PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044271

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044271

India Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

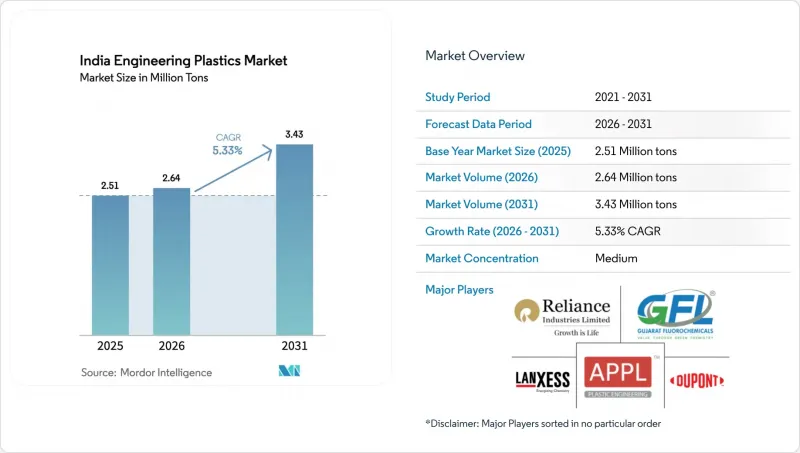

The Indian Engineering Plastics Market size is expected to grow from 2.51 million tons in 2025 to 2.64 million tons in 2026 and is forecast to reach 3.43 million tons by 2031 at 5.33% CAGR over 2026-2031.

Demand for rigid and flexible packaging remains robust across the beverage, food, and e-commerce sectors. However, there is a notable pivot towards premium components in the electrical, electronics, and mobility domains. Government initiatives, such as the Production Linked Incentive (PLI) outlays, alongside a growing electric vehicle (EV) production base and stringent recycled content mandates, have drastically accelerated resin-adoption cycles. What previously required nearly a decade has now been reduced to approximately five years. This swift transition is highlighted by the expanding grades in flame-retardant polyamides, polycarbonate-ABS blends, and fluoropolymers. Between 2026 and 2031, domestic capacity expansions have focused on PET, ABS, and standard polyamide 6. However, India continues to depend on imports for a considerable portion of its specialty polymers. This reliance makes converters vulnerable to foreign exchange fluctuations and potential shipping delays.

India Engineering Plastics Market Trends and Insights

Automotive Light-Weighting and Electric-Vehicle Adoption Boom

From 2024 to 2033, India's EV sales are projected to surge, driving up the demand for polymers in vehicles. OEMs are increasingly opting for materials such as glass-fiber-reinforced polyamide 66, polyphthalamide, and flame-retardant polycarbonate-ABS, replacing traditional metal housings. This shift not only reduces curb weight but also enhances the EV driving range, making it a pivotal choice for battery enclosures, power-electronics modules, and thermal-management manifolds. Tata Motors and Mahindra are leading the charge, specifying a higher content of engineering plastics in their new EV platforms, which doubles the content used in comparable internal-combustion models. While domestic production of PA 66 faces capacity constraints, the value-chain players are turning to imports for intermediates such as caprolactam and adipic acid. This reliance on imports tempers potential cost reductions, even with Bhansali Engineering Polymers planning an expansion set to conclude in 2028. Starting in 2027, the Bureau of Energy Efficiency is tightening Corporate Average Fuel Economy (CAFE) norms. This policy is expected to further accelerate the shift from plastic to metal in components such as door modules, instrument clusters, and seat structures.

Government PLI Incentives for Specialty Polymers

By December 2025, disbursements under the PLI scheme reached significant levels, leading to the establishment of multiple greenfield projects in corridors focused on electronics, batteries, and specialty chemicals. Major players such as Foxconn, Samsung, and Tata Electronics are committed to sourcing components, including polycarbonate housings, liquid-crystal-polymer connectors, and PVDF binders, from domestic markets. This marked a significant shift from their earlier reliance on imports. The Advanced Chemistry Cell PLI, with substantial funding, created a considerable demand for PVDF and PTFE annually for applications such as cathode binders and separator coatings. The Dahej-Vadodara belt in Gujarat and the Bengaluru cluster in Karnataka experienced the most momentum. In these regions, land subsidies and favorable power tariffs enabled resin manufacturers to reduce operating costs. Notably, mobile-phone import volumes had significantly declined since FY 2020-21, underscoring the potential of localization efforts to reshape trade balances within a single investment cycle.

Feedstock Price Volatility (PX, Benzene, HF)

Paraxylene prices have exhibited significant fluctuations, and benzene prices have also experienced notable swings in a short timeframe. These price movements have compressed margins for polyester and polyamide producers. In a bid to safeguard their spreads, Reliance Industries and Gujarat State Fertilizers & Chemicals transitioned from quarterly to monthly price adjustments. However, this shift has strained their working capital, adversely affecting downstream operations. Meanwhile, hydrofluoric acid, a critical feedstock for PTFE and PVDF production, has experienced a tightening supply due to new environmental restrictions implemented in China. As a result, Gujarat Fluorochemicals has entered into multi-year supply contracts at a premium over previous averages. Furthermore, smaller compounders, who typically do not hedge, postponed their new extrusion lines by several months. This postponement has hindered the commercialization of resin grades for emerging applications, including 5G antennas and EV battery seals.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Electronics Manufacturing

- Food-Grade rPET Mandate for Beverage Bottles

- Compliance Costs from EPR and Recycled-Content Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, packaging took the lead in India's engineering plastics market, securing a commanding 57.12% share. This upswing was fueled by a dynamic domestic packaging sector, skillfully addressing the needs of swift urbanization, food delivery services, and organized retail. As companies in the soft drink, water, and dairy sectors geared up for the rPET mandate, production of PET bottles saw a consistent rise. Flexible multi-layer films, now a significant segment of total packaging tonnage, are enhanced with EVOH and polyamide barriers to extend the shelf life of snack foods. Although electronics manufacturing represented a smaller slice of the 2025 volume, it is set to expand at an 8.55% CAGR through the 2026-2031 forecast period. This anticipated growth is driven by PLI incentives that bolster the domestic assembly of smartphones, white goods, and wearables. Each addition of a PCB or printed antenna notably heightens the demand for high-temperature LCP and PBT. The automotive sector is ramping up its polymer usage for electric vehicles (EVs), favoring optical-grade polycarbonate for components like battery packs, electrical connectors, and exterior glazing, moving away from traditional materials. The construction sector, leveraging CPVC pipes, PMMA glazing, and polycarbonate roofing, is a major consumer, spurred by initiatives like the Smart Cities Mission and PM Awas Yojana housing projects.

As e-commerce trends evolve, there is a noticeable shift in packaging towards lighter, recyclable formats. This evolution has spotlighted niches for monomaterial glycol-modified PET and polyolefin-based barrier films. Brand owners' push for tamper-evident bottles and laser-engraved closures has spiked the demand for specialty polyacetal and thermoplastic elastomers. The electronics sector, closely tied to major players like Apple and Samsung, has seen a marked decrease in the country's dependence on imported flame-retardant ABS. The automotive industry's drive for lightweight components has led to a surge in demand for glass-fiber-reinforced PA 66 and polyphthalamide engine covers. Additionally, impact-modified polycarbonate is becoming the go-to for two-wheeler battery casings. With a construction boom underway, especially in municipal water projects, there has been a notable uptick in the demand for CPVC and UPVC pipes. Industrial machinery, from bearings to conveyor systems, is increasingly opting for low-friction POM and aramid-reinforced PA 6 to boost wear resistance, though there is still a significant dependence on imports for advanced grades.

The India Engineering Plastics Market Report is Segmented by End-User Industry (Automotive, Electrical and Electronics, Building and Construction, Packaging, Industrial and Machinery, Aerospace, and Other End-User Industries), Resin Type (Fluoropolymers, Liquid Crystal Polymer, Polyamide, Polybutylene Terephthalate, Polycarbonate, Polyether Ether Ketone, and More). Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- APPL Industries Limited

- Bhansali Engineering Polymers Ltd.

- DuPont

- Gujarat Fluorochemicals Limited (GFL)

- Gujarat State Fertilizers & Chemicals Limited (GSFC)

- INEOS

- IVL Dhunseri Petrochem Industries Private Limited (IDPIPL)

- Kingfa Science & Technology (India) Limited

- LANXESS

- Mitsubishi Chemical Group

- Polyplex Corporation Ltd.

- Reliance Industries Ltd

- Styrenix Performance Materials Limited

- JBF Industries Ltd

- CHIRIPAL POLY FILM

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automotive Light-weighting and Electric Vehicle Adoption Boom

- 4.2.2 Government PLI Incentives for Specialty Polymers

- 4.2.3 Surge in Electronics Manufacturing

- 4.2.4 Food-grade rPET Mandate for Beverage Bottles

- 4.2.5 Rapid Growth of Technical-textile and Fiber Exports

- 4.3 Market Restraints

- 4.3.1 Feedstock Price Volatility (PX, Benzene, HF)

- 4.3.2 Compliance Costs from EPR and Recycled-content Rules

- 4.3.3 Under-investment in Certified Recycling Infrastructure

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of Substitutes

- 4.6.4 Competitive Rivalry

- 4.6.5 Threat of New Entrants

- 4.7 Import and Export Trends

- 4.7.1 Fluoropolymer Trade

- 4.7.2 Polyamide (PA) Trade

- 4.7.3 Polyethylene Terephthalate (PET) Trade

- 4.7.4 Polymethyl Methacrylate (PMMA) Trade

- 4.7.5 Polyoxymethylene (POM) Trade

- 4.7.6 Styrene Copolymers (ABS and SAN) Trade

- 4.8 Price Trends

- 4.8.1 Fluoropolymer

- 4.8.2 Polycarbonate (PC)

- 4.8.3 Polyethylene Terephthalate (PET)

- 4.8.4 Polyoxymethylene (POM)

- 4.8.5 Polymethyl Methacrylate (PMMA)

- 4.8.6 Styrene Copolymers (ABS and SAN)

- 4.8.7 Polyamide (PA)

- 4.9 Recycling Overview

- 4.9.1 Polyamide (PA) Recycling Trends

- 4.9.2 Polycarbonate (PC) Recycling Trends

- 4.9.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.9.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.10 Licensors Overview

- 4.11 Production Overview

- 4.12 End-use Sector Trends

- 4.12.1 Aerospace (Aerospace Component Production Revenue)

- 4.12.2 Automotive (Automobile Production)

- 4.12.3 Building and Construction (New Construction Floor Area)

- 4.12.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.12.5 Packaging (Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Volume)

- 5.1 By End-User Industry

- 5.1.1 Automotive

- 5.1.2 Electrical and Electronics

- 5.1.3 Building and Construction

- 5.1.4 Packaging

- 5.1.5 Industrial and Machinery

- 5.1.6 Aerospace

- 5.1.7 Other End-User Industries

- 5.2 By Resin Type

- 5.2.1 Fluoropolymers

- 5.2.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.4 Polyvinylfluoride (PVF)

- 5.2.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer

- 5.2.3 Polyamide

- 5.2.3.1 Aramid

- 5.2.3.2 Polyamide (PA) 6

- 5.2.3.3 Polyamide (PA) 66

- 5.2.3.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate

- 5.2.5 Polycarbonate

- 5.2.6 Polyether Ether Ketone

- 5.2.7 Polyethylene Terephthalate

- 5.2.8 Polyimide

- 5.2.9 Polymethyl Methacrylate

- 5.2.10 Polyoxymethylene

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 APPL Industries Limited

- 6.4.2 Bhansali Engineering Polymers Ltd.

- 6.4.3 DuPont

- 6.4.4 Gujarat Fluorochemicals Limited (GFL)

- 6.4.5 Gujarat State Fertilizers & Chemicals Limited (GSFC)

- 6.4.6 INEOS

- 6.4.7 IVL Dhunseri Petrochem Industries Private Limited (IDPIPL)

- 6.4.8 Kingfa Science & Technology (India) Limited

- 6.4.9 LANXESS

- 6.4.10 Mitsubishi Chemical Group

- 6.4.11 Polyplex Corporation Ltd.

- 6.4.12 Reliance Industries Ltd

- 6.4.13 Styrenix Performance Materials Limited

- 6.4.14 JBF Industries Ltd

- 6.4.15 CHIRIPAL POLY FILM

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs