PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044272

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044272

Japan Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

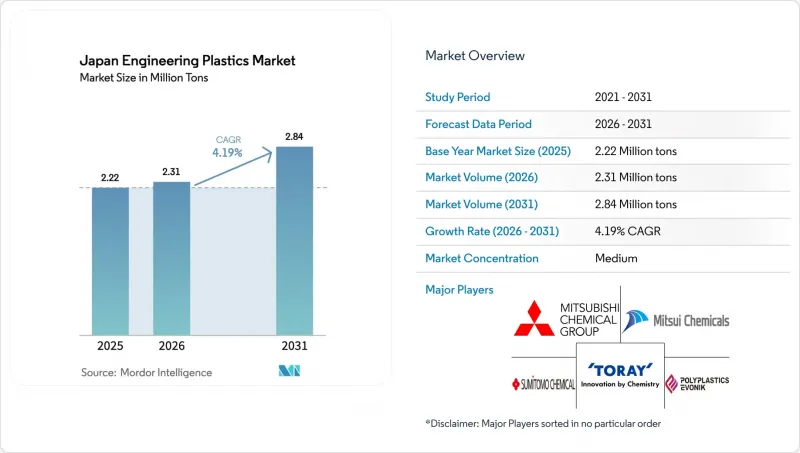

The Japan Engineering Plastics Market size is projected to be 2.22 million tons in 2025, 2.31 million tons in 2026, and reach 2.84 million tons by 2031, growing at a CAGR of 4.19% from 2026 to 2031.

Demand is shifting from commodity polyolefins to specialty grades that serve 5G infrastructure, medical implants, and hydrogen-electrolysis equipment as domestic producers retreat from volumes that compete head-on with low-priced imports. Japan's value chain is migrating away from Chubu's automotive stamping plants toward Kanto's semiconductor packaging lines and metropolitan clean rooms that manufacture high-added-value medical devices. Investment is concentrating in fluoropolymers, polyimide films, and PFAS-free tribological polyamides because these niches are insulated from Chinese overcapacity and enjoy pricing power. Meanwhile, consolidation among commodity producers and injection molders is squeezing marginal players, creating wider spreads between high-performance resins and bulk grades.

Japan Engineering Plastics Market Trends and Insights

Surge in 5G and Advanced Semiconductor Packaging

Japan's drive for semiconductor sovereignty is redirecting more than 15,000 tons per year of high-purity fluoropolymers into plasma-etch chambers and chemical-delivery tubing. AGC's JPY 35 billion expansion at Chiba, completed in 2025, increased Ethylenetetrafluoroethylene (ETFE) and Polyvinylidene Fluoride (PVDF) capacity expressly for this demand. TOPPAN and Kyocera have ramped ultra-thin polyimide films below 10 µm for advanced IC substrates, a niche that commands three to five times the margin of automotive resins. UBE is doubling polyimide capacity by 2030 as it exits commodity nylon. These moves tilt the Japan engineering plastics market toward low-dielectric, heat-resistant polymers that Chinese competitors cannot yet mass-produce at required purity levels.

Aging-Society Demand for Medical Devices

Twenty-eight-point-six percent of Japan's population is over 65, transforming medical devices into a structural growth pillar. The Ministry of Health, Labour and Welfare approved 47 new device classifications in 2025 that rely on ISO-10993-compliant polymers. Polyether Ether Ketone (PEEK) and polysulfone are taking share in spinal implants and dialysis membranes because they enable MRI-compatible and chemically robust solutions that metals cannot offer. Asahi Kasei is doubling PIMEL polyimide capacity by 2030 to support minimally invasive surgical tools. Such clinical innovation decouples resin demand from GDP, linking growth instead to procedure adoption curves that favor high-margin biocompatible grades.

Automotive Output Contraction 2023-24

Monthly vehicle output fell to 587,348 units in November 2025, far below historical peaks, and Japan Auto Parts Industries Association (JAPIA) recorded 36 supplier bankruptcies in 2024. The slump hits commodity PP and ABS hardest, but it also crimps demand for PA66 intake manifolds and PC headlamp lenses. Surviving molders such as the newly formed GMS Group (created by the April 2026 Nissei Plastic-TOYO Innobex merger) now control larger shares of downstream conversion capacity, slowing diffusion of next-generation resins.

Other drivers and restraints analyzed in the detailed report include:

- Recycling and Circular-Economy Compliance Mandates

- PFAS Phase-Out Enabling PA Tribological Grades

- PFAS Regulatory Uncertainty for Fluoropolymers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Packaging held 28.89% of Japan Engineering Plastics market share in 2025, driven by beverage and food applications that consumed 640,000 tons of PET, PP, and PS. Electrical and Electronics is forecast to grow at a 6.37% CAGR during the forecast period (2026-2031), propelled by a 17% surge in domestic IC output as Rapidus and TSMC fabs ramp capacity. Automotive remains volume-heavy but is losing relative weight; however, each EV integrates 30-40 kg of high-performance PPS, PPA, and PEEK versus 15-20 kg in internal-combustion cars, cushioning the Japan Engineering Plastics market size for this segment.

Hospitals' shift to single-use devices and robotic platforms is boosting medical applications of radiolucent PEEK and sterilization-resistant PSU. Building and Construction demand for PVC profiles and PC glazing is stabilizing alongside residential starts, while Industrial Machinery is pacing 3-4% annual growth as factories digitize. Aerospace, though small, benefits from NEDO-funded composite programs that favor high-temperature polyimides and carbon-fiber-reinforced thermoplastics.

The Japan Engineering Plastics Market Report is Segmented by Resin Type (Fluoropolymer, Liquid Crystal Polymer, Polyamide, Polybutylene Terephthalate, Polycarbonate, Polyether Ether Ketone, Polyimide, Polymethyl Methacrylate, and More) and End-User Industry (Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- AGC Inc.

- Asahi Kasei

- Daicel Corporation

- Daikin Industries Ltd.

- Idemitsu Kosan Co., Ltd.

- Kaneka Corporation

- Kuraray Co., Ltd.

- Kureha Corporation

- MCT PET Resin Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals, Inc.

- PBI Advanced Materials Co., Ltd.

- Polyplastics-Evonik Corporation

- Sumitomo Chemical Co., Ltd.

- Techno-UMG Co., Ltd.

- Teijin Limited

- TORAY INDUSTRIES INC.

- UBE Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in 5G and advanced semiconductor packaging

- 4.2.2 Ageing-society demand for medical devices

- 4.2.3 Recycling and circular-economy compliance mandates

- 4.2.4 PFAS phase-out enabling PA tribological grades

- 4.2.5 Cloud-based polymer CAE boosting high-turnover SKUs

- 4.3 Market Restraints

- 4.3.1 Automotive output contraction 2023-24

- 4.3.2 PFAS regulatory uncertainty for fluoropolymers

- 4.3.3 Shrinking domestic injection-molding SME base

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of Substitutes

- 4.6.4 Competitive Rivalry

- 4.6.5 Threat of New Entrants

- 4.7 Import and Export Trends

- 4.7.1 Fluoropolymer Trade

- 4.7.2 Polyamide (PA) Trade

- 4.7.3 Polyethylene Terephthalate (PET) Trade

- 4.7.4 Polymethyl Methacrylate (PMMA) Trade

- 4.7.5 Polyoxymethylene (POM) Trade

- 4.7.6 Styrene Copolymers (ABS and SAN) Trade

- 4.8 Price Trends

- 4.8.1 Fluoropolymer

- 4.8.2 Polycarbonate (PC)

- 4.8.3 Polyethylene Terephthalate (PET)

- 4.8.4 Polyoxymethylene (POM)

- 4.8.5 Polymethyl Methacrylate (PMMA)

- 4.8.6 Styrene Copolymers (ABS and SAN)

- 4.8.7 Polyamide (PA)

- 4.9 Recycling Overview

- 4.9.1 Polyamide (PA) Recycling Trends

- 4.9.2 Polycarbonate (PC) Recycling Trends

- 4.9.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.9.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.10 Licensors Overview

- 4.11 Production Overview

- 4.12 End-use Sector Trends

- 4.12.1 Aerospace (Aerospace Component Production Revenue)

- 4.12.2 Automotive (Automobile Production)

- 4.12.3 Building and Construction (New Construction Floor Area)

- 4.12.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.12.5 Packaging (Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Volume)

- 5.1 By End-User Industry

- 5.1.1 Automotive

- 5.1.2 Electrical and Electronics

- 5.1.3 Building and Construction

- 5.1.4 Packaging

- 5.1.5 Industrial and Machinery

- 5.1.6 Aerospace

- 5.1.7 Other End-User Industries

- 5.2 By Resin Type

- 5.2.1 Fluoropolymers

- 5.2.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.4 Polyvinylfluoride (PVF)

- 5.2.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer

- 5.2.3 Polyamide

- 5.2.3.1 Aramid

- 5.2.3.2 Polyamide (PA) 6

- 5.2.3.3 Polyamide (PA) 66

- 5.2.3.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate

- 5.2.5 Polycarbonate

- 5.2.6 Polyether Ether Ketone

- 5.2.7 Polyethylene Terephthalate

- 5.2.8 Polyimide

- 5.2.9 Polymethyl Methacrylate

- 5.2.10 Polyoxymethylene

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 Asahi Kasei

- 6.4.3 Daicel Corporation

- 6.4.4 Daikin Industries Ltd.

- 6.4.5 Idemitsu Kosan Co., Ltd.

- 6.4.6 Kaneka Corporation

- 6.4.7 Kuraray Co., Ltd.

- 6.4.8 Kureha Corporation

- 6.4.9 MCT PET Resin Co., Ltd.

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 Mitsui Chemicals, Inc.

- 6.4.12 PBI Advanced Materials Co., Ltd.

- 6.4.13 Polyplastics-Evonik Corporation

- 6.4.14 Sumitomo Chemical Co., Ltd.

- 6.4.15 Techno-UMG Co., Ltd.

- 6.4.16 Teijin Limited

- 6.4.17 TORAY INDUSTRIES INC.

- 6.4.18 UBE Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs