PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044273

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044273

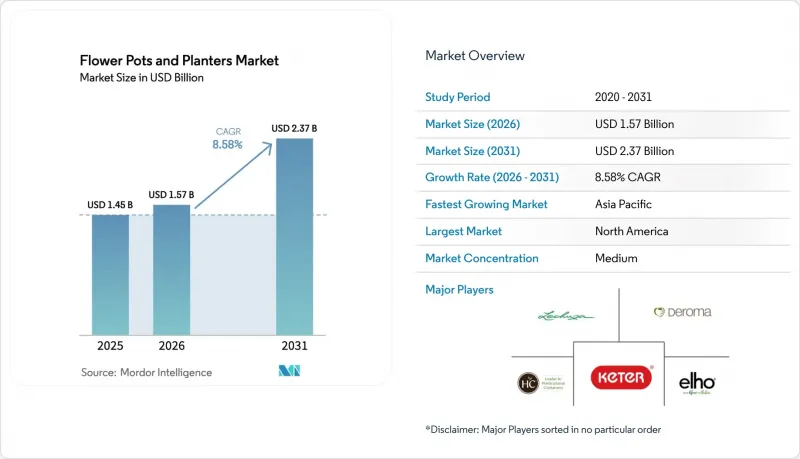

Flower Pots And Planters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The flower pots and planters market size is expected to increase from USD 1.45 billion in 2025 to USD 1.57 billion in 2026 and reach USD 2.37 billion by 2031, growing at a CAGR of 8.58% over 2026-2031.

Progress is shaped by regulation-driven shifts to recycled content, verified lifecycle impact, and resilient supply strategies that temper resin volatility. Compliance milestones in the European Union and the United States are pushing mono-material designs and higher post-consumer recycled content, which tightens integration across sourcing, molding, and take-back operations. The flower pots and planters market also benefits from public-sector greening programs and city-scale climate adaptation, which favor durable, low-carbon products with verifiable energy and emissions performance. Channel dynamics show offline as the anchor for tactile evaluation, while online grows quickly with better visualization and accessibility compliance, which elevates omnichannel inventory and content execution. Leaders in the flower pots and planters market link feedstock strategy with product design and distribution orchestration, which builds a margin and compliance advantage over portfolios reliant on virgin resin.

Global Flower Pots And Planters Market Trends and Insights

Urban Gardening and Outdoor-Living Upgrades Propel Residential Spend

Home upgrades that improve curb appeal and livability now feature planters as a visible and modular element of outdoor design. Green space is widely associated with improved household well-being and asset appeal, which makes targeted planter additions a simple way to lift visual impact without large-scale construction. Urban policies that prioritize heat mitigation and shade can include containerized trees and shrubs for faster rollout in constrained streetscapes. China's continued land greening through 2024 indicates policy momentum that supports sapling and planter demand into the next decade. This tailwind supports entry-level and premium offerings alike as households look for durable, low-maintenance options that fit compact balconies and patios. The flower pots and planters market benefits from this steady residential base while public programs add volume in high-visibility corridors.

Omnichannel Expansion Balances Tactile Discovery with Digital Conversion

Offline remains large because weight, finish, and drainage design invite in-person evaluation, but digital discovery and replenishment now move in sync with seasonal windows. The segment's 2025 base shows offline at 75.8% with online growing faster, which pushes brands to align merchandising, inventory, and creative across both touchpoints. Accessibility requirements in the European Union, effective June 2025, are raising the quality bar for e-commerce content, including alternative text and screen-reader support. That change is improving conversion for compliant retailers and encouraging better product-data standards across the value chain. Retailers that merge physical showrooms with virtual visualization and click-and-collect flow see steadier sell-through across uneven weather patterns. This evolution keeps the flower pots and planters market centered on experience quality while digital capabilities scale reach and resilience.

Seasonality and Discretionary-Spend Sensitivity Compress Margins and Working Capital

Demand spikes align with weather and planting windows, which raises stock planning complexity and return risk. Retailers see early-season surges followed by lulls, which can leave excess inventory and markdowns if replenishment outpaces actual planting. Private-label assortments price aggressively and amplify elasticities, which narrows premium bands unless brands add measurable value. Certifications and documented lifecycle performance help defend pricing where buyers face sustainability reporting. Clear and harmonized labeling standards improve signal in crowded aisles and reduce confusion that often favors the lowest price. In aggregate, these factors compress working capital cycles and challenge less diversified suppliers in the flower pots and planters market.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability Shift to Recycled Plastics and Natural Materials Redefines Feedstock Strategy

- Commercial Landscaping and Municipal Beautification Spend Growth Unlocks B2B Channels

- Resin and Kiln Energy Volatility Plus Decarbonization Capex Stress Producer Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic held a 51.05% share in 2025, while bio-composite and recycled materials are forecast to post a 9.75% CAGR through 2031, which reshapes sourcing and tooling priorities for the category. The EU Packaging and Packaging Waste Regulation, effective in August 2026, formalizes recycled content thresholds that influence both packaging and product strategies in adjacent categories. Producers that switched to 100% recycled polypropylene at scale have validated lower carbon footprints and proof of quality control, which strengthens retail positioning and compliance narratives. United States mandates and defined non-compliance penalties increase the value of centralized PCR procurement and mono-material construction that protects end-of-life recyclability. These converging rules and case studies increase confidence that content claims can be verified and defended in audits across channels. The flower pots and planters industry is therefore standardizing around traceable feedstock and clear labeling to future-proof assortments and pricing.

Ceramic and terracotta retain relevance where thermal mass, patina, and longevity are valued in public streetscapes and heritage settings. Energy intensity is the pressure point, which is why national policy reducing network charges for energy-intensive industries matters for medium-term viability. This relief aligns with private investment in electric kilns that can achieve very large emissions reductions and support compliance under tighter trading schemes. Metal planters maintain a niche in architectural projects, while certified wood options support natural-wood aesthetics with controlled sourcing. Bio-composites enter commercial assortments as UV and frost validation completes and as agricultural byproduct streams become reliable. Over the forecast horizon, verified PCR and bio-based inputs will expand their role in the flower pots and planters market as procurement policies and retailer scorecards embed them in standard buying criteria.

Traditional pots accounted for 45.7% in 2025, while self-watering and smart containers are projected to grow at a 10.55% CAGR through 2031, supported by proven water-use and labor benefits. Self-watering reservoirs, moisture indicators, and integrated sensors reduce guesswork and missed irrigation windows for residential buyers and property managers. Leading brands have expanded self-watering lines and introduced visible indicators that simplify upkeep, which builds adoption among first-time gardeners. Product quality is now tied to seal integrity, UV stability, and capillary-wick performance, documented through QA systems that meet ISO requirements in commercial tenders. The flower pots and planters market share will track how quickly automation features filter into mainstream price bands where replacement cycles are steady. As interoperability improves, smart variants will stack on top of these gains with telemetry and better battery life.

Planter boxes, troughs, and raised beds power balcony kitchens and small-plot urban growing where depth, modularity, and airflow matter. Hanging baskets maintain presence, especially where early spring promotions move the season forward in cooler climates. Municipal buyers use large-format planters for curb protection, traffic calming, and stormwater management, and these applications reward impact resistance and serviceable irrigation. Vendors that document repeatability with ISO 9001 and environmental practices with ISO 14001 have an advantage in those procurements. Brands that focus on minimal parts, mono-material designs, and refillable accessories can simplify maintenance and recycling. Over time, these features compound across the flower pots and planters Market as both home and public buyers look for visible value and simple care.

The Flower Pots and Planters Market Report is Segmented by Material (Plastic, Ceramic and Terracotta, and More), Product Type (Flower Pots, Planters, and More), Application (Residential, and Commercial and Municipal), Distribution Channel (Offline, and Online Retail), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 32.8% in 2025, and Asia-Pacific is projected to expand at a 9.92% CAGR through 2031, which sets the pace differential for regional planning. North America's share of the flower pots and planters market size stood at 32.8% in 2025, while Asia-Pacific's faster growth profile is anchored by urbanizing corridors and public greening. The United States municipal projects, including targeted curb-zone enhancements, use planters for safety, wayfinding, and stormwater objectives. State-level PCR mandates and defined penalties incentivize recycled feedstock and mono-material designs. In Canada and Mexico, short planting windows and middle-class expansion sustain demand across premium and value tiers. These patterns confirm that the flower pots and planters market will remain diverse in regional product mixes and buying cycles.

Europe's regulatory path is clear, and effective dates now fall within the planning horizon for procurement and packaging. The EU Packaging and Packaging Waste Regulation formalizes recycled content goals and pushes mono-material designs that preserve recyclability. The United Kingdom's decision to extend discounted network charges for energy-intensive sectors supports ceramic and terracotta supply economics. European heritage districts often prefer terracotta for streetscapes, which benefits from both energy relief and private investment in electrification that improves emissions outcomes. Northern and Western European countries with high garden ownership create stable household demand alongside municipal plantings. As a result, the flower pots and planters market in Europe blends steady retail flow with procurement anchored by compliance and durability.

Asia-Pacific leads the growth tables as city governments and private developers integrate greenery into built environments. Policy continuity in China on land greening extends momentum for nurseries and urban plantings, which drives container demand upstream and downstream. Singapore's urban greenery systems and new indoor farms show how automated planters and telemetry can scale where space is tight. In the Middle East, Saudi Arabia's city-scale program adds volume and sets high durability and heat-resistance requirements for products. Select African municipalities and fast-growing cities are beginning to adopt streetscape and micro-forest programs where containerized trees can be deployed quickly. Together, these programs shape the flower pots and planters market with high-visibility installs that influence consumer preferences and retail displays.

- Keter Group

- elho B.V.

- Deroma Group

- LECHUZA (Geobra Brandstatter)

- The HC Companies, Inc.

- East Jordan Plastics, Inc.

- Nursery Supplies Inc.

- Landmark Plastic Inc.

- Crescent Garden

- Bloem, LLC

- Novelty Manufacturing Co.

- Veradek Inc.

- CAPI Europe B.V.

- Euro3plast S.p.A.

- Stefanplast S.p.A.

- Yorkshire Flowerpots Ltd.

- BENITO URBAN

- Emsa GmbH

- Pacific Home & Garden

- Scheurich GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urban gardening and outdoor-living upgrades

- 4.2.2 Omnichannel expansion with strong offline discovery and rising e-commerce conversion

- 4.2.3 Sustainability shift to recycled plastics and natural materials

- 4.2.4 Commercial landscaping and municipal beautification spend growth

- 4.2.5 EPR/PPWR compliance accelerating mono-material, high-PCR planters

- 4.2.6 Smart/self-watering planters and IoT-enabled municipal maintenance

- 4.3 Market Restraints

- 4.3.1 Seasonality and discretionary-spend sensitivity; intense price competition

- 4.3.2 Resin and kiln energy volatility; decarbonization capex for ceramics

- 4.3.3 Private-label commoditization and online price pressure

- 4.3.4 Plastics recycling bottlenecks; uneven kerbside acceptance; new EPR fees

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.2 Ceramic & Terracotta

- 5.1.3 Metal

- 5.1.4 Wood

- 5.1.5 Bio-composite & Recycled

- 5.2 By Product Type

- 5.2.1 Flower Pots

- 5.2.2 Planters (Boxes, Troughs, Raised Beds)

- 5.2.3 Hanging Baskets

- 5.2.4 Self-watering / Smart Containers

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial & Municipal

- 5.4 By Distribution Channel

- 5.4.1 Offline

- 5.4.1.1 Home-Improvement & DIY Chains

- 5.4.1.2 Specialty Decor & Furniture Stores

- 5.4.1.3 Nurseries & Garden Centers

- 5.4.1.4 Supermarkets & Hypermarkets

- 5.4.2 Online Retail

- 5.4.1 Offline

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX

- 5.5.3.7 NORDICS

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South-East Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Keter Group

- 6.4.2 elho B.V.

- 6.4.3 Deroma Group

- 6.4.4 LECHUZA (Geobra Brandstatter)

- 6.4.5 The HC Companies, Inc.

- 6.4.6 East Jordan Plastics, Inc.

- 6.4.7 Nursery Supplies Inc.

- 6.4.8 Landmark Plastic Inc.

- 6.4.9 Crescent Garden

- 6.4.10 Bloem, LLC

- 6.4.11 Novelty Manufacturing Co.

- 6.4.12 Veradek Inc.

- 6.4.13 CAPI Europe B.V.

- 6.4.14 Euro3plast S.p.A.

- 6.4.15 Stefanplast S.p.A.

- 6.4.16 Yorkshire Flowerpots Ltd.

- 6.4.17 BENITO URBAN

- 6.4.18 Emsa GmbH

- 6.4.19 Pacific Home & Garden

- 6.4.20 Scheurich GmbH & Co. KG

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

- 7.2 Mono-material recycled PP planters aligned to EU PPWR 2030 PCR/recyclability thresholds

- 7.3 Smart/self-watering retrofits and IoT telemetry for municipal and commercial planters to cut OPEX and water use