PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044042

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044042

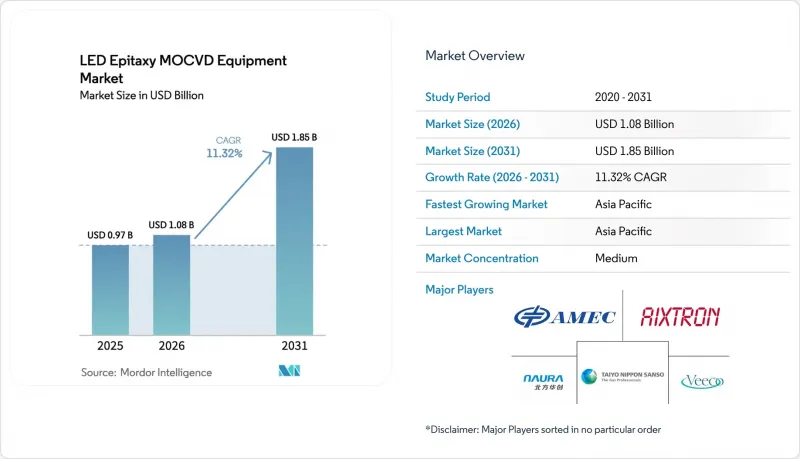

LED Epitaxy MOCVD Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The LED epitaxy MOCVD equipment market size is expected to grow from USD 0.97 billion in 2025 to USD 1.08 billion in 2026 and is forecast to reach USD 1.85 billion by 2031 at 11.32% CAGR over 2026-2031.

Display makers are shifting from edge-lit LCD backlighting to direct-lit mini-LED and micro-LED architectures, multiplying wafer demand per television and dashboard. Compound-semiconductor fabs are migrating to 200 mm GaN-on-Si substrates that can share tool sets with power electronics, lowering cost curves and raising the barrier to entry. Subsidy programs under the United States CHIPS and Science Act, the EU Chips Act, and several Chinese provincial funds are underwriting new domestic epitaxy capacity. The LED epitaxy MOCVD equipment market diverges from the broader wafer-fab equipment cycle because regulatory drivers in sterilization, automotive safety, and energy efficiency underpin demand when memory and logic investments pause.

Global LED Epitaxy MOCVD Equipment Market Trends and Insights

Proliferation of Mini and Micro LED Backlighting

Panel makers are replacing edge-lit assemblies with direct-lit mini-LED and micro-LED matrices that allow more than 10 000 dimming zones per television. Each premium set uses up to ten times the epitaxy wafer area once allocated to legacy backlights, raising steady-state reactor utilization. Automotive dashboards, head-up displays, and augmented-reality wearables now specify micro-LED for sunlight readability, further expanding addressable volume. San'an Optoelectronics lifted micro-LED capacity above 1 400 six-inch wafers a month in 2025 after passing customer audits, signalling that micro-LED has entered commercial scale. Foundries note rising demand for blue and green dice that support optical interconnects inside hyperscale data centers, providing a non-display growth lane. The remaining bottleneck is efficient red emission on GaN-on-Si, which has prompted equipment vendors to refine chamber designs that can switch to AlInGaP recipes without cross-contamination.

Accelerated Transition to 200 mm GaN-On-Si Platforms

LED producers are qualifying 200 mm GaN-on-Si templates to share depreciation with power-device lines and to cut per-die epitaxy cost by roughly one-third. Ennostar and ALLOS Semiconductors are co-developing common substrates so the same reactor fleet can serve headlamp LEDs and 650 V transistors. IQE added multiwafer tools in Newport, United Kingdom, and Massachusetts, United States, demonstrating automotive-grade power devices grown on the identical chambers that supply micro-LED wafers. Managing wafer bow on 200 mm silicon remains difficult, therefore planetary reactors with multi-zone heating and real-time pyrometry command premium pricing. Once average utilizations surpass 70%, fab owners report thirty percent lower cost per lumen than on 150 mm lines, driving a second wave of conversions after 2027.

Cyclicality in General Lighting Investments

General lighting still commands roughly forty percent of wafer runs, yet end-market demand yo-yos with construction cycles, rebate expirations, and interest-rate shifts. San'an Optoelectronics saw LED wafer revenue drop almost four percent year over year in 2025 even as margins rose, signalling that producers pushed capacity toward automotive and display niches. Aixtron's filings confirmed a double-digit share contraction for its LED segment in 2025 as customers paused orders during inventory corrections. Because lamps now exceed 50 000-hour lifetime, replacement sales decelerate and growth shifts to smart-lighting retrofits, which stall during downturns. The LED epitaxy MOCVD equipment market therefore faces near-term softness when housing starts or commercial tenancy dip.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies for Compound-Semiconductor Fabs

- Rising Demand for UV-C LED Sterilization Systems

- High Capital Intensity for 200 mm Planetary Tools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

GaN platforms retained 67.86% of the LED epitaxy MOCVD equipment market in 2025 because they underpin blue and white diodes for general illumination and automotive lamps. AlGaN ultraviolet tools, though starting from a smaller base, are forecast to rise at 12.53% CAGR through 2031, the fastest among material systems, as regulators phase out mercury-based sterilizers. The LED epitaxy MOCVD equipment market size for AlGaN lines is still modest compared with visible-spectrum capacity, yet each installed reactor produces higher average selling price wafers and therefore delivers superior gross margin for equipment vendors. Recent shipments to European universities reflect public-health funding momentum that offsets early-stage process complexity.

Most fabs wrestle with efficiency loss when aluminum fractions exceed fifty percent, which drives R&D into pulsed precursor flows, in-situ stress monitoring, and substrate miscuts that mitigate dislocation formation. IQE pursues a dual track, keeping red emission on GaAs today while developing gallium-nitride alternatives for future generations. Tool makers answer with hybrid chambers capable of switching between GaN, AlGaN, and AlInGaP within a single preventive-maintenance cycle, trimming capex by up to thirty percent for foundries that must serve multi-color micro-LED customers.

Reactors configured for 150 mm wafers accounted for 47.39% of the market share in 2025, buoyed by well-debugged recipes and legacy fab infrastructure. The LED epitaxy MOCVD equipment market size tied to 200 mm tools is projected to increase fastest, tracking a 12.38% CAGR into 2031 as IDMs retrofit mothballed silicon lines and chase scale economies. Bow control challenges persist, yet planetary configurations with zoned heating raise yield above eighty-five percent, closing the gap with smaller wafers.

Foundries leverage the larger format to align with downstream dicing and packaging lines already optimized for power devices, slashing cost per lumen. PwC observes that optoelectronics lags logic on diameter migration; nevertheless, 200 mm tipping points emerge whenever annual output crosses ten thousand wafers per tool. IDMs with high automotive mix and micro-LED roadmaps have already breached that volume, whereas commodity lamp suppliers still depend on fully depreciated 100 mm and 150 mm fleets.

The LED Epitaxy MOCVD Equipment Market Report is Segmented by LED Material System (GaN-Based LED Epitaxy Systems, and More), Wafer Size Capability (Up To 100mm, 150mm, and 200mm and Above), Reactor Configuration (Planetary Reactors, and Showerhead Reactors), End User (Integrated LED Manufacturers, and Epitaxy Foundries and Merchant Epi Suppliers), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 48.42% of LED epitaxy MOCVD equipment market revenue in 2025 and is projected to grow at 12.98% CAGR to 2031. Chinese municipal and national funds together exceed USD 840 million earmarked for compound-semiconductor self-reliance, subsidizing both tool purchases and precursor plants. Taiwan's legacy 100 mm lines transition to 150 mm and 200 mm formats, adding volume without greenfield construction. San'an Optoelectronics ramped six-inch micro-LED capacity after Samsung qualification, illustrating ecosystem readiness for display-grade volumes. Japan and South Korea sustain healthy replacement demand as Nichia and Seoul Semiconductor upgrade fleets for higher luminous-efficacy mandates.

North America and Europe together held roughly 35-40% share in 2025, with unit growth tethered to subsidy rollouts rather than lamp sales. Washington dispersed multi-million-dollar grants to IntelliEPI, Coherent, Macom, and GlobalWafers, each targeting domestic wafer starts. Brussels backed IMEC's pilot line with EUR 700 million (USD 756 million) and set an ambition to halve dependency on imported nitride wafers. Export licences lengthen lead times for high-spec reactors into China, nudging Western vendors to allocate scarce slots to regional customers first, thereby inflating local order backlogs.

The Rest of the World, covering South America, Middle East, and Africa, contributed about one-tenth of revenue in 2025. Australia enacted minimum 140 lumen-per-watt standards in March 2026, indirectly lifting wafer quality requirements and driving imports of high-uniformity dice. Gulf municipalities deploy adaptive streetlights within smart-city programs, yet chips still ship mainly from Korean and Chinese vendors. Water-sanitation pilots in rural Africa adopt UV-C modules powered by solar panels, creating small but strategic demand pockets that Asian merchant epi houses presently serve.

- Veeco Instruments Inc.

- Aixtron SE

- Taiyo Nippon Sanso Corp.

- Advanced Micro-Fabrication Equipment Inc. China

- Jiangsu Huantian Science and Technology Co. Ltd.

- Tempress Technologies B.V.

- Jusung Engineering Co. Ltd.

- Guangzhou China-Topstar Technology Co. Ltd.

- Pro-M Tec GmbH

- EpiGaN N.V.

- LPE S.p.A.

- Piotech Inc.

- Samco Inc.

- NuFlare Technology Inc.

- Epiluvac AB

- Naura Technology Group Co. Ltd.

- Wuhan Pactech Microelectronics Equipment Co. Ltd.

- CVD Equipment Corporation

- Taiyo Nippon Sanshin Electronic Co. Ltd.

- Intellion Semiconductor Equipment Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Mini and Micro LED Backlighting

- 4.2.2 Accelerated Transition to 200 mm GaN-on-Si Platforms

- 4.2.3 Rising Demand for UV-C LED Sterilization Systems

- 4.2.4 Government Subsidies for Compound-Semiconductor Fabs

- 4.2.5 Automotive OEM Shift to Adaptive LED Headlamps

- 4.2.6 Sustainability Push Toward High-Efficiency Lighting

- 4.3 Market Restraints

- 4.3.1 Cyclicality in General Lighting Investments

- 4.3.2 Complex Process Control Versus HVPE Alternatives

- 4.3.3 IP Litigation Risk in Epitaxy Process Recipes

- 4.3.4 High Capital Intensity for 200 mm Planetary Tools

- 4.4 Industry Supply Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Material System

- 5.1.1 GaN-based LED Epitaxy Systems

- 5.1.2 AlGaN UV LED Epitaxy Systems

- 5.1.3 AlInGaP LED Epitaxy Systems

- 5.2 By Wafer Size Capability

- 5.2.1 Upto 100 mm

- 5.2.2 150 mm

- 5.2.3 200 mm and Above

- 5.3 By Reactor Configuration

- 5.3.1 Planetary Reactors

- 5.3.2 Showerhead Reactors

- 5.4 By End User

- 5.4.1 Integrated LED Manufacturers (IDMs)

- 5.4.2 Epitaxy Foundries and Merchant Epi Suppliers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia-Pacific

- 5.5.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Veeco Instruments Inc.

- 6.4.2 Aixtron SE

- 6.4.3 Taiyo Nippon Sanso Corp.

- 6.4.4 Advanced Micro-Fabrication Equipment Inc. China

- 6.4.5 Jiangsu Huantian Science and Technology Co. Ltd.

- 6.4.6 Tempress Technologies B.V.

- 6.4.7 Jusung Engineering Co. Ltd.

- 6.4.8 Guangzhou China-Topstar Technology Co. Ltd.

- 6.4.9 Pro-M Tec GmbH

- 6.4.10 EpiGaN N.V.

- 6.4.11 LPE S.p.A.

- 6.4.12 Piotech Inc.

- 6.4.13 Samco Inc.

- 6.4.14 NuFlare Technology Inc.

- 6.4.15 Epiluvac AB

- 6.4.16 Naura Technology Group Co. Ltd.

- 6.4.17 Wuhan Pactech Microelectronics Equipment Co. Ltd.

- 6.4.18 CVD Equipment Corporation

- 6.4.19 Taiyo Nippon Sanshin Electronic Co. Ltd.

- 6.4.20 Intellion Semiconductor Equipment Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment