PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044106

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044106

India Pharmaceuticals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

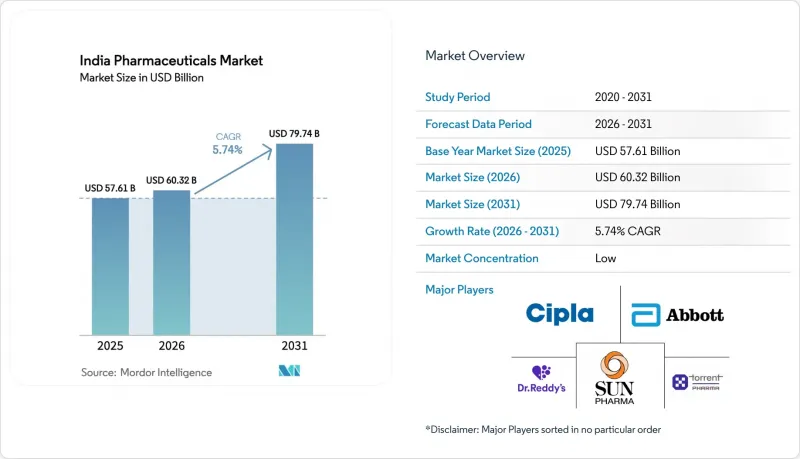

The India Pharmaceuticals Market size is projected to be USD 57.61 billion in 2025, USD 60.32 billion in 2026, and reach USD 79.74 billion by 2031, growing at a CAGR of 5.74% from 2026 to 2031.

The growth curve is underpinned by patent expiries that widen the generic pipeline, government production-linked incentives that bolster active pharmaceutical ingredient capacity, and a rapid rise in chronic diseases that ties patients to multi-year therapy plans. Anti-infectives continue to dominate day-to-day prescribing, yet oncology volumes outpace every other therapeutic class as biosimilar approvals and state-funded cancer schemes remove affordability barriers. Parallel policy shifts such as outcome-based procurement in private hospitals reward manufacturers that provide real-world evidence, while Central Drugs Standard Control Organisation's e-pharmacy rules legitimize home delivery and reinforce the "phygital" loop that links doctors, pharmacies, and digital health IDs. Competitive intensity stays moderate, creating white space for mid-tier producers that specialize in backward-integrated generics or value-added biosimilars.

India Pharmaceuticals Market Trends and Insights

Patent-Cliff of Legacy Blockbusters Fuels Generic Penetration

Blockbuster molecules that lost exclusivity between 2024 and 2026 created a USD 4 billion annual window for Indian generic makers. Sun Pharmaceutical captured 18% domestic share within six months of launching three oncology generics in 2025, while Dr. Reddy's filed 12 first-to-file abbreviated new drug applications in the United States for 2026 expiries. Contract development and manufacturing organizations compress filing timelines from 36 to 18 months by bundling bioequivalence and dossier services. Biosimilar rivalry narrows the opportunity because Biocon Biologics seized 22% of trastuzumab prescriptions by mid-2025. The competitive clock therefore pushes firms to lock in scale advantages before biosimilars cannibalize adjacent small-molecule volumes.

Government Production-Linked Incentives Accelerate Domestic API & Formulation Capacity

The production-linked incentive program disbursed INR 6,800 crore (USD 817 million) in April 2024 underwriting 53 greenfield fermentation and chemical-synthesis projects. Laurus Labs alone pledged INR 5,000 crore (USD 601 million) for antiretroviral and antidiabetic intermediates that target 40% self-sufficiency by 2027. Aurobindo Pharma revived domestic penicillin-G output, trimming Chinese dependency by 30%. Yet 18% of approved facilities missed 2025 milestones because of land acquisition and environmental hurdles, highlighting execution risk. Mid-size players such as Divi's and Piramal use the incentive to back-integrate into value-added intermediates and cushion raw-material volatility.

Frequent Retail Price Caps Under NLEM Revisions Squeeze Margins

The National Pharmaceutical Pricing Authority added 34 formulations to the essential-medicines list in 2024, trimming ceiling prices on key chronic therapies by up to 25%. Alkem Laboratories reported a 320-basis-point gross-margin contraction in fiscal 2025 after its lead antihypertensive moved under control. Eleven percent of Indian Pharmaceutical Alliance members rank price caps as their top profitability threat. The 18- to 24-month revision cycle clouds capital-planning decisions, nudging companies toward dermatology and ophthalmology niches that remain free of controls. Over time, this migration can erode economies of scale in mainstream chronic therapies.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Chronic-Disease Incidence Expands Long-Term Demand

- Pay-for-Performance Tendering by Large Hospital Chains

- Compliance Gaps with Revised Schedule M Audits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oncology leads segment growth with an 8.22% CAGR through 2031 as biosimilar trastuzumab and rituximab gain rapid uptake under state cancer schemes. Anti-infectives held the largest 34.11% share in 2025, yet stewardship programs slow volume gains to 4.8% CAGR. Cardiovascular therapies account for 22% of revenue, supported by India pharmaceuticals market size expansion in urban hypertensive cohorts, while anti-diabetic drugs serve 101 million patients. Respiratory, gastrointestinal, and analgesic lines grow in the mid-single-digit range.

The oncology upswing mirrors 1.46 million new cancer diagnoses in 2024 and the National Cancer Grid's outreach to 300 centers. Ayushman Bharat added 17 high-cost oncology drugs to its reimbursement list, cutting household spend by 55%. Anti-infective use is tempered by new over-the-counter restrictions on 39 antibiotics. Cardiovascular adherence improves because fixed-dose combinations simplify regimens; Cipla's triple combo captured 14% share in 2025. Respiratory demand climbs as Delhi and Mumbai breach World Health Organization air-quality limits on most days.

Prescription drugs contributed 61.26% of 2025 revenue, but OTC products record the quickest 7.24% CAGR amid looser scheduling and digital availability. CDSCO moved 12 molecules, including antihistamines, from prescription-only to OTC in 2024. Mankind Pharma's consumer health line grew 23% in fiscal 2025, driven by cough and digestive remedies.

OTC penetration is strongest in Tier-2 cities where pharmacy density is high and India pharmaceuticals market size gains from rising disposable incomes. Sun Pharmaceutical's OTC basket rose 18% in the same period. Price pressure emerges because supermarkets and e-commerce demand deep discounts. Prescription drugs remain dominant in chronic care and inpatient oncology, where insurance frameworks reward physician oversight. Patented molecules grow at 6.8% CAGR on biosimilar adoption, while generics advance 5.4% under price-cap strain.

The India Pharmaceuticals Market Report is Segmented by Therapeutic Area (Anti-Infectives, Cardiovascular, Anti-Diabetic, and More), Drug Type (Prescription Drugs [Patented, Generic], OTC Drugs), Formulation (Tablets, Capsules, and More), and Route of Administration (Oral and More), Distribution Channel (Hospital Pharmacies and More) and Region (West India and More). Market Forecasts are Provided in Value (USD).

List of Companies Covered in this Report:

- Abbott Laboratories

- Alkem Laboratories

- Aurobindo Pharma

- Bharat Biotech

- Biocon

- Cipla

- Dr. Reddy's Laboratories

- Glenmark Pharmaceuticals

- GSK India

- Intas Pharmaceuticals

- Johnson & Johnson Pvt. Ltd. (Janssen)

- Lupin

- Mankind Pharma

- Novartis India

- Pfizer India

- Sanofi India

- Serum Institute of India

- Sun Pharmaceuticals Industries

- Torrent Pharmaceuticals

- Zydus Lifesciences

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Patent Cliff of Legacy Blockbusters Fuels Generic Penetration

- 4.2.2 Government PLI Schemes Accelerating Domestic API & Formulation Capacity

- 4.2.3 Rapid Chronic-Disease Incidence (Diabetes, CVD) Expands Long-Term Demand

- 4.2.4 Pay-For-Performance Tendering by Large Hospital Chains

- 4.2.5 AI-Enabled Drug-Repurposing Hubs in Hyderabad & Bengaluru

- 4.2.6 Rise of "Phygital" E-Pharmacy-Doctor Ecosystems Improving Adherence

- 4.3 Market Restraints

- 4.3.1 Frequent Retail Price Caps under NLEM Revisions Squeeze Margins

- 4.3.2 Compliance Gaps with Revised Schedule M cGMP Audits

- 4.3.3 Delay in Patent Linkage System Hampers Innovative Drug Launches

- 4.3.4 Reduced Chinese Intermediate Supply Optionality Post-COVID Drives Cost Volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Therapeutic Area

- 5.1.1 Anti-infectives

- 5.1.2 Cardiovascular

- 5.1.3 Anti-diabetic

- 5.1.4 Respiratory

- 5.1.5 Oncology

- 5.1.6 Gastrointestinal

- 5.1.7 Pain / Analgesics

- 5.1.8 Others

- 5.2 By Drug Type

- 5.2.1 Prescription Drugs

- 5.2.1.1 Patented Drugs

- 5.2.1.2 Generic Drugs

- 5.2.2 OTC Drugs

- 5.2.1 Prescription Drugs

- 5.3 By Formulation

- 5.3.1 Tablets

- 5.3.2 Capsules

- 5.3.3 Injectables

- 5.3.4 Syrups / Suspensions

- 5.3.5 Others

- 5.4 By Route of Administration

- 5.4.1 Oral

- 5.4.2 Inhalational

- 5.4.3 Parental

- 5.4.4 Others

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies

- 5.5.3 Online Pharmacies

- 5.6 By Region

- 5.6.1 North India

- 5.6.2 West India

- 5.6.3 South India

- 5.6.4 East and Northeast India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Alkem Laboratories

- 6.3.3 Aurobindo Pharma

- 6.3.4 Bharat Biotech

- 6.3.5 Biocon Ltd.

- 6.3.6 Cipla Ltd.

- 6.3.7 Dr. Reddy's Laboratories

- 6.3.8 Glenmark Pharmaceuticals

- 6.3.9 GSK India

- 6.3.10 Intas Pharmaceuticals

- 6.3.11 Johnson & Johnson Pvt. Ltd. (Janssen)

- 6.3.12 Lupin Ltd.

- 6.3.13 Mankind Pharma

- 6.3.14 Novartis India

- 6.3.15 Pfizer India

- 6.3.16 Sanofi India

- 6.3.17 Serum Institute of India

- 6.3.18 Sun Pharmaceutical Industries Ltd.

- 6.3.19 Torrent Pharmaceuticals

- 6.3.20 Zydus Lifesciences

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment