PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044275

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044275

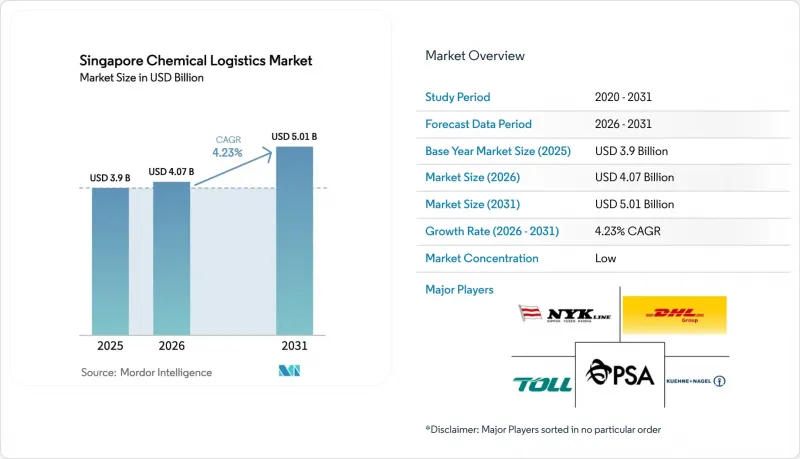

Singapore Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Singapore chemical logistics market size was valued at USD 3.9 billion in 2025 and estimated to grow from USD 4.07 billion in 2026 to reach USD 5.01 billion by 2031, at a CAGR of 4.23% during the forecast period (2026-2031).

Chemical re-export flows to Africa and South Asia generate premium margins because importers in those regions rely on Singapore for quality verification and consolidated documentation. SS 667:2020 upgrades are tightening dangerous-goods warehouse supply, favoring capital-rich operators with compliant facilities. Tuas Port's autonomous yard-truck deployments are already showing 20-30% dwell-time savings that raise asset utilization for operators with real-time data connectivity. Private-equity backed ISO-tank leasing pools domiciled in Singapore are expanding specialized equipment availability and helping integrated providers bundle transport, tank rental, and TradeNet filing into single-source offerings. Low-carbon ammonia bunkering trials, together with the TradeNet e-DG permit revamp, illustrate how government-led digitalization and decarbonization initiatives are continually raising the baseline for operational efficiency.

Singapore Chemical Logistics Market Trends and Insights

Surge in Singapore's Specialty-Chemical Re-Exports to Africa and South Asia

Enterprise Singapore recorded SGD 91.5 billion (USD 68.6 billion) of chemical exports in 2024, and specialty segments such as surfactants and catalysts posted double-digit growth toward emerging markets. Importers rely on Singapore for smaller lot repackaging, local-language SDS preparation, and authenticity assurance, allowing logistics providers to charge 2-3 times standard transshipment rates. Partnerships with African distributors add inventory management and supply-chain financing services, while South Asian pharmaceutical buyers adopt Singapore-based sourcing to diversify away from single-country dependencies. The dynamic is expected to widen the revenue share of value-added activities, reinforcing Singapore's function as a risk-buffering gateway for specialty chemicals.

Autonomous Yard-Truck Pilots at Tuas Port Accelerating Turnaround Times

PSA Singapore has deployed more than 200 autonomous electric yard trucks capable of 24/7 operation with centimeter-level precision, cutting chemical container dwell time by up to 30%. Automation removes driver fatigue limitations and reduces human exposure to hazardous cargo, enhancing both safety and productivity. Event-driven port software feeds routing updates to each vehicle, synchronizing yard moves with vessel schedules and warehouse slot availability. Integrated 3PLs that plug their transport-management systems directly into PSA's data layer gain real-time milestones, pushing on-time performance above 98%.

Rising Insurance Premiums for DG Warehousing Post-Global Incidents

After the Beirut and Tianjin explosions, underwriters raised premiums 30-50% for facilities without advanced detection and suppression, compelling operators to adopt real-time monitoring and third-party safety audits to maintain cover. Capital-rich firms comply; smaller players often exit, tightening supply and supporting higher rents for certified space.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory SS 667:2020 Certification Driving Compliant Storage Demand

- PE-Backed Growth of ISO-Tank Leasing Pools Domiciled in Singapore

- EU CBAM Compliance Burden Inflating Export Documentation Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation maintained 66.47% share of the Singapore chemical logistics market in 2025, yet other services are growing faster at 6.11% CAGR as exporters grapple with CBAM filings, dangerous-goods packaging, and customs brokerage. The Singapore chemical logistics market size for value-added services benefits from advisory fees of USD 5,000-25,000 per exporter on carbon reporting mandates. Meanwhile, autonomous yard-truck rollouts improve truck cycle times but cannot fully offset fuel-surcharge volatility. Warehousing revenue is buoyed by SS 667:2020 premiums that lift rents 40-60% above standard industrial space and enhance the overall Singapore chemical logistics market share captured by operators offering certified storage.

Demand for bundled solutions lets integrated 3PLs pair ISO-tank leasing with TradeNet automation, creating stickier contracts and pricing power. Niche consultants thrive on dangerous-goods documentation and packaging for small-lot re-exports to Africa. Those without digital permit integration risk disintermediation as shippers embrace providers capable of same-day clearance.

Oil and Gas controls 27.08% Singapore chemical logistics market share owing to Jurong Island's refinery complex, yet pharmaceutical logistics expands at 5.28% CAGR on biologics flows to power-unstable ASEAN neighbors. GDP-compliant facilities with backup power and validated cold rooms command 2-3-times standard handling rates, boosting the Singapore chemical logistics market size attributable to healthcare shipments. Cosmetics and specialty electronic chemicals also gain from Singapore's role as a regional consolidation hub for semiconductor fabs and beauty brands.

Stringent Health Sciences Authority oversight ensures only licensed GDP providers compete, limiting supply and supporting margins. Conversely, energy-transition measures compress crude trading volumes, forcing Oil & Gas logistics to pursue ISO-tank optimization and automation to preserve profitability.

The Singapore Chemical Logistics Market Report is Segmented by Service (Transportation, Warehousing/Distribution/Inventory Management, Other Services), End-User Industry (Pharmaceutical, Cosmetic, Oil and Gas, Specialty Chemicals, and More), Hazard Class (Hazardous Chemicals, Non-Hazardous Chemicals), Temperature Control (Temperature-Controlled, Non-Temperature-Controlled). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ALPS Global Logistics

- Bertschi Singapore Pte Ltd.

- DHL Group

- Kuehne+Nagel

- PSA Chemical Logistics (PSA Corp)

- NYK Line

- CMA CGM Group (Including CEVA Logistics)

- "K" Line

- Mitsubishi Chemical Logistics

- Noatum Holdings

- CWT Pte Ltd.

- YCH Group

- DSV A/S

- Rohlig Logistics

- Poh Tiong Choon Logistics Ltd.

- Yang Kee Logistics Pte Ltd.

- Suttons International

- Den Hartogh Logistics

- TranceGlobal Logistics Pte Ltd.

- Toll Group

- ACW Logistics Pte Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in SG's Specialty-Chemical Re-Exports to Africa and South Asia

- 4.2.2 Autonomous Yard-Truck Pilots at Tuas Port Accelerating Turnaround Times

- 4.2.3 Mandatory SS 667:2020 Certification Driving Compliant Storage Demand

- 4.2.4 PE-Backed Growth of ISO-Tank Leasing Pools Domiciled in Singapore

- 4.2.5 Low-Carbon Ammonia Bunkering Trials Creating New Logistics Flows

- 4.2.6 Tradenet E-DG Permit Revamp Reducing Customs Clearance Times

- 4.3 Market Restraints

- 4.3.1 Rising Insurance Premiums for DG Warehousing Post-Global Incidents

- 4.3.2 EU CBAM Compliance Burden Inflating Export Documentation Cycles

- 4.3.3 Limited Domestic Rail Connectivity Hindering Multimodal Cost Savings

- 4.3.4 Volatile Bunker Fuel Surcharges Eroding 3PL Margin Stability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea

- 5.1.2 Warehousing, Distribution and Inventory Management

- 5.1.3 Other Services

- 5.1.1 Transportation

- 5.2 By End-User Industry

- 5.2.1 Pharmaceutical

- 5.2.2 Cosmetic

- 5.2.3 Oil and Gas

- 5.2.4 Specialty Chemicals

- 5.2.5 Other End-Users

- 5.3 By Hazard Class

- 5.3.1 Hazardous Chemicals

- 5.3.2 Non-hazardous Chemicals

- 5.4 By Temperature Control

- 5.4.1 Temperature-Controlled (Refrigerated/Heated)

- 5.4.2 Non-Temperature-Controlled

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 ALPS Global Logistics

- 6.4.2 Bertschi Singapore Pte Ltd.

- 6.4.3 DHL Group

- 6.4.4 Kuehne+Nagel

- 6.4.5 PSA Chemical Logistics (PSA Corp)

- 6.4.6 NYK Line

- 6.4.7 CMA CGM Group (Including CEVA Logistics)

- 6.4.8 "K" Line

- 6.4.9 Mitsubishi Chemical Logistics

- 6.4.10 Noatum Holdings

- 6.4.11 CWT Pte Ltd.

- 6.4.12 YCH Group

- 6.4.13 DSV A/S

- 6.4.14 Rohlig Logistics

- 6.4.15 Poh Tiong Choon Logistics Ltd.

- 6.4.16 Yang Kee Logistics Pte Ltd.

- 6.4.17 Suttons International

- 6.4.18 Den Hartogh Logistics

- 6.4.19 TranceGlobal Logistics Pte Ltd.

- 6.4.20 Toll Group

- 6.4.21 ACW Logistics Pte Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment