PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072905

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072905

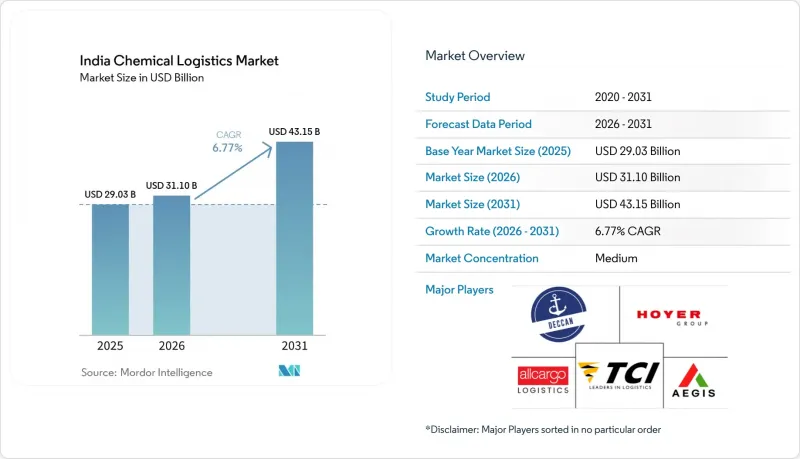

India Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india chemical logistics market size is expected to increase from USD 29.03 billion in 2025 to USD 31.10 billion in 2026 and reach USD 43.15 billion by 2031, growing at a CAGR of 6.77% over 2026-2031.

This report is Segmented by Logistics (Transportation, Warehousing & Distribution, Value-Added Services), by Hazard Class (Hazardous, Non-Hazardous), by Temperature Control (Temperature-Controlled, Non-Temperature-Controlled), by End User (Pharmaceutical, Cosmetic, Oil & Gas, Specialty Chemicals, Others), and by Region (North, Central, West, East, South). The Forecasts are Provided in Terms of Value (USD).

India Chemical Logistics Market Trends and Insights

Tightening Bulk-Cargo Safety Norms Drive Compliance-Led Logistics Upgrades

Mandatory certification and stricter inspection discipline are pushing the India chemical logistics market toward greater equipment integrity and stronger process control. Bulk cargo operators are upgrading pressure-tested assets, monitoring systems, and documentation procedures to continue serving regulated lanes without disruption. This raises fixed costs for all participants, but larger fleets can spread that burden across higher shipment volumes and longer customer contracts. Smaller carriers, therefore, face weaker economics in hazardous lanes, especially where buyers now expect audited compliance and more formal safety safeguards. Over the forecast period, this compliance-led reset should leave organized operators with a stronger negotiating position in the India chemical logistics market.

PM Gati-Shakti Multimodal Corridors Redefine Chemical Freight Economics

PM Gati-Shakti is changing freight economics in the India chemical logistics market by improving links between plants, rail corridors, terminals, and ports. The practical effect is not only better line-haul speed, but also stronger schedule reliability for bulk and containerized chemical cargo. As more traffic moves through dedicated freight and cargo-terminal infrastructure, chemical shippers can work with leaner buffers and tighter dispatch planning. This is gradually shifting supply chains away from fragmented road-only loops and toward integrated rail and port combinations. Logistics providers that pair corridor access with chemical warehousing and compliance support are likely to capture a larger share of the India chemical logistics market over time.

Under-Investment in DG Cargo Rail Sidings Limits Rail Modal Shift

Under-investment in DG cargo rail sidings is slowing the modal shift that many shippers want in the India chemical logistics market. The gap is more visible in eastern and central corridors, where chemical plants still rely heavily on road tankers because dedicated rail-linked infrastructure is limited. Hazardous-commodity sidings also demand more capital, more approvals, and longer execution timelines than ordinary cargo facilities. That keeps road as the default choice for a large part of bulk DG traffic, even where rail could lower cost and improve safety. Until rail-linked hazardous cargo infrastructure improves, the India chemical logistics market will continue to carry avoidable trucking exposure in several inland corridors.

Other drivers and restraints analyzed in the detailed report include:

- Specialty-Chemical Export Surge Creates Dedicated Logistics Sub-Segments

- Cold-Chain Demand for Pharma APIs Redefines Temperature-Sensitive Chemical Logistics

- Driver-Skill Shortage Constrains Hazmat Tank-Truck Capacity Nationally

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 62.93% of the India chemical logistics market share in 2025, making it the report's core volume engine. Road continues to dominate because many chemical plants still sit away from railheads and ports, and buyers need flexible last-mile delivery across industrial belts. This also suits the large base of smaller shippers that move limited batches and cannot always fill dedicated rail or coastal lots. Rail is still gaining relevance in transportation, as carriers widen their liquid-cargo offerings and use containerized solutions to serve longer corridors.

Value-added services are projected to expand at a 9.60% CAGR through 2031, making it the fastest-growing function in the India chemical logistics industry. Chemical shippers increasingly want one provider to manage tracking, temperature logging, customs support, hazmat paperwork, and exception handling. Warehousing, distribution, and inventory management, therefore, remain important because customers are asking for safer storage and tighter stock control near major manufacturing belts. The result is a shift from pure freight execution toward bundled service models where compliance and visibility carry as much value as movement.

Hazardous chemicals accounted for 64.12% of the India chemical logistics market share in 2025 and are also the fastest-growing segment, with a CAGR of 8.77% through 2031, reflecting the significant role of petrochemicals, agrochemicals, and industrial solvents in the India chemical logistics market. The segment is large not only because of volume, but also because each shipment carries a heavier service burden. DG-rated tankers, UN-rated packaging, documented safety procedures, and endorsed drivers all lift the revenue value of hazardous cargo.

Hazardous chemicals remain the most defensible part of the India chemical logistics industry because compliance complexity raises the cost of entry. Operators need PESO-grade terminals, retrofitted fleets, digital records, and trained staff before they can compete credibly in this lane. That creates durable moats for organized companies and limits how quickly new carriers can scale in the regulated cargo market. It also means margin pressure tends to fall harder on smaller operators that lack the systems needed to manage safety and documentation at scale.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Hazard Class

- Hazardous Chemicals

- Non-hazardous Chemicals

- By Temperature Control

- Temperature-Controlled (Refrigerated/Heated)

- Non-Temperature-Controlled

- By End Use Industry

- Pharmaceutical

- Cosmetic

- Oil and Gas

- Specialty Chemicals

- Other End-Users

- By Region

- North

- Central

- West

- East

- South

List of Companies Covered in this Report:

- Aegis Logistics Limited

- Allcargo Logistics Ltd.

- Transport Corporation of India (TCI)

- Deccan Transcon Leasing Pvt. Ltd.

- HOYER Global Transport India

- Bertschi India Pvt. Ltd.

- Stolt Tank Containers India

- Balmer Lawrie & Co. Ltd.

- Kuehne+Nagel India

- DHL Supply Chain India

- Adani Logistics Ltd.

- Maersk India Pvt. Ltd.

- DSV India

- Gateway Distriparks Ltd.

- APL Logistics India

- NewPort Tank Containers India Pvt. Ltd.

- SAR Logistics

- CKB Global Logistics Pvt. Ltd.

- Crystal Group India

- Navkar Corporation Ltd.

- Shreeji Translogistics Ltd.

- RM Logistics Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Logistics in Chemical

- 4.2 Chemical Industry Spending Trends

- 4.3 Market Drivers

- 4.3.1 Tightening Bulk Cargo Safety Norms (BIS 14687-2024, Draft)

- 4.3.2 Growing Multi-Modal Chemical Corridors Under PM Gati-Shakti

- 4.3.3 Surge in Specialty-Chemical Exports (More Than 10 % YoY FY 25)

- 4.3.4 Cold-Chain Demand for High-Value Pharma APIs

- 4.3.5 Blockchain-Enabled Wagon Tracing Pilots by CONCOR

- 4.3.6 Standardization Of Flexitank & ISO-Tank Handling at Indian Ports

- 4.4 Market Restraints

- 4.4.1 Under-Investment in DG Cargo Rail Sidings

- 4.4.2 Driver-Skill Shortage for Haz-Mat Tank-Trucks

- 4.4.3 Limited Refrigerated Warehouse Capacity Outside Tier-1 Cities

- 4.4.4 High Insurance Premiums after Vizag LG Polymer Incident

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Chemical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing, Distribution and Inventory Management

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Hazard Class

- 5.2.1 Hazardous Chemicals

- 5.2.2 Non-hazardous Chemicals

- 5.3 By Temperature Control

- 5.3.1 Temperature-Controlled (Refrigerated/Heated)

- 5.3.2 Non-Temperature-Controlled

- 5.4 By End Use Industry

- 5.4.1 Pharmaceutical

- 5.4.2 Cosmetic

- 5.4.3 Oil and Gas

- 5.4.4 Specialty Chemicals

- 5.4.5 Other End-Users

- 5.5 By Region

- 5.5.1 North

- 5.5.2 Central

- 5.5.3 West

- 5.5.4 East

- 5.5.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Aegis Logistics Limited

- 6.4.2 Allcargo Logistics Ltd.

- 6.4.3 Transport Corporation of India (TCI)

- 6.4.4 Deccan Transcon Leasing Pvt. Ltd.

- 6.4.5 HOYER Global Transport India

- 6.4.6 Bertschi India Pvt. Ltd.

- 6.4.7 Stolt Tank Containers India

- 6.4.8 Balmer Lawrie & Co. Ltd.

- 6.4.9 Kuehne+Nagel India

- 6.4.10 DHL Supply Chain India

- 6.4.11 Adani Logistics Ltd.

- 6.4.12 Maersk India Pvt. Ltd.

- 6.4.13 DSV India

- 6.4.14 Gateway Distriparks Ltd.

- 6.4.15 APL Logistics India

- 6.4.16 NewPort Tank Containers India Pvt. Ltd.

- 6.4.17 SAR Logistics

- 6.4.18 CKB Global Logistics Pvt. Ltd.

- 6.4.19 Crystal Group India

- 6.4.20 Navkar Corporation Ltd.

- 6.4.21 Shreeji Translogistics Ltd.

- 6.4.22 RM Logistics Pvt. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment