PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061602

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061602

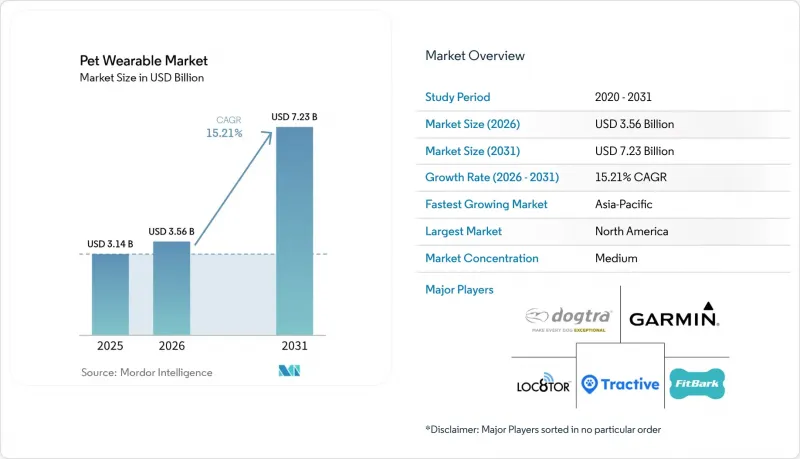

Pet Wearable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the pet wearable market size is projected to expand from USD 3.14 billion in 2025 and USD 3.56 billion in 2026 to USD 7.23 billion by 2031, registering a CAGR of 15.21% between 2026 to 2031.

This report is Segmented by Product (Smart Collars, Smart Cameras, and More), Connectivity Mode (Stand-Alone GPS, Wi-Fi Connected, and More), Animal Type (Dogs, Cats, and More), Application (Identification & Tracking, Health & Wellness Monitoring, and More), End User (Household Pet Owners, and More ) and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Pet Wearable Market Trends and Insights

Increasing Pet-Care Expenditure Fueling Market Growth

Elevated pet-care spending remains the broadest demand driver for the pet wearable market. The American Pet Products Association confirmed that the U.S. pet industry reached USD 158 billion in 2025 and is expected to move to USD 165 billion in 2026, which keeps the spending base large enough to support newer connected products. The more important shift is where that spending is going, because owners are placing more value on health-oriented and technology-enabled care than on basic discretionary items. That matters for the pet wearable market because devices linked to safety, monitoring, and wellness have a stronger case when households review spending priorities. APPA also showed that only 27% of pet owners planned to reduce pet spending over the next 12 months in 2025, which was well below the intended pullback in apparel and home goods, and that supports continued demand for higher-value pet solutions. The result is that brands positioned around pet health and prevention are better protected than those relying only on novelty or entertainment features.

Preventive Health Monitoring and Chronic-Disease Screening

Preventive monitoring is becoming one of the strongest structural supports for the pet wearable market. Invoxia's Biotracker, designed for dogs at cardiac risk, reports 92% sensitivity in detecting atrial fibrillation and tracks resting breathing rate against thresholds aligned with ACVIM guidance, showing how wearables are moving closer to clinically relevant use cases. PetPace pushed this direction further in September 2025 when it launched V3.0 of its AI smart collar with epilepsy episode monitoring for dogs, giving veterinarians and owners a more precise record for diagnosis and treatment planning. These launches matter because the pet wearable market is no longer driven only by pet recovery after escape or loss. Continuous monitoring creates a reason to keep the device active every day, which lifts retention and strengthens subscription revenue. Veterinary support also becomes a practical distribution advantage, because products with stronger clinical positioning are harder for less validated competitors to displace.

Upfront Device and Recurring Subscription Costs

Pricing remains the most immediate barrier to broader household adoption in the pet wearable market. Premium AI-enabled smart collars still sit between USD 200 and USD 599, and recurring data plans can add another USD 96 to USD 360 each year. That total cost is manageable for upper-income owners in North America and Western Europe, but it remains difficult for many buyers in Latin America, Southeast Asia, and parts of the Middle East and Africa. The challenge is not only the hardware price, because mandatory subscriptions also make the long-term commitment harder to justify for first-time users. When a device is framed as a nice-to-have tracker instead of a health or safety tool, value-seeking households are far more likely to delay the purchase. Brands that cannot separate entry hardware from premium analytics will limit the scale potential of the pet wearable market in lower-income and high-growth geographies.

Other drivers and restraints analyzed in the detailed report include:

- GPS Safety, Geofencing, and Lost-Pet Recovery Demand

- IoT, AI, and Sensor Miniaturization

- Data Privacy, Consent, and Interoperability Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart collars held 63.55% of the pet wearable market size in 2025, which shows that the collar remains the main platform for GPS, biometrics, and behavioral analytics. The segment leads because it sits on the animal throughout the day and can capture continuous data without adding extra friction for owners. That daily contact gives smart collars an advantage over more occasional or place-based devices such as cameras. Fi reinforced this segment in March 2026 with Fi Intelligence, an AI health companion that uses its canine dataset to deliver personalized insights and let owners upload veterinary records into one health profile. Health-specific wearables are also emerging as a more clinical layer inside the pet wearable industry, and PetPace Health 2.0 was named IoT Wearable Device of the Year in January 2025, which supported the shift toward medically oriented positioning.

Smart cameras are projected to grow at a 15.89% CAGR through 2031, making them the fastest-growing product line in the pet wearable market. Demand is tied to dual-income households that want remote visibility, interaction, and feeding support while away from home. The category is benefiting from lower hardware costs and the more common use of two-way audio and AI detection. At the same time, camera hardware is becoming easier to replicate, so the pet wearable market is likely to reward brands that connect cameras to broader health and alert ecosystems rather than selling them as isolated devices.

Stand-alone GPS accounted for 44.87% of the 2025 market, which reflects the continued importance of dependable tracking in outdoor and low-connectivity settings. This segment still serves hunters, ranchers, and trail users who value purpose-built reliability more than a broad feature stack. Garmin's Alpha systems show why this remains durable, because the product family combines multi-GNSS reception with field-oriented coverage support for working and sporting dogs. Cellular and Wi-Fi modes remain more attractive for urban and suburban users who need seamless app access rather than rugged field performance. The pet wearable market still depends on GPS credibility because owners will tolerate fewer compromises in safety-related functions than in lifestyle features.

Hybrid multi-connectivity is forecast to expand at a 16.18% CAGR through 2031, which makes it the fastest-growing connectivity mode in the pet wearable market. The value of hybrid design is that it reduces dead zones by switching between satellite, LTE-M, Wi-Fi, and Bluetooth based on the environment and battery needs. That shift matters because pet movement often crosses indoor, outdoor, urban, and semi-rural settings in one normal day. Connectivity architecture is therefore becoming a true differentiator in the pet wearable industry, especially when smart switching improves battery life and reliability at the same time. Brands that own this firmware layer are less exposed to hardware commoditization than those competing only on a GPS chip or a radio module.

Geography Analysis

North America held 41.88% of the pet wearable market share in 2025, and the region remains the largest base for subscriptions, connected monitoring, and premium device adoption. The United States drove most of that position, with 95 million pet-owning households in 2025 and dog ownership reaching 71 million households, which was 4 million higher than in 2024. The region also benefits from strong mobile network coverage that supports LTE-M tracking and from a veterinary system that is more ready to use remote monitoring tools in normal care routines. Pet insurance adoption is helping as well because device-linked benefits make wearables easier to justify for health and safety use cases. Fi's expansion path, which moved through Canada before broader rollout into the UK and EU in March 2026, shows that North America still functions as the main launch platform for international scale.

Europe is the second-largest region in the pet wearable market, with Germany standing out because buyers place strong value on technically reliable and certified devices. The UK, France, Spain, and Italy follow as important mid-tier markets where cat ownership trends, urban living, and rising insurance use are supporting device demand. Europe also has a clearer path toward insurer-linked adoption as reimbursement models begin to appear in pet care. At the same time, GDPR Article 5 data minimization and EDPS Opinion 22/2024 raise the design bar for connected products that handle location or health data, which makes privacy-ready development more important in this region.

Asia-Pacific is forecast to grow at a 17.62% CAGR through 2031, which makes it the fastest-expanding regional opportunity in the pet wearable market. China, India, and South Korea are the main growth engines because companion-animal ownership is increasing while urban living makes safety and monitoring more relevant. Japan and Australia are more established markets where clinical-grade devices can sustain pricing closer to North American levels. The Middle East and Africa remains earlier in adoption, with GCC countries led by the UAE and Saudi Arabia showing the strongest premium demand, while South Africa is the main sub-Saharan market. South America is led by Brazil, where the primary demand still centers on GPS-enabled tracking, and the rest of the region adds gradual growth as middle-class pet spending increases.

- Datamars

- Dogtra

- Fi

- FitBark

- Garmin

- Halo Collar Inc.

- Invoxia

- Link My Pet

- Loc8tor

- Pawfit

- PETFON

- Petcube Inc.

- PetSafe

- PETKIT

- PetPace

- PitPat

- SATELLAI

- Sure Petcare

- Tractive GmbH

- Weenect

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Pet-Care Expenditure Fueling Market Growth

- 4.2.2 Preventive Health Monitoring and Chronic-Disease Screening

- 4.2.3 GPS Safety, Geofencing, and Lost-Pet Recovery Demand

- 4.2.4 IoT, AI, And Sensor Miniaturization

- 4.2.5 Tele-Veterinary and Pet-Insurance Data Integration

- 4.2.6 Cat-Specific and Small-Pet Wearable Miniaturization

- 4.3 Market Restraints

- 4.3.1 Upfront Device and Recurring Subscription Costs

- 4.3.2 Battery Life, Charging Frequency, and Outdoor Durability Constraints

- 4.3.3 Data Privacy, Consent, and Interoperability Compliance Burden

- 4.3.4 Counterfeit And Low-Accuracy Devices Undermining Owner Trust

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Smart Collars

- 5.1.2 Smart Cameras

- 5.1.3 Smart Harnesses & Vests

- 5.1.4 Smart Tags & Clip-on Trackers

- 5.1.5 Health Monitoring Wearables

- 5.2 By Connectivity Mode

- 5.2.1 Stand-alone GPS

- 5.2.2 Cellular-connected

- 5.2.3 Wi-Fi-connected

- 5.2.4 Hybrid Multi-connectivity

- 5.2.5 Satellite-connected

- 5.3 By Animal Type

- 5.3.1 Dogs

- 5.3.2 Cats

- 5.3.3 Other Companion Animals

- 5.4 By Application

- 5.4.1 Identification & Tracking

- 5.4.2 Health & Wellness Monitoring

- 5.4.3 Medical Diagnosis & Treatment

- 5.4.4 Behavior Monitoring & Control

- 5.4.5 Safety, Security & Facilitation

- 5.5 By End User

- 5.5.1 Household Pet Owners

- 5.5.2 Veterinary Hospitals & Clinics

- 5.5.3 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Datamars

- 6.3.2 Dogtra

- 6.3.3 Fi

- 6.3.4 FitBark Inc.

- 6.3.5 Garmin Ltd.

- 6.3.6 Halo Collar Inc.

- 6.3.7 Invoxia

- 6.3.8 Link My Pet

- 6.3.9 Loc8tor Ltd.

- 6.3.10 Pawfit

- 6.3.11 PETFON

- 6.3.12 Petcube Inc.

- 6.3.13 PetSafe

- 6.3.14 PETKIT

- 6.3.15 PetPace Ltd.

- 6.3.16 PitPat

- 6.3.17 SATELLAI

- 6.3.18 Sure Petcare

- 6.3.19 Tractive GmbH

- 6.3.20 Weenect

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment