PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044126

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044126

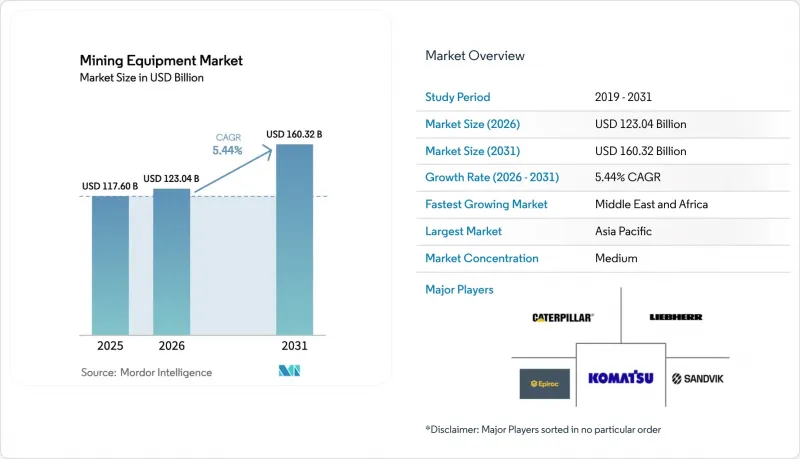

Mining Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The mining equipment market size is projected to be USD 117.60 billion in 2025, USD 123.04 billion in 2026, and reach USD 160.32 billion by 2031, growing at a CAGR of 5.44% from 2026 to 2031.

Growth is driven by brisk capital spending on battery-mineral projects, the accelerated replacement of diesel fleets in Canada, Chile, and Australia, and renewed iron-ore developments in Western Australia and Brazil. Surface fleets continue to dominate procurement budgets, yet underground loaders and drill rigs are scaling rapidly as lithium and copper ore bodies move deeper and narrower. Financing linked to verified emission reductions is saving 150-200 basis points from lease rates on zero-emission trucks, further tilting demand toward battery-electric models. Competitive pressure is intensifying as XCMG and SANY underprice Western OEMs, while Caterpillar and Komatsu defend share through proprietary digital platforms that lock customers into bundled service contracts.

Global Mining Equipment Market Trends and Insights

Surging Demand for Critical Minerals for Battery Supply Chains (Asia and United States)

Lithium, cobalt, and nickel expansions are reshaping procurement, as battery-metal mines require high-throughput crushers and flotation cells distinct from base-metal circuits. Chilean brine projects now deploy solar-powered pumps that cut diesel use significantly, whereas Western Australia's hard-rock lithium sites specify above 1,000-horsepower haul trucks to manage spodumene densities higher than iron ore. In the United States, the Inflation Reduction Act sourcing rules steer buyers toward Caterpillar and Komatsu to capture domestic-content tax credits. Congolese cobalt projects are upgrading from manual excavators to semi-autonomous loaders to meet traceability rules, and Indonesian nickel laterite operators are installing rotary kilns and electric arc furnaces that create an addressable market for mineral-processing equipment. These factors push the mining equipment market toward specialized, higher-margin systems that command pricing power despite broader cost pressure.

Accelerated Mine Electrification Mandates in Canada, Chile and Australia

Canada requires underground mines to field zero-emission units for at least 50% of mobile fleets, rising to 75% by 2030 . New South Wales rolled out a ventilation-cost levy, leveling the playing field for battery-electric loaders at significant depths. As a result of these policies, operators are now retiring diesel assets much earlier than anticipated, leading to a surge in demand for Epiroc's ST18 Battery and Sandvik's LH518B. Additionally, lenders are now mandating ISO 14001-compliant transition plans as a prerequisite for disbursement of funds, underscoring the growing nexus between decarbonization efforts and capital accessibility.

Ore-Grade Deterioration Inflating Total Cost-Of-Ownership

In 2024, copper grades at Escondida have declined, prompting BHP to move significantly more waste material and substantially increase tire usage. Similarly, gold grades in West Africa have also dropped, leading to a notable rise in ore processing through crushers. Lower grades amplify the costs of downtime; for example, a haul-truck malfunction at a low-grade copper pit now results in significant losses. In response, operators are opting for larger-payload trucks to extend component lifespan. However, this approach significantly raises initial capital investment and reduces returns. While in-pit crushing and conveying provides a potential solution, it depends on long-term reserve certainty, which many deposits currently lack.

Other drivers and restraints analyzed in the detailed report include:

- Sustained Capex Up-Cycle in African Copper, Cobalt and Lithium Projects

- Recovery of Greenfield Iron-Ore Projects in Western Australia and Brazil

- Grid Constraints at Remote Mines Delaying BEV Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mining trucks captured 59.22% of the mining equipment market share in 2025, cementing their status as the single-largest revenue contributor to the overall mining equipment market. Ultra-class haulage remains indispensable at large copper and iron-ore pits where payloads exceed 360 tonnes and haul distances stretch beyond 5 kilometers. Despite this dominance, procurement managers are trimming absolute truck counts by 15-20% in autonomous fleets, reallocating capital toward high-precision peripheral gear that maximizes cycle efficiency.

Drills and breakers are projected to post a 6.91% CAGR from 2026 to 2031, the fastest rate among equipment types, as deeper, harder orebodies boost demand for high-power rotary rigs, long-hole drills, and rock-breakers that can operate reliably in 200 megapascal ground. Autonomous drilling systems add a further productivity kicker by delivering tighter blast fragmentation, reducing downstream energy needs in crushing circuits. This shift reshapes procurement strategies: operators are bundling truck orders with drill-automation packages to secure integrated dispatch and data analytics support. This pattern strengthens OEM cross-selling leverage within the mining equipment market.

Manual fleets held 81.65% of the mining equipment market share in 2025, yet fully autonomous units had notably higher availability compared to their manned counterparts, resulting in considerably more annual running hours per unit. Fully autonomous equipment is set to grow at a 15.01% CAGR by 2031. The mining equipment market is witnessing a rapid expansion in autonomous systems, driven by insurers offering substantial premium reductions for accident-free records. The industry is shifting away from semi-autonomous solutions toward fully driverless systems, driven by superior data clarity and reduced training requirements.

Manual gear persists in artisanal and union-sensitive jurisdictions, and underground latency issues limit manual oversight in narrow areas. Regulatory inertia outside Australia, Canada, and Chile slows approvals, but once frameworks are codified, suppressed demand could trigger a step-change. Battery-electric drive trains align naturally with autonomy because instant torque and fewer mechanical parts simplify control logic, strengthening the virtuous cycle between electrification and automation.

The Mining Equipment Market Report is Segmented by Equipment Type (Loaders, Excavators, and More), Automation Level (Manual Equipment, and More), Powertrain Type (Internal-Combustion Engine Vehicles, and More), Power Output (Less Than 500 HP, and More) Application (Metal Mining and More), Mining Type (Surface Mining and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

The Asia-Pacific region maintained a 59.35% mining equipment market share in 2025, buoyed by Chinese coal mechanization, Indonesian nickel growth, and Indian iron-ore upgrades. Chinese fleet renewals plateau as coal volumes stabilize and emission rules tighten, but Indonesia ordered several haul trucks to feed stainless-steel capacity. Australia transitions from expansion to replacement demand, swapping diesel for autonomous BEVs to meet 2030 targets. Japan and South Korea import most of their equipment, yet their domestic firms-Komatsu, Hitachi, and Hyundai-export a notable share of their output.

The Middle East and Africa region is poised for an 8.04% CAGR through 2031, driven by Saudi phosphate, South African platinum modernization, and Congolese copper. Recently, Ma'aden placed the region's most significant single order, securing a substantial number of Caterpillar 795F AC trucks for Wa'ad Al Shamal. Responding to South Africa's upcoming diesel particulate limits, Impala Platinum made a strategic move by ordering a significant number of Sandvik BEV loaders. Meanwhile, DRC's Kamoa-Kakula is pioneering energy innovation in frontier markets, operating autonomous trucks powered by a solar-plus-battery microgrid.

North America trends toward replacement spending and autonomy retrofits. In Canada, Newmont's Borden was positioned as an all-electric underground gold mine, highlighting the direction of fleet electrification.

Whereas in South America, Chile, copper pits are adopting trolley assists, achieving a considerable reduction in diesel consumption per ton hauled. Brazil is bolstering its iron-ore capacity, with additional Liebherr T 284s set to arrive over the next few years. However, Europe is facing challenges: recently, no greenfield hard-rock mine secured financial closure due to regulatory uncertainties, stalling capital influx. These regional disparities highlight the significant impact of policy and commodity dynamics on the mining equipment market.

- Caterpillar Inc.

- Komatsu Ltd.

- Sandvik AB

- Liebherr-International AG

- Epiroc AB

- Hitachi Construction Machinery Co., Ltd.

- Atlas Copco AB

- Volvo Construction Equipment AB

- Metso Outotec Oyj

- Doosan Infracore Co.

- BEML Ltd.

- XCMG Group

- SANY Heavy Equipment

- Hyundai Construction Equipment Co.

- Terex Corporation

- Joy Global (Komatsu Mining)

- CNH Industrial N.V.

- JCB Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Critical Minerals for Battery Supply Chains (Asia and US)

- 4.2.2 Accelerated Mine Electrification Mandates in Canada, Chile and Australia

- 4.2.3 Sustained CAPEX Up-Cycle in African Copper, Cobalt and Lithium Projects

- 4.2.4 Emissions-Linked Financing Lowering Cost of Capital for Electric Fleets

- 4.2.5 Recovery of Greenfield Iron-Ore Projects in Western Australia and Brazil

- 4.2.6 Shift To Predictive Maintenance Driving Aftermarket Parts Pull-Through

- 4.3 Market Restraints

- 4.3.1 Ore-Grade Deterioration Inflating Total Cost-Of-Ownership

- 4.3.2 Grid Constraints at Remote Mines Delaying BEV Deployment

- 4.3.3 Talent Shortage for Autonomous Haul-Truck Operations

- 4.3.4 Uneven Permitting Timelines for New Surface Mines (EU and US)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Equipment Type

- 5.1.1 Surface Mining Equipment

- 5.1.2 Underground Mining Equipment

- 5.1.3 Mineral Processing Equipment

- 5.1.4 Drills and Breakers

- 5.1.5 Crushing, Pulverizing and Screening

- 5.1.6 Loaders and Haul Trucks

- 5.2 By Automation Level

- 5.2.1 Manual Equipment

- 5.2.2 Semi-Autonomous Equipment

- 5.2.3 Fully Autonomous Equipment

- 5.3 By Powertrain Type

- 5.3.1 Internal-Combustion Engine Vehicles

- 5.3.2 Battery-Electric Vehicles

- 5.3.3 Hybrid Vehicles

- 5.4 By Power Output

- 5.4.1 Less than 500 HP

- 5.4.2 500 - 1,000 HP

- 5.4.3 Above 1,000 HP

- 5.5 By Application

- 5.5.1 Metal Mining

- 5.5.2 Mineral Mining

- 5.5.3 Coal Mining

- 5.6 By Mining Type

- 5.6.1 Surface Mining

- 5.6.2 Underground Mining

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Chile

- 5.7.2.3 Peru

- 5.7.2.4 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Spain

- 5.7.3.5 Sweden

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Indonesia

- 5.7.4.6 Rest of Asia

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Democratic Republic of Congo

- 5.7.6.3 Zambia

- 5.7.6.4 Rest of Africa

- 5.7.7 Oceania

- 5.7.7.1 Australia

- 5.7.7.2 New Zealand

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Komatsu Ltd.

- 6.4.3 Sandvik AB

- 6.4.4 Liebherr-International AG

- 6.4.5 Epiroc AB

- 6.4.6 Hitachi Construction Machinery Co., Ltd.

- 6.4.7 Atlas Copco AB

- 6.4.8 Volvo Construction Equipment AB

- 6.4.9 Metso Outotec Oyj

- 6.4.10 Doosan Infracore Co.

- 6.4.11 BEML Ltd.

- 6.4.12 XCMG Group

- 6.4.13 SANY Heavy Equipment

- 6.4.14 Hyundai Construction Equipment Co.

- 6.4.15 Terex Corporation

- 6.4.16 Joy Global (Komatsu Mining)

- 6.4.17 CNH Industrial N.V.

- 6.4.18 JCB Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment