PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044070

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044070

Scrap Metal Recycling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

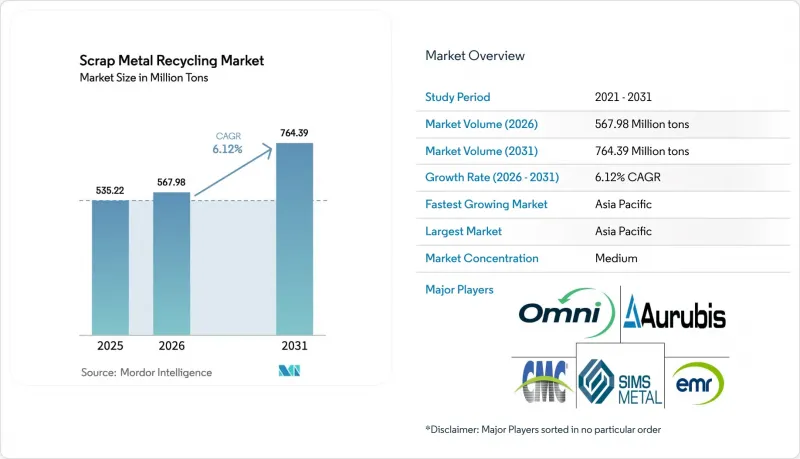

The Scrap Metal Recycling Market size is projected to expand from 535.22 Million tons in 2025 and 567.98 Million tons in 2026 to 764.39 Million tons by 2031, registering a CAGR of 6.12% between 2026 to 2031.

Three structural factors are driving the near-term growth. First, the introduction of new electric arc furnaces (EAFs) in India, the Middle-East, and Southeast Asia is increasing domestic scrap consumption and reducing export volumes. Second, automotive and electronics original equipment manufacturers (OEMs) are securing low-residual contracts, which limit spot market availability. Third, the OECD's advocacy for open scrap trade is encouraging regulators to adopt uniform quality standards, although national export levies continue to create tight regional balances. These dynamics enhance the profitability of processors capable of maintaining copper content below 0.15% while disadvantaging facilities that still depend on manual sorting methods.

Global Scrap Metal Recycling Market Trends and Insights

Rapid EAF Capacity Additions in India, MENA, and Southeast Asia

EAF projects launched since 2024 have reshaped intra-Asian scrap flows. Tata Steel's Punjab furnace alone increased local demand by 0.75 million tons in its first operational year, while Emirates Steel Arkan's 3.5 million-ton Abu Dhabi plant redirected Gulf cargoes that previously went to Turkey. Between 2024 and 2025, Indonesia, Vietnam, and Malaysia added 2.8 million tons of new EAF capacity, absorbing Japanese scrap that previously moved to China. As these furnaces reach full capacity, the Scrap Metal Recycling Market faces challenges such as limited short-haul trucking capacity and higher premiums for prompt material within 300 kilometers of mill gates. Increased local demand is expected to boost collection rates in secondary cities where organized scrap chains were previously underdeveloped.

Vertically Integrated Mill M&A to Secure Captive Scrap

Steelmakers have accelerated acquisitions of scrap yards to secure supply following a 45% spike in pig-iron prices in early 2024, which compressed melt-shop margins. ArcelorMittal's acquisition of half of Nippon Steel's continental processing network ensures access to 2 million tons of certified feed while reducing transaction costs by at least USD 12 per ton. In the United States, Nucor's David J. Joseph subsidiary acquired 12 Midwest yards in 2025, increasing throughput to 8 million tons and tightening the already-concentrated regional scrap pool. This wave of consolidation keeps the Scrap Metal Recycling Market dynamic for large buyers but leaves smaller independent players facing reduced spot availability and greater working-capital volatility.

Rising Residual Copper Contamination Limits EAF Feed Quality

The average copper content in obsolete scrap rose to 0.35% in 2025, exceeding the 0.2% threshold that most long-product EAFs can tolerate without causing color defects. ThyssenKrupp reported an additional EUR 15 per ton in melt-shop costs after installing decopperization units at its Duisburg facility. As electric vehicle wiring density increases and printed circuit boards become more prevalent, processors must either invest in robotic separation technologies or accept downgrades into lower-value products like rebar. Japan's trade ministry has introduced capital grants for automated copper extraction, aiming to reduce residual copper levels by 20% by 2028.

Other drivers and restraints analyzed in the detailed report include:

- AI-Guided LIBS and Hyperspectral Sorting Lifting Recovery Yield Above 98%

- OEM Closed-Loop Contracts for Certified Low-Residual Scrap

- Wave of National Export Restriction Laws Shrinking Tradable Pool

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ferrous metals contributed 70.82% of the 2025 throughput, driven by demand for rebar, beams, and automotive sheet. Non-ferrous metals are anticipated to grow at a CAGR of 6.22% through 2031, supported by applications such as data-center cabling, electric vehicle enclosures, and near-total battery collection in North America and Europe. Copper scrap prices rose by 18% in 2025 due to a 2.5 million-ton mine shortfall combined with strong electrification demand, boosting the premium segment of the scrap metal recycling market. Aluminum collection remains robust under beverage-can take-back laws, though lacquer contamination limits secondary alloy yields to 85% of virgin ingot levels. Lead batteries set the efficiency standard with a 99% collection rate in the United States, while titanium continues to serve niche, high-margin aerospace applications.

Grade premiums are shaping market trends. Certified low-copper ferrous scrap fetches up to USD 50 per ton more, enabling sensor-based sorting investments among top-tier yards. Non-ferrous processors observe similar trends: mill-grade aluminum trades USD 150 per ton higher than mixed turnings, and No. 1 copper achieves a 4% spot premium over No. 2 copper during peak deficit periods. As AI detection technology becomes more widespread, these price gaps are expected to narrow. However, early adopters are already capitalizing on the most lucrative opportunities within the scrap metal recycling market.

The Scrap Metal Recycling Market Report is Segmented by Metal Type (Ferrous (Iron, and Steel) Non-Ferrous (Copper, Aluminum, Lead, and Other Metal Types)), End-Use Industry (Construction, Automotive, Electrical and Electronics, Manufacturing and Industrial, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific accounted for 52.22% of the 2025 market volume and is expected to grow at a CAGR of 6.73% through 2031. China's domestic export ban redirected 8 million tons of scrap to coastal electric arc furnaces (EAFs), tightening supply in Japan and South Korea. Despite this, Japan exported 6.2 million tons, though this figure was 15% lower than its 2023 baseline. South Korea's new 2 million-ton POSCO furnace, equipped with AI sorters, has increased demand for auto-grade feed. Vietnam, Indonesia, and Malaysia are following similar trajectories, with capacity expansions absorbing surplus feeds from long-haul routes and contributing to the growth of the local scrap metal recycling market.

In North America, the United States processed 70 million tons in 2025, supported by stringent automotive take-back regulations and aging infrastructure demolitions. Commercial Metals Company operates 40 yards across the United States and Mexico. Canada primarily exported scrap to U.S. buyers, while Mexico's USMCA rules facilitated the movement of 2 million tons to Ternium's Monterrey complex. Nucor's expansion in the U.S. Midwest further tightened regional flows, highlighting the role of integrated networks in stabilizing prices within the scrap metal recycling market.

In Europe, the Circular Economy Action Plan mandates 70% demolition-waste recovery by 2030, ensuring a consistent scrap supply for long-product and flat-product mills. ArcelorMittal's partnership with Nippon Steel secures 2 million tons of captive feed. Turkey's import demand declined after licensing restrictions halved overseas sales, prompting Nordic mini-mills to rely more on regional scrap. Russia, under payment sanctions, continues to reinforce regional imbalances that impact the European scrap metal recycling market.

- AIM Recycling

- ArcelorMittal

- Aurubis AG

- Baosteel Group Corporation

- CMR Green Technologies Ltd

- COHEN

- Commercial Metals Company (CMC)

- Dowa Holdings Co. Ltd

- European Metal Recycling Ltd.

- Gerdau S/A

- Greenwave Technology Solutions Inc.

- Norton Aluminium

- OmniSource, LLC

- Remondis SE & CO. KG

- Sims Limited

- SL Recycling

- Tata Steel Limited

- The David J. Joseph Company (Nucor Corporation)

- TKC Metal Recycling Inc.

- Tom Martin Company Ltd

- Total Metal Recycling, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid EAF capacity additions in India, MENA, and Southeast Asia

- 4.2.2 Vertically-integrated mill M&A to secure captive scrap

- 4.2.3 AI-guided LIBS and hyperspectral sorting lifting recovery yield more than 98%

- 4.2.4 OEM closed-loop contracts for certified low-residual scrap

- 4.2.5 OECD push for open scrap trade to hit 2050 net-zero steel targets

- 4.3 Market Restraints

- 4.3.1 Rising residual-copper contamination limits EAF feed quality

- 4.3.2 Wave of national export-restriction laws shrinking tradable pool

- 4.3.3 Scrap price volatility widening hedge costs for SMEs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Metal Type

- 5.1.1 Ferrous

- 5.1.1.1 Iron

- 5.1.1.2 Steel

- 5.1.2 Non-Ferrous

- 5.1.2.1 Copper

- 5.1.2.2 Aluminum

- 5.1.2.3 Lead

- 5.1.2.4 Other Metal Types

- 5.1.1 Ferrous

- 5.2 By End-use Industry

- 5.2.1 Construction

- 5.2.2 Automotive

- 5.2.3 Electrical and Electronics

- 5.2.4 Manufacturing and Industrial

- 5.2.5 Consumer Appliances

- 5.2.6 Aerospace and Defense

- 5.2.7 Other End-use Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Egypt

- 5.3.5.5 South Africa

- 5.3.5.6 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AIM Recycling

- 6.4.2 ArcelorMittal

- 6.4.3 Aurubis AG

- 6.4.4 Baosteel Group Corporation

- 6.4.5 CMR Green Technologies Ltd

- 6.4.6 COHEN

- 6.4.7 Commercial Metals Company (CMC)

- 6.4.8 Dowa Holdings Co. Ltd

- 6.4.9 European Metal Recycling Ltd.

- 6.4.10 Gerdau S/A

- 6.4.11 Greenwave Technology Solutions Inc.

- 6.4.12 Norton Aluminium

- 6.4.13 OmniSource, LLC

- 6.4.14 Remondis SE & CO. KG

- 6.4.15 Sims Limited

- 6.4.16 SL Recycling

- 6.4.17 Tata Steel Limited

- 6.4.18 The David J. Joseph Company (Nucor Corporation)

- 6.4.19 TKC Metal Recycling Inc.

- 6.4.20 Tom Martin Company Ltd

- 6.4.21 Total Metal Recycling, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment