PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044261

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044261

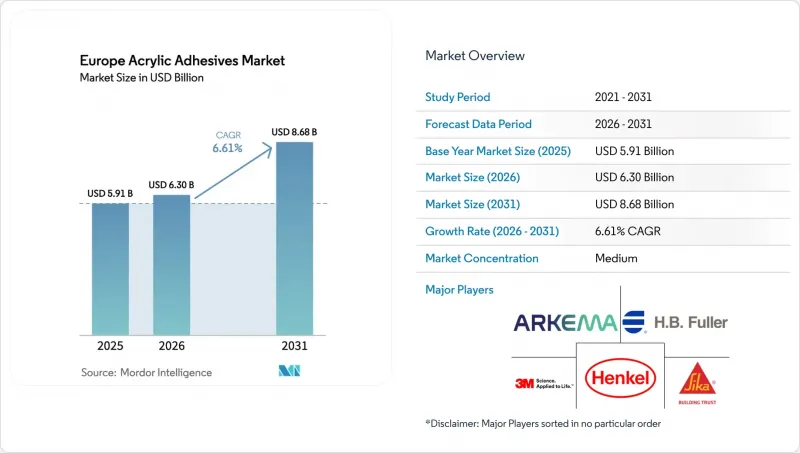

Europe Acrylic Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe Acrylic Adhesives Market size is expected to increase from USD 5.91 billion in 2025 to USD 6.30 billion in 2026 and reach USD 8.68 billion by 2031, growing at a CAGR of 6.61% over 2026-2031. Product demand benefits from e-commerce packaging, vehicle lightweighting, and retrofit construction incentives that collectively lift volumes and improve average selling prices. Regulatory changes that tighten volatile-organic-compound (VOC) thresholds accelerate the switch to low-VOC water-borne chemistries, prompting suppliers to re-engineer supply chains for compliant monomers and emulsifiers. Integrated producers with backward linkages into methyl-methacrylate and butyl-acrylate feedstocks retain a cost edge, while mid-tier converters win volume with tailored formulations for niche substrates. Portfolio rationalization, technical-service support, and rapid scale-up capacity remain decisive competitive factors as buyers consolidate supplier bases to secure on-time deliveries and regulatory documentation.

Europe Acrylic Adhesives Market Trends and Insights

Shift Toward Water-Borne Acrylics Under European Union VOC Limits

Revised EU VOC ceilings, announced late 2025 and effective mid-2026, compel formulators to audit every solvent-borne stock-keeping unit, accelerate pilot runs of compliant water-borne grades, and certify new raw-material supply chains. Early movers that publish third-party life-cycle assessments secure preferential scores in public tenders and hospitality refurbishments that weight low-emission products higher. Installers need retraining because emulsion systems exhibit longer open time and altered rheology, yet their near-zero odor profile reduces indoor-air re-occupancy delays. Packaging groups have already trialed hybrid acrylic UV-emulsion chemistries that meet both productivity and compliance targets. Collectively, the legislative push adds a visible 1.8 percentage-point uplift to the forecast CAGR of the Europe Acrylic Adhesives market.

E-Commerce Packaging Boom Driving PSA Demand

Online retail migration propels demand for corrugated labels, flexible films, and resealable pouches that rely on pressure-sensitive acrylic emulsions for consistent tack across cardboard, polyethylene, and metallized substrates. RFID tags and smart-label sensors increasingly specify low-migration acrylics that remain stable through multi-temperature logistics cycles. Brand owners favor water-borne grades that facilitate fiber-to-fiber recycling and reduce de-inking steps, aligning with EU circular-economy directives. European converters report line-speed gains of up to 12% after switching to next-generation emulsion PSAs, supporting a 1.5 percentage-point boost to overall growth in the Europe Acrylic Adhesives market.

Acrylic-Monomer Price Volatility

Scheduled cracker turnarounds and spot acetone tightness have historically triggered double-digit quarterly swings in methyl-methacrylate pricing. Although late-2025 oversupply cooled quotations, buyers remain wary and shift toward formula-based contracts or dual sourcing from fully integrated suppliers. Feedstock swings of +-10% compress formulators' margins, delaying discretionary investments and shaving 0.8 percentage-points off the Europe acrylic adhesives market growth potential in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweighting and Mixed-Material Bonding

- EU Renovation Wave Spurring Facade-Insulation Adhesives

- VOC-Compliance Costs for Solvent Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Packaging accounted for 59.56% of the Europe Acrylic Adhesives market share in 2025, supported by escalating parcel volumes and flexible-film lamination lines running at record utilization. The segment is expected to retain leadership through 2031 as brand owners migrate to mono-material structures that rely on high-clarity acrylic emulsions. Arkema's late-2024 acquisition of Dow's flexible-packaging adhesive assets immediately lifted Bostik's European footprint and secured backward integration into performance resins. Medical packaging and pharmaceutical blister labels further reinforce baseline demand, ensuring the Europe Acrylic Adhesives market size for packaging expands steadily across the forecast years.

Automotive, while contributing a smaller base, is forecast to grow fastest at 6.72% CAGR on the back of battery module assembly, lightweight body-in-white bonding, and electromobility investments. Vehicle platforms aggressively cut weight to extend driving range, and OEMs (Original Equipment Manufacturers) validate acrylic tapes for mixed-metal joints that tolerate differential thermal expansion. Strategic sourcing arrangements signed by German automakers secure multi-year capacity reservations, creating a visible growth pipeline for the Europe acrylic adhesives market within the mobility value chain.

The Europe Acrylic Adhesives Market Report is Segmented by End-User Industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, and More), Technology (Reactive, Solvent-Borne, UV-Cured Adhesives, and Water-Borne), and Country (Australia, China, India, Indonesia, Malaysia, Singapore, South Korea, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corporation

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI S.p.A.

- Sika AG

- Soudal Holding N.V.

- BASF

- Dymax Corporation

- ITW Performance Polymers

- PARKER HANNIFIN CORP

- Lohmann

- Hoenle AG

- Parson Adhesives, Inc.

- Novatech International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift toward water-borne acrylics under European Union VOC limits

- 4.2.2 E-commerce packaging boom driving PSA demand

- 4.2.3 Automotive lightweighting and mixed-material bonding

- 4.2.4 European Union "Renovation Wave" spurring facade-insulation adhesives

- 4.2.5 Wind-turbine blade refurbishment using structural acrylics

- 4.3 Market Restraints

- 4.3.1 Acrylic-monomer price volatility

- 4.3.2 VOC-compliance costs for solvent systems

- 4.3.3 Bio-based polyurethane dispersions cannibalising share

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Distribution Channel Analysis

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-user Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 By Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV-cured

- 5.2.4 Water-borne

- 5.3 By Country

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Russia

- 5.3.7 NORDIC Countries

- 5.3.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 Dow

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Huntsman International LLC

- 6.4.8 MAPEI S.p.A.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

- 6.4.11 BASF

- 6.4.12 Dymax Corporation

- 6.4.13 ITW Performance Polymers

- 6.4.14 PARKER HANNIFIN CORP

- 6.4.15 Lohmann

- 6.4.16 Hoenle AG

- 6.4.17 Parson Adhesives, Inc.

- 6.4.18 Novatech International

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment