PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061566

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061566

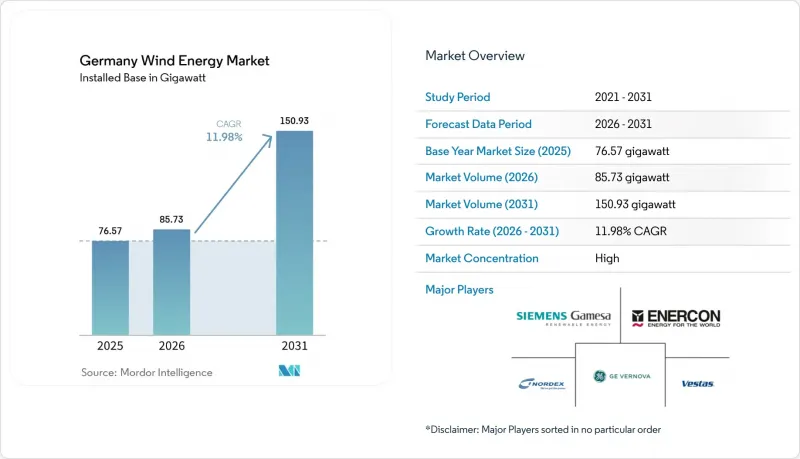

Germany Wind Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany wind energy market size is expected to grow from 76.57 gigawatt in 2025 to 85.73 gigawatt in 2026 and is forecast to reach 150.93 gigawatt by 2031 at 11.98% CAGR over 2026-2031.

This report is Segmented by Location (Onshore and Offshore), Turbine Capacity (Less Than 3 MW, 3 To 6 MW, and Above 6 MW), and Application (Utility-Scale, Commercial and Industrial, and Community Projects). The Market Size and Forecasts are Provided in Terms of Installed Capacity (GW).

Germany Wind Energy Market Trends and Insights

Federal 115 GW Onshore & 30 GW Offshore Targets Drive Market Acceleration

Binding 2030 capacity goals translate into annual additions of 7.7 GW onshore and 4 GW offshore, a step-change from 2024's 2.5 GW net onshore increase. Developers with shovel-ready projects and secured interconnection spots gain a first-mover advantage. Offshore ambitions triple present capacity, forcing unprecedented coordination between grid operators and project sponsors. TenneT's North Sea links already move 8.03 GW, yet expansion to 70 GW by 2045 requires 35 HVDC corridors that are now entering the tender phase.

Streamlined Permitting & Wind-an-Land Act Reduce Development Friction

Permitting reforms lifted 2024 approvals 85% year-on-year to 14 GW, cutting bureaucratic hurdles for small and mid-sized developers. Federal states must zone 2% of land for wind by 2027-2032, guaranteeing spatial certainty. North Rhine-Westphalia licensed 1.5 GW in Q1-2025 alone, illustrating rapid uptake. Yet average construction lead time still exceeds two years, meaning the bulk of new capacity flows into the 2026-2028 window.

Grid Bottlenecks & Curtailment Risk Constrain Output Optimization

Nineteen TWh of wind power were curtailed in 2023, equal to 13% of total generation, due to limited north-to-south transmission. Federal approval of five major AC corridors will ease congestion, but completion dates after 2027 leave near-term earnings exposed. Offshore generation compounds the issue as North Sea output surges ahead of onshore grid reinforcements.

Other drivers and restraints analyzed in the detailed report include:

- Corporate PPAs & Green Hydrogen Create New Revenue Streams

- Repowering of >15-Year Turbines Amplifies Capacity Additions

- Dependency on Asian Supply Chains Creates Strategic Vulnerabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Onshore assets supplied 87.02% of the German wind energy market size in 2025, yet offshore projects grow at a 20.7% CAGR through 2031. Schleswig-Holstein, Lower Saxony, and Mecklenburg-Vorpommern host two-thirds of installed capacity, benefiting from 7-8 m/s winds at 100 m hub height and early zoning. Fixed-bottom foundations in 30-50 m depths cost EUR 1.5-2 million per turbine, well below floating alternatives, giving the German wind energy market strong cost signals to push near-shore sites first.

Offshore capacity rises from 10.03 GW in 2025 to 33.58 GW in 2031 as the German Bight and Pomeranian Bay absorb 7 GW of 2024 auction awards. Capacity factors above 50% and zero-subsidy economics improve project finance leverage ratios. Onshore growth hinges on repowering in Lower Saxony and Brandenburg, where three 2 MW turbines give way to one 6 MW unit, freeing rotor-swept area while recycling foundations. This dual-track expansion keeps the German wind energy industry resilient to site scarcity.

List of Companies Covered in this Report:

- Siemens Gamesa Renewable Energy SA

- Vestas Wind Systems A/S

- Enercon GmbH

- Nordex SE

- GE Vernova (GE Renewable Energy)

- RWE AG

- Orsted A/S

- ENBW AG

- PNE AG

- BayWa r.e. AG

- WPD AG

- ABO Energy GmbH & Co. KGaA

- Deutsche Windtechnik AG

- Siemens Energy AG (Grid solutions)

- TenneT TSO GmbH

- 50Hertz Transmission GmbH

- Orsted Germany GmbH

- Statkraft Markets GmbH

- TotalEnergies Renewables Deutschland

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal 115 GW on-shore & 30 GW off-shore targets (2030)

- 4.2.2 Stream-lined permitting & "Wind-an-Land" Act

- 4.2.3 Corporate PPAs + green-hydrogen demand pull

- 4.2.4 Repowering of >15-yr turbines boosts MW additions

- 4.2.5 HVDC offshore grid & North Sea inter-connectors

- 4.2.6 Citizen-energy revenue-sharing schemes

- 4.3 Market Restraints

- 4.3.1 Grid bottlenecks & curtailment risk

- 4.3.2 Dependency on Asian turbine supply-chains

- 4.3.3 Local opposition & litigation delays

- 4.3.4 Skilled-labour shortage for offshore O&M

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Location

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 By Turbine Capacity

- 5.2.1 Up to 3 MW

- 5.2.2 3 to 6 MW

- 5.2.3 Above 6 MW

- 5.3 By Application

- 5.3.1 Utility-scale

- 5.3.2 Commercial and Industrial

- 5.3.3 Community Projects

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Nacelle/Turbine

- 5.4.2 Blade

- 5.4.3 Tower

- 5.4.4 Generator and Gearbox

- 5.4.5 Balance-of-System

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Siemens Gamesa Renewable Energy SA

- 6.4.2 Vestas Wind Systems A/S

- 6.4.3 Enercon GmbH

- 6.4.4 Nordex SE

- 6.4.5 GE Vernova (GE Renewable Energy)

- 6.4.6 RWE AG

- 6.4.7 Orsted A/S

- 6.4.8 ENBW AG

- 6.4.9 PNE AG

- 6.4.10 BayWa r.e. AG

- 6.4.11 WPD AG

- 6.4.12 ABO Energy GmbH & Co. KGaA

- 6.4.13 Deutsche Windtechnik AG

- 6.4.14 Siemens Energy AG (Grid solutions)

- 6.4.15 TenneT TSO GmbH

- 6.4.16 50Hertz Transmission GmbH

- 6.4.17 Orsted Germany GmbH

- 6.4.18 Statkraft Markets GmbH

- 6.4.19 TotalEnergies Renewables Deutschland

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment