PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044281

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044281

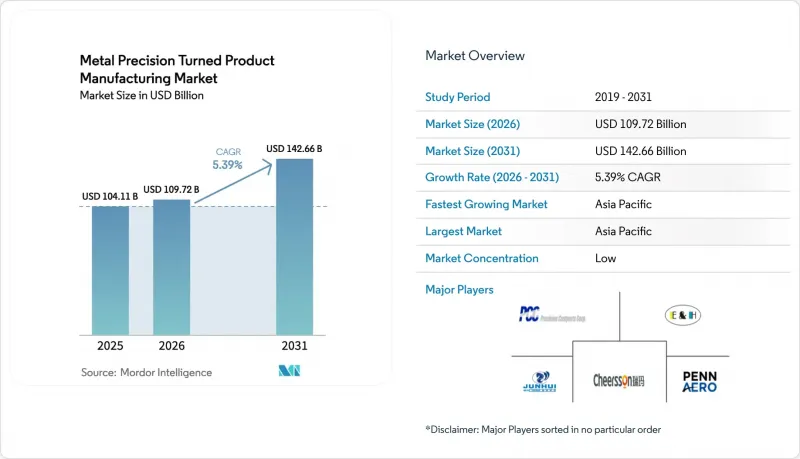

Metal Precision Turned Product Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The metal precision turned product manufacturing market size is projected to grow from USD 104.11 billion in 2025 to USD 109.72 billion in 2026 and is forecast to reach USD 142.66 billion by 2031, registering a CAGR of 5.39% between 2026 and 2031.

Rising vehicle electrification, recovering commercial-aircraft build rates, and the miniaturization of orthopedic and dental implants are together tightening tolerance bands and shortening cycle-time expectations across the metal-precision-turned product manufacturing market. As battery-electric platforms replace traditional ferrous power-train components, the demand for lightweight aluminum and copper alloys is increasing. Concurrently, aerospace giants are reviving previously dormant production lines, now favoring nickel- and titanium-based alloys. Hospitals are expanding orders for small implant screws, pushing suppliers to transition from standard chucking lathes to precision Swiss-type machines capable of holding extremely tight tolerances. In the metal precision turned product manufacturing arena, automation and in-process metrology have become the benchmarks of competitiveness, narrowing the performance divide between Tier-1 precision shops and their smaller regional counterparts.

Global Metal Precision Turned Product Manufacturing Market Trends and Insights

EV Power-Train Lightweight Precision Demand

As automakers in the European Union aimed to meet stricter CO2 emission thresholds, the aluminum content in light vehicles increased significantly . In the same period, China experienced a substantial rise in the production of battery-electric and plug-in hybrid vehicles, driving higher demand for aluminum heat-sink pins and copper busbars. Tesla's giga-casting approach reduced the number of parts but concentrated precision machining on fewer, larger aluminum nodes, requiring post-cast boring with high precision. Accelerated tool wear on non-ferrous alloys is prompting Tier-2 shops to adopt ceramic inserts and through-spindle coolant, which significantly extends tool life. These trends are collectively boosting demand for high-speed CNC cells in the metal-precision-turned product manufacturing sector.

Industry 4.0-Enabled Multi-Axis CNC Adoption

Yamazaki Mazak revealed that a significant portion of its shipments featured automation-ready robot interfaces. These interfaces facilitate overnight "lights-out" operations, effectively doubling the spindle hours. Meanwhile, a German power-train supplier successfully reduced its unplanned downtime by integrating digital twins with predictive bearing analytics. Multi-axis turning centers, now capable of simultaneous multi-axis operation, can finish turbine-blade roots or orthopedic hip stems in a single setup, thereby eliminating cumulative tolerance stack-up. Japan's machine-tool output in NC lathes achieved a notable penetration rate, indicating a near-total shift to programmable platforms. Furthermore, adaptive CAM software, which adjusts feeds and speeds in real-time, is achieving a significant reduction in cycle times for Inconel 718 and Ti-6Al-4V programs.

Volatile Steel and Brass Pricing

Aluminum prices increased over the period and are expected to remain steady in the near future, constrained by limited supply flexibility amid high energy costs in the EU and production restrictions in China. Copper prices have risen sharply and are expected to continue rising, driven by increasing demand for electric vehicle cables. The United States imposed substantial tariffs on certain copper imports, prompting Midwest shops to source from Canada at a premium. In the metal-precision turned product manufacturing market, brass-focused job shops without pass-through clauses are facing challenges as rising copper and zinc prices strain working capital and reduce profit margins.

Other drivers and restraints analyzed in the detailed report include:

- Aerospace Build-Rate and MRO Surge

- Micro-Implant Swiss-Turning Boom

- Skilled CNC Machinist Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shafts accounted for 37.11% of the metal-precision turned product manufacturing market share in 2025. High-rpm electric-motor designs spinning 15,000-20,000 rpm now demand ultra-fine surface finishes to avert bearing failures, pushing shops toward diamond-impregnated honing stones and in-machine balancing. Couplings, although smaller in absolute volume, are forecast to expand their revenue base at a 7.81% CAGR as warehouse automation and collaborative robots require zero-backlash torque transmission. Suppliers command price premiums by using sensor-embedded couplings that report vibrational signatures.

While commoditized nuts, bolts, and bushings are sensitive to price fluctuations, aerospace fasteners made from A286 stainless steel or Inconel maintain their margins, thanks to their NADCAP pedigree. Multi-spindle screw machines dominate high-volume contracts for automotive nuts. Meanwhile, flexible CNC platforms are replacing cam-driven legacy assets for medium-volume runs. In the realm of metal precision turned product manufacturing, as EV powertrains reduce part counts, shafts and couplings remain strategically important because they transmit torque between electric motors and final-drive reducers.

Steel accounted for 43.22% of the metal-precision turned product manufacturing market share in 2025, yet aluminum's 6.78% CAGR is the fastest path to volume accretion. The aluminum content of battery-electric cars has increased significantly over time. Stainless steel grades, such as 304 and 316L, dominate niches like implants, food processing, and marine applications due to their corrosion resistance, which enables them to command premium pricing. Brass continues to hold its position in low-voltage connectors due to its excellent machinability and electrical conductivity, despite fluctuations in commodity prices. Exotic alloys, including titanium, Inconel, and PEEK, account for a small share of total tonnage but represent a substantial share of market value. This emphasizes the high revenue per unit weight driven by the aerospace and medical sectors within the metal precision turned product manufacturing market.

Machining economics vary significantly. For example, Ti-6Al-4V is machined at a much slower speed compared to aluminum and requires flood coolant to prevent work hardening, which increases production costs. Similarly, PEEK polymer screws have a rotational speed limit to avoid melting, which extends production times. However, these screws command significantly higher prices than their stainless steel counterparts.

The Metal Precision Turned Product Manufacturing Market Report is Segmented by Product Type (Shafts, Spindles, Bushings, Fasteners, and More), Material (Steel, Stainless Steel, and More), Process (CNC Turning, and More), Application (Automotive, Aerospace and Defense, Industrial Machinery, and More), Sales Channel (OEMs and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 46.34% of the metal-precision turned product manufacturing market share in 2025 and is projected to grow at a 7.89% CAGR through 2031, as China remains a leading producer of vehicles, while India continues to experience significant annual growth in precision-machining capacity . In Chennai, Tsugami's complex highlights Japan's approach of co-locating foundry and finish-machining operations to meet India's domestic demand. South Korea's supply to Samsung and Hyundai ensures steady local demand for high-volume connectors and fasteners. Meanwhile, Vietnam's substantial FDI inflow is channeling brass and stainless steel turnings to global electronics brands. Thailand and Indonesia are emerging as auxiliary "China+1" nodes to address excess demand driven by rising labor costs in China.

North America and Europe, while growing steadily, maintain dominance, holding the majority of NADCAP and ISO certifications, particularly in the aerospace and medical sectors. Mexico's significant FDI investments are strengthening Bajio parks, ensuring timely shipments to U.S. assembly plants in line with USMCA regulations. Germany's machine tool exports include a notable share of precision turning centers for aerospace and automation applications. The U.K.'s Viking Precision has optimized a new production cell for the continuous manufacturing of titanium MRO parts.

Although South America, the Middle East, and Africa are smaller players, they are gaining momentum, particularly in mining and energy. Brazil's Sao Paulo cluster supports local OEMs. In the Middle East, both the UAE and Saudi Arabia are developing aerospace MRO hubs, though they currently rely on European imports. South Africa's mining sector, requiring large-diameter steel shafts, is sourcing them locally, significantly reducing lead times compared to imports. Turkey is leveraging its customs-union access to the EU, focusing on automotive and appliance parts, and benefiting from the established subcontractor networks in Istanbul and Bursa. This division-volume concentrated in Asia-Pacific and value in the West-appears set to continue in the metal-precision-turned-product manufacturing market.

- Precision Castparts Corp.

- E&H Precision (Thailand) Co., Ltd.

- NINGBO JH Metal Technology Co.,Ltd.

- Pioneer Service Inc.

- U.S. Swiss, Inc.

- PennAero

- A&B Torneria Automatica Srl

- Forster Tool and Mfg.

- Sheldon Precision

- Davturn Ltd

- Orange1 Precision

- Star Micronics

- Citizen Machinery

- Tsugami Corp.

- DMG Mori

- Yamazaki Mazak

- Okuma Corp.

- Haas Automation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV Power-Train Lightweight Precision Demand

- 4.2.2 Industry 4.0-Enabled Multi-Axis CNC Adoption

- 4.2.3 Aerospace Build-Rate and MRO Surge

- 4.2.4 Micro-Implant Swiss-Turning Boom

- 4.2.5 OEM Regional Supplier-Park Localisation

- 4.2.6 On-Machine Real-Time Metrology and Adaptive Control Adoption

- 4.3 Market Restraints

- 4.3.1 Volatile Steel and Brass Pricing

- 4.3.2 Skilled CNC Machinist Shortage

- 4.3.3 Qualification Costs For Exotic Alloys

- 4.3.4 Rising Electricity Prices For High-Speed Machining Operations

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Product Type

- 5.1.1 Shafts

- 5.1.2 Spindles

- 5.1.3 Bushings

- 5.1.4 Fasteners

- 5.1.5 Couplings

- 5.1.6 Nuts and Bolts

- 5.1.7 Others (Pins, Connectors)

- 5.2 By Material

- 5.2.1 Steel

- 5.2.2 Stainless Steel

- 5.2.3 Brass

- 5.2.4 Aluminum

- 5.2.5 Copper

- 5.2.6 Others (Alloys, Specialty Metals)

- 5.3 By Process

- 5.3.1 CNC Turning

- 5.3.2 Automatic Turning

- 5.3.3 Swiss-Type Turning

- 5.3.4 Multi-Spindle Turning

- 5.4 By Application

- 5.4.1 Automotive

- 5.4.2 Aerospace and Defense

- 5.4.3 Industrial Machinery

- 5.4.4 Electrical and Electronics

- 5.4.5 Medical Devices

- 5.4.6 Construction Equipment

- 5.4.7 Others

- 5.5 By Sales Channel

- 5.5.1 Original Equipment Manufacturer (OEM)

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Precision Castparts Corp.

- 6.4.2 E&H Precision (Thailand) Co., Ltd.

- 6.4.3 NINGBO JH Metal Technology Co.,Ltd.

- 6.4.4 Pioneer Service Inc.

- 6.4.5 U.S. Swiss, Inc.

- 6.4.6 PennAero

- 6.4.7 A&B Torneria Automatica Srl

- 6.4.8 Forster Tool and Mfg.

- 6.4.9 Sheldon Precision

- 6.4.10 Davturn Ltd

- 6.4.11 Orange1 Precision

- 6.4.12 Star Micronics

- 6.4.13 Citizen Machinery

- 6.4.14 Tsugami Corp.

- 6.4.15 DMG Mori

- 6.4.16 Yamazaki Mazak

- 6.4.17 Okuma Corp.

- 6.4.18 Haas Automation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment