PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061570

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061570

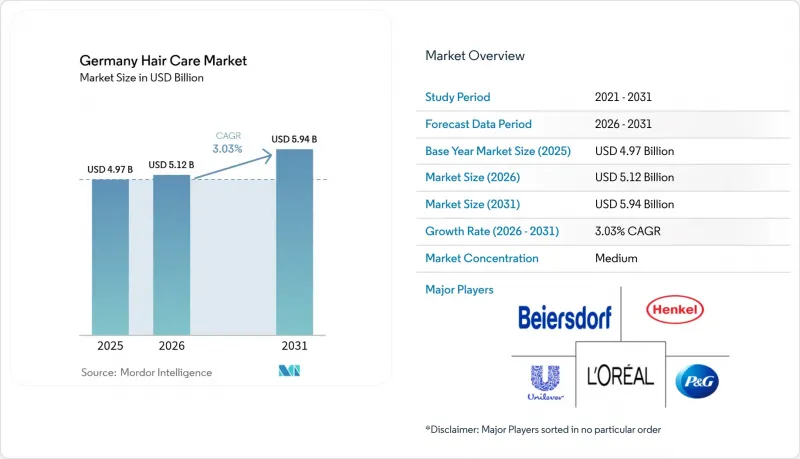

Germany Hair Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany hair care market size was valued at USD 4.40 billion in 2025 and estimated to grow from USD 4.61 billion in 2026 to reach USD 5.76 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031).

This report is Segmented by Product Type (Shampoo, Conditioner, Hair Colorants, and More), Category (Synthetic/Conventional, Natural/Organic), Price Tier (Mass, Premium), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, Online Retail Stores, Other Distribution Channels), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Germany Hair Care Market Trends and Insights

Ageing population spurring scalp-health products

Germany's ageing population is driving significant growth in the demand for scalp-health products, particularly those addressing hair loss, thinning, and scalp sensitivity. The country's demographic shift is creating a steady need for hair care solutions tailored to age-related issues. Individuals aged 55 and above are leading the consumption of health-focused personal care products. According to Statistisches Bundesamt, Germany's population aged 65 and older reached 19.01 million in 2024. This group not only maintains long-standing product preferences but also actively seeks solutions for thinning hair, sensitive scalps, and hair color coverage. With their strong purchasing power and preference for at-home care, this demographic is pushing the market towards innovations in gentle formulations and dermatologist-approved products. Companies are responding by launching specialized product lines featuring keratin repair technologies and active ingredients for scalp health. This trend is further supported by Germany's salon industry, which is adapting to meet the needs of older clients by focusing on hair preservation treatments rather than dramatic styling changes. Additionally, compliance with EU Cosmetics Regulation ensures high safety standards, benefiting older consumers who prioritize gentle yet effective formulations.

Greater demand for premium and customized hair care

German consumers, despite their price sensitivity, are increasingly drawn to premium positioning. Brands are effectively validating their higher price points through personalization and efficacy claims. The customization trend leverages digital diagnostics and AI-driven recommendations, with leading players investing in data collection platforms to deliver personalized formulations. German consumers are willing to pay premiums for products tailored to specific hair types and concerns, particularly when supported by scientific validation and visible results. According to the Statistisches Bundesamt, private household spending on personal care in Germany amounted to EUR 63.78 billion in 2024. This shift is disrupting traditional mass-market strategies, pushing brands to adopt more advanced segmentation approaches and strengthen their direct-to-consumer capabilities. Professional salon channels are capitalizing on this trend by offering exclusive product lines and in-salon diagnostic services that justify premium pricing. This move toward customization aligns with broader European beauty trends that focus on individual needs rather than one-size-fits-all solutions.

Saturated market and high brand rivalry

Established players face mounting competitive pressure as they defend their market share against private label growth and the entry of emerging natural brands. In Germany, the retail landscape is dominated by major chains such as Edeka, Rewe, and Schwarz Group, leading to limited shelf space and forcing brands to compete fiercely for distribution. The proliferation of brands across different price tiers creates consumer confusion and weakens marketing effectiveness, prompting higher advertising expenditures to sustain visibility. This heightened competition reduces pricing flexibility and squeezes margins, particularly for mid-tier brands caught between premium and value segments. The market becomes even more crowded with the growth of private labels, niche products, and substitutes like home-based DIY regimens. These trends raise consumer expectations and make it increasingly difficult for any single player to secure lasting loyalty or market dominance. Smaller brands struggle to manage regulatory compliance costs, especially when competing with larger players capable of absorbing higher expenses for product testing, reformulation, and multi-channel distribution. This dynamic raises barriers to entry and hinders innovation from new market entrants.

Other drivers and restraints analyzed in the detailed report include:

- Rising demand for natural/organic formulations

- Influence of social media and celebrity endorsements

- Price sensitivity amid private-label rise

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shampoo holds a leading 38.55% market share in 2025, highlighting its critical role in daily hair care and frequent consumer repurchases. The shampoo segment, which includes anti-dandruff, moisturizing, color protection, volumizing, medicated, and natural/organic variants, meets diverse consumer preferences and hair types, sustaining its demand. Hair styling products represent the fastest-growing segment, with a projected 4.45% CAGR through 2031, driven by social media influence and the availability of professional-grade formulations in the consumer market. Conditioners are benefiting from increased awareness of hair health and damage prevention, while hair colorants face challenges from salon competition and fluctuating DIY trends. The rapid growth of the styling segment reflects the increasing sophistication of German consumers, who are more inclined to experiment with professional-quality products at home.

Brands like Henkel's Gliss differentiate themselves in competitive segments by leveraging innovations such as "Liquid Hair-Repair Technology," showcasing the impact of liquid keratin technologies and bond-building formulations. Other product categories, including treatments and masks, are gaining incremental market share through premiumization and targeted solutions for specific hair concerns. This shift aligns with a broader beauty industry trend that prioritizes multi-step routines and specialized products tailored to individual needs over generic hair care solutions.

Synthetic and conventional formulations dominate the market with a 71.78% share in 2025, owing to their proven efficacy and cost-effectiveness, which resonate with budget-conscious consumers. Manufacturers leverage synthetic ingredients to craft products that are stable, long-lasting, and consistent in texture, scent, and performance. Meanwhile, natural and organic alternatives are on a growth trajectory, expanding at a 4.96% CAGR through 2031, underscoring the sustainability and clean beauty values of German consumers. The natural segment gains an edge from certification frameworks like NATRUE and COSMOS, which enhance credibility and differentiation in saturated markets. As consumers become more discerning, ingredient transparency takes center stage, with many seeking products devoid of contentious synthetic components.

This shift in consumer preference poses formulation challenges for brands. They grapple with maintaining a natural image while meeting performance standards, especially in color and styling applications where synthetics have historically outperformed. To navigate this, hybrid formulations are gaining traction, melding natural actives with select synthetic ingredients to strike a balance between sustainability and efficacy. Furthermore, EU regulatory changes bolster the natural ingredient movement, curbing certain synthetic components and clarifying guidelines for marketing natural products.

List of Companies Covered in this Report:

- Henkel AG and Co. KGaA

- L'Oreal SA

- Procter and Gamble Co.

- Unilever PLC

- Beiersdorf AG

- Coty Inc.

- Shiseido Co., Ltd.

- Estee Lauder Companies

- Amway Corporation

- Oriflame Cosmetics

- Kao Corporation

- Revlon Inc.

- Kenvue

- Unilever PLC

- LVMH (Moet Hennessy Louis Vuitton)

- LG Household and Health Care

- Moroccanoil

- Olaplex

- Davines S.p.A.

- Paul Mitchell/John Paul Mitchell Systems

- Lush GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing population spurring scalp-health products

- 4.2.2 Greater demand for premium and customized hair care

- 4.2.3 Rising demand for natural/organic formulations

- 4.2.4 Influence of social media and celebrity endorsements

- 4.2.5 Product innovation and packaging

- 4.2.6 Trend toward multipurpose and convenient products

- 4.3 Market Restraints

- 4.3.1 Saturated market and high brand rivalry

- 4.3.2 Price sensitivity amid private-label rise

- 4.3.3 Consumer skepticism about product claims

- 4.3.4 Regulatory challenges and compliance costs

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porte's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Shampoo

- 5.1.2 Conditioner

- 5.1.3 Hair Colorants

- 5.1.4 Hair Styling Products

- 5.1.5 Other Product Types

- 5.2 By Category

- 5.2.1 Synthetic/Conventional

- 5.2.2 Natural /Organic

- 5.3 By Price Tier

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/ Hypermarkets

- 5.4.2 Specialty Stores

- 5.4.3 Convenience Stores

- 5.4.4 Online Retail Stores

- 5.4.5 Other Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Henkel AG and Co. KGaA

- 6.4.2 L'Oreal SA

- 6.4.3 Procter and Gamble Co.

- 6.4.4 Unilever PLC

- 6.4.5 Beiersdorf AG

- 6.4.6 Coty Inc.

- 6.4.7 Shiseido Co., Ltd.

- 6.4.8 Estee Lauder Companies

- 6.4.9 Amway Corporation

- 6.4.10 Oriflame Cosmetics

- 6.4.11 Kao Corporation

- 6.4.12 Revlon Inc.

- 6.4.13 Kenvue

- 6.4.14 Unilever PLC

- 6.4.15 LVMH (Moet Hennessy Louis Vuitton)

- 6.4.16 LG Household and Health Care

- 6.4.17 Moroccanoil

- 6.4.18 Olaplex

- 6.4.19 Davines S.p.A.

- 6.4.20 Paul Mitchell/John Paul Mitchell Systems

- 6.4.21 Lush GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK