicon wafer market in 2025 and expands at 13.83% CAGR through 2031. China's 4.2 million macro base stations and Taiwan's foundry cluster together generate unrivaled demand pools, while Japanese wafer suppliers command more than half of global 300 millimeter output. Regional policy, notably Beijing's localization mandates and Tokyo's advanced packaging subsidies, further anchors capacity and reinforces the region's leadership position.

North America captures strategic mindshare through the U.S. CHIPS and Science Act, which subsidizes fabs in Texas, Arizona, New York, and Ohio. Once fully online by 2028, these sites will consume roughly 30-35 million square inches annually about 10% global share securing domestic supply for defense and critical infrastructure without materially eroding Asia's volume lead. Canada and Mexico accelerate complimentary back-end and mature-node investments, rounding out a continental ecosystem that supports the 5G semiconductor silicon wafer market.

Europe's Chips Act channels EUR 43 billion (USD 47 billion) into new capacity, lifting regional wafer demand from 8% in 2025 toward an expected 12%-14% by 2030 once sites in Magdeburg and Dresden ramp. South America and the Middle East and Africa jointly remain below 3% share, with growth tied to automotive electrification in Brazil and data-center deployments in the United Arab Emirates. These smaller regions nonetheless widen the global footprint of the 5G semiconductor silicon wafer market.

List of Companies Covered in this Report:

- Shin-Etsu Chemical Co., Ltd.

- SUMCO Corporation

- GlobalWafers Co., Ltd.

- Siltronic AG

- SK Siltron Co., Ltd.

- Wafer Works Corporation

- Gritek Electronics Co., Ltd.

- Addison Engineering, Inc.

- Ferrotec Holdings Corporation

- Okmetic Oyj

- LG Electronics Inc. (Wafer Business)

- Taiwan Semiconductor Manufacturing Company Limited

- Samsung Electronics Co., Ltd.

- GlobalFoundries Inc.

- Semiconductor Manufacturing International Corporation

- United Microelectronics Corporation

- Tower Semiconductor Ltd.

- Vanguard International Semiconductor Corporation

- Powerchip Semiconductor Manufacturing Corporation

- onsemi

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Mobile Data Traffic from 5G Smartphones

- 4.2.2 Rapid Deployment of 5G Telecom Infrastructure

- 4.2.3 Increasing Demand for Advanced Node Chips in 5G Devices

- 4.2.4 Adoption of Silicon Wafer Thinning for 5G mmWave Antenna Integration

- 4.2.5 Growth of Private 5G Networks in Industrial Automation

- 4.2.6 Government Incentives for Localized Wafer Fabrication in Emerging Economies

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure for 300 mm Wafer Fabs

- 4.3.2 Supply Chain Disruptions of Semiconductor Grade Polysilicon

- 4.3.3 Yield Challenges at <7nm Nodes for RF Front-End ICs

- 4.3.4 Environmental Regulations Limiting Ultra-Pure Water Usage in Wafer Production

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Wafer Diameter

- 5.1.1 300 mm

- 5.1.2 200 mm

- 5.2 By Technology Node

- 5.2.1 Advanced Node (Below 7nm)

- 5.2.2 Mainstream Node (10nm-28nm)

- 5.2.3 Mature Node (Above 28nm)

- 5.3 By End Application

- 5.3.1 Smartphones

- 5.3.2 Telecom Infrastructure (Macro / Small Cells)

- 5.3.3 Fixed Wireless Access (FWA)

- 5.3.4 Industrial 5G

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Taiwan

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Shin-Etsu Chemical Co., Ltd.

- 6.4.2 SUMCO Corporation

- 6.4.3 GlobalWafers Co., Ltd.

- 6.4.4 Siltronic AG

- 6.4.5 SK Siltron Co., Ltd.

- 6.4.6 Wafer Works Corporation

- 6.4.7 Gritek Electronics Co., Ltd.

- 6.4.8 Addison Engineering, Inc.

- 6.4.9 Ferrotec Holdings Corporation

- 6.4.10 Okmetic Oyj

- 6.4.11 LG Electronics Inc. (Wafer Business)

- 6.4.12 Taiwan Semiconductor Manufacturing Company Limited

- 6.4.13 Samsung Electronics Co., Ltd.

- 6.4.14 GlobalFoundries Inc.

- 6.4.15 Semiconductor Manufacturing International Corporation

- 6.4.16 United Microelectronics Corporation

- 6.4.17 Tower Semiconductor Ltd.

- 6.4.18 Vanguard International Semiconductor Corporation

- 6.4.19 Powerchip Semiconductor Manufacturing Corporation

- 6.4.20 onsemi

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment