PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063231

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063231

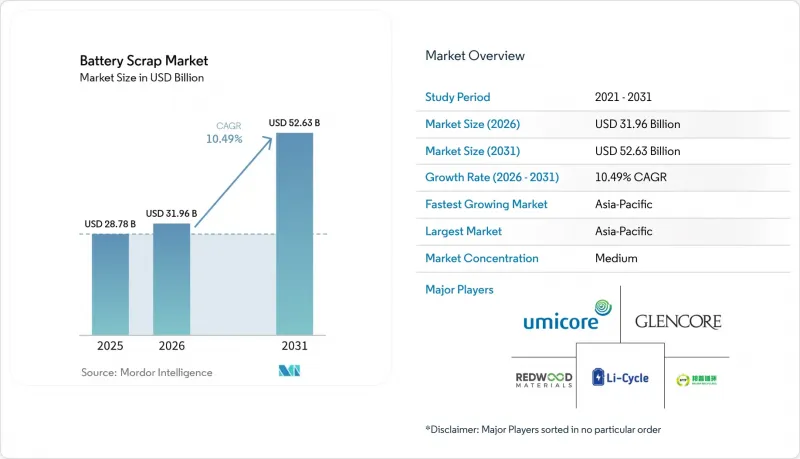

Battery Scrap - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the battery scrap market size is projected to expand from USD 28.78 billion in 2025 and USD 31.96 billion in 2026 to USD 52.63 billion by 2031, registering a CAGR of 10.49% between 2026 and 2031.

This report is Segmented by Type (Lead-Acid, Lithium-Ion, Nickel-Based, Other Chemistries), Application (Automotive, Industrial Motive-Power, Consumer Electronics, and More), End-User (Dedicated Recycling Facilities, OEM Take-Back, Utilities, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Battery Scrap Market Trends and Insights

Soaring EV-Linked Li-ion Volumes Hitting End-of-Life

The first mass-market EV batteries installed between 2015 and 2020 have begun retiring, creating a rapid upswing in lithium-ion scrap. Global EV battery demand stood near 1 TWh in 2024 and is forecast to exceed 3 TWh by 2030, yet worldwide recycling capacity totaled only 300 GWh in 2023, underscoring a structural supply imbalance . China processed more than 500,000 tons of spent Li-ion cells in 2024 and targets 300,000 tons of annual throughput by 2026 through GEM's new Jingmen line. Guangdong Brunp Recycling reported 99.6% recovery of nickel, cobalt, and manganese and 96.5% of lithium in 2024, keeping material costs 15-20% below mined equivalents. Battery retirements are forecast to climb from roughly 200 GWh in 2025 to more than 1 TWh in 2030, transforming scrap into a front-line supply source for cathode producers. Regional feedstock tightness is set to reward recyclers who lock in offtake early with automakers, cell makers, and utilities.

Mandatory Producer-Responsibility Laws in EU, China, India

Extended producer responsibility (EPR) frameworks now obligate manufacturers to fund collection and recycling, accelerating formal reverse-logistics build-outs. The EU Battery Regulation mandates 63% collection by 2027 and 90% recycling efficiency for cobalt, copper, and nickel by 2027, with recycled-content floors of 16% cobalt, 85% lead, and 6% lithium and nickel taking effect from 2031 . China's Ministry of Industry and Information Technology requires EV producers to establish take-back channels and log traceability data, stimulating partnerships between automakers and large recyclers such as GEM and Brunp. India's Battery Waste Management Rules, amended through 2025, lift recovery targets to 90% by 2026-2027 and introduce recycled-content mandates rising to 20% by 2030-2031. These policies marginalize informal collectors and channel volumes toward ISO 14001-certified facilities, pushing the battery scrap market toward industrial-scale operations.

Inefficient Global Reverse-Logistics for End-of-Life Packs

Collection and transport of spent packs remain fragmented and costly. UN 3480 and ADR classifications demand specialized packaging and labeling, inflating per-unit logistics costs by 40-60% over non-hazardous goods. Design heterogeneity forces recyclers to invest in bespoke disassembly tooling or accept lower yields from shredding-only lines. India's 2024 black-mass export restriction created bottlenecks for small collectors who lack domestic refining, while Indonesia's informal sector still handles around 30-40% of lead-acid scrap outside regulatory oversight. A comprehensive battery passport system will not arrive in the EU until February 2027, keeping traceability data siloed. Until reverse-logistics standards converge, feedstock aggregation costs will temper the growth of the battery scrap market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Black-Mass Spot Prices Improving Recycler Margins

- OEM "Closed-Loop" Offtake Contracts

- Volatile Cobalt & Nickel Prices Eroding Re-Seller Profits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lead-acid batteries supplied 61.2% of 2025 flows, anchoring the battery scrap market size with recovery rates above 99% in North America and Europe. Lithium-ion volumes, however, are projected to surge at a 22.3% CAGR to 2031 as EV retirements accelerate. Hydrometallurgical refiners deliver 90-95% metal recovery but need USD 200-500 million per commercial hub, whereas pyrometallurgical operators accept 80-85% yields for lower capital intensity. The battery scrap market share for nickel-metal-hydride cells is shrinking as hybrid vehicles transition to Li-ion, yet aerospace and defense preserve a niche demand for nickel-cadmium recycling.

Direct-cathode-regeneration is disrupting lithium-ion processing by eliminating full material breakdown and cutting costs by 30-40%. Ascend Elements' Hydro-to-Cathode line in Georgia achieves 91% recovery and reintroduces material into cell plants within weeks, shrinking working-capital cycles. ReCell Center pilots show NMC 622 scrap can regenerate NMC 811, though LFP and nickel-cobalt-aluminum variants still require separate flows. As LFP adoption rises, flexible multi-chemistry plants will determine which players retain battery scrap market share through 2031.

Geography Analysis

Asia-Pacific dominated the battery scrap market size with 49.3% of 2025 volumes and is forecast to have a 13.3% CAGR through 2031. China alone controls 80% of global recycling capacity; GEM's new 50,000-ton line pushes its total to 300,000 tons and supplies CATL and BYD under contract. India's amended Battery Waste Management Rules raise recovery targets to 90% by 2026-2027, but uneven enforcement and black-mass export bans challenge small collectors. Japan and South Korea remain technology leaders: SungEel HiTech's 600-ton cobalt plant in Saemangeum anchors regional hydrometallurgical expertise, and Sumitomo partners with Nissan on Leaf pack recycling.

Europe ranks second by value thanks to stringent regulation. Northvolt's Revolt plant reached 50,000 tons throughput in 2025 and aims for 125,000 tons by 2030. The EU Battery Passport, mandatory from February 2027, embeds QR-code traceability and recycled-content disclosure, tilting competitive advantage toward vertically integrated players. North America is catching up under the Inflation Reduction Act incentives: Redwood and Ascend Elements both scaled commercial lines in 2025, while Li-Cycle paused its Rochester hub amid cost overruns despite Glencore's USD 200 million investment in an Alabama spoke.

South America and the Middle East & Africa remain nascent. Brazil's flex-fuel car parc creates steady lead-acid flows, yet low EV penetration defers lithium-ion investment. Saudi Arabia and the UAE are evaluating recycling as part of diversification agendas, but feedstock remains scarce. Egypt's informal operators handle over half of national lead-acid volumes, with 2024 draft rules set to push formal take-back schemes. Regional disparity suggests cross-border trade in black mass will rise until domestic hubs reach scale.

- Umicore

- Li-Cycle

- Redwood Materials

- Glencore

- GEM Co., Ltd.

- Guangdong Brunp Recycling

- TES (Sims Lifecycle Services)

- Retriev Technologies

- Fortum Battery Solutions

- Ganfeng Lithium

- Stena Recycling

- Duesenfeld

- SungEel HiTech

- American Battery Technology Co.

- RecycLiCo Battery Materials

- Accurec Recycling

- Envirostream Australia

- Battery Solutions LLC

- Raw Materials Co.

- Highpower Technology

- Inobat Recycling

- EcoGraf

- Tenova

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring EV-linked Li-ion volumes hitting end-of-life

- 4.2.2 Mandatory producer-responsibility laws in EU, China, India

- 4.2.3 Growing black-mass spot prices improving recycler margins

- 4.2.4 OEM "closed-loop" offtake contracts (e.g., Tesla-Redwood)

- 4.2.5 AI-enabled scrap-stream triage boosting recovery yields

- 4.2.6 Stationary-storage repurposing delaying recycle flows

- 4.3 Market Restraints

- 4.3.1 Inefficient global reverse-logistics for end-of-life packs

- 4.3.2 Volatile cobalt & nickel prices eroding re-seller profits

- 4.3.3 Technology-lock risk from rapid cell-chemistry shifts

- 4.3.4 Fire-safety liabilities inflating insurance premiums

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Lead-Acid Battery Scrap

- 5.1.2 Lithium-ion Battery Scrap

- 5.1.3 Nickel-based Battery Scrap

- 5.1.4 Other Chemistries (NiCd, Zn-air, Solid-state pre-commercial)

- 5.2 By Application

- 5.2.1 Automotive

- 5.2.2 Industrial Motive-Power

- 5.2.3 Consumer Electronics

- 5.2.4 Stationary Energy-Storage Systems

- 5.2.5 Aerospace and Defense

- 5.2.6 Other Niche Uses (medical, maritime, mining)

- 5.3 By End-User

- 5.3.1 Dedicated Recycling Facilities

- 5.3.2 Original Equipment Manufacturers (OEM Take-Back)

- 5.3.3 Utilities and Power Producers

- 5.3.4 Third-party Waste-Management Firms

- 5.3.5 Informal/Small-scale Collectors

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Umicore

- 6.4.2 Li-Cycle

- 6.4.3 Redwood Materials

- 6.4.4 Glencore

- 6.4.5 GEM Co., Ltd.

- 6.4.6 Guangdong Brunp Recycling

- 6.4.7 TES (Sims Lifecycle Services)

- 6.4.8 Retriev Technologies

- 6.4.9 Fortum Battery Solutions

- 6.4.10 Ganfeng Lithium

- 6.4.11 Stena Recycling

- 6.4.12 Duesenfeld

- 6.4.13 SungEel HiTech

- 6.4.14 American Battery Technology Co.

- 6.4.15 RecycLiCo Battery Materials

- 6.4.16 Accurec Recycling

- 6.4.17 Envirostream Australia

- 6.4.18 Battery Solutions LLC

- 6.4.19 Raw Materials Co.

- 6.4.20 Highpower Technology

- 6.4.21 Inobat Recycling

- 6.4.22 EcoGraf

- 6.4.23 Tenova

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment