PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061605

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061605

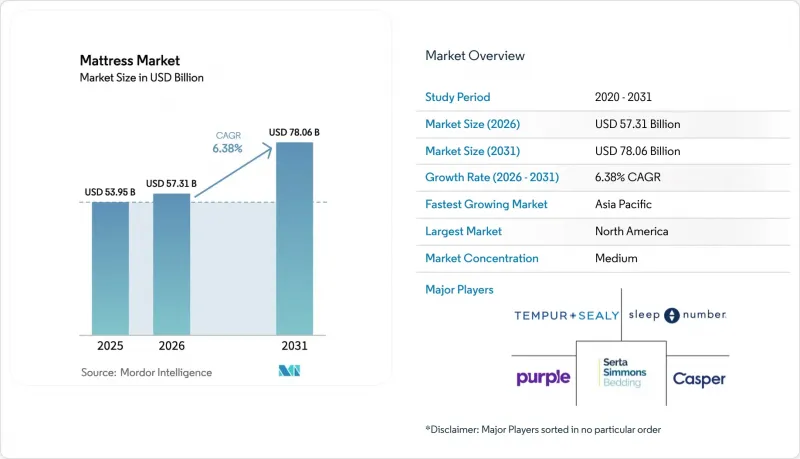

Mattress - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the mattress market size is projected to be USD 53.95 billion in 2025, USD 57.31 billion in 2026, and reach USD 78.06 billion by 2031, growing at a CAGR of 6.38% from 2026 to 2031.

This report is Segmented by Mattress Type (Innerspring, Foam, Latex, Hybrid, Gel, Other), Size (Single, Double, Queen, and More), End User (Residential, Commercial), Distribution Channel (B2B, B2C Including Specialty Stores, Multi-Brand Stores, Online, Other), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Mattress Market Trends and Insights

Heightened sleep-health consciousness & premium spend shift

The State of Sleep Health in America report indicates that many United States adults struggle to get adequate restorative sleep, with 1 in 3 not meeting recommended levels, while over half (55%) consider good sleep a major priority. This reflects a growing awareness of sleep's importance for overall health and wellness, driving demand for products that enhance rest quality. In the United States, households increasingly seek mattresses that provide measurable benefits, including orthopedic support, temperature regulation, and allergen control, often guided by physician advice or wellness routines. Similar trends are emerging in urban India, where consumers view high-quality beds as long-term wellness investments, encouraging trade-up behavior toward premium designs. Brands are responding by emphasizing scientifically backed sleep benefits, durable construction, and advanced features that justify higher price points. Marketing is increasingly focused on objective outcomes rather than brand or price alone, supporting the global growth of premium mattresses.

Direct-to-consumer e-commerce boom

Digital-first buying journeys are reshaping the mattress market, but the most effective strategies now combine online convenience with in-person testing to reduce uncertainty about comfort and support. Omnichannel retail models link local showrooms with regional digital marketing and customer care, helping lower return rates and build consumer trust. In India, expanding logistics networks into tier-2 and tier-3 cities, flexible payment options, and localized content are making it easier for first-time buyers to access premium mattresses. Brands are enhancing e-commerce platforms with appointment-based consultations, home trials, and improved site experiences to address fit and delivery concerns that previously limited online adoption. This integrated approach strengthens lifetime value, boosts conversion in high-intent areas, and enhances resilience across demand cycles. The United States Census Bureau reports that retail e-commerce accounted for 16.4% of total United States retail sales in Q3 2025, highlighting sustained growth in online channels and the expanding role of D2C strategies in the mattress market.

Volatile petro-foam, coil & latex input costs

Feedstock volatility has raised the difficulty of budgeting core inputs, and quarterly swings in polyurethane resin pricing create margin pressure on entry-level assortments. Regional price trends show asynchronous movements, which complicates global sourcing and makes contract coverage and inventory position more critical for the mattress market. Shipping-route disruptions lifted container costs well above historical averages in 2024 and forced manufacturers to layer surcharges across quarters to manage working capital and landed costs. Latex markets tightened as weather and disease lowered yields in key producing countries, a pattern that continued into 2025 with expectations of production shortfalls that kept replacement costs elevated for latex-forward SKUs. Vertically integrated producers with captive foam capacity and scale procurement hold an advantage during these cycles because they can react faster to mix-shift and pass-through.

Other drivers and restraints analyzed in the detailed report include:

- Global hospitality & real-estate buildout

- Breakthrough cooling & adaptive material technology

- EPR regulations elevating end-of-life disposal expenses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Innerspring mattresses held a 43.44% market share in 2025, reflecting the scale of legacy demand and price accessibility in value-oriented channels for the mattress market. The format remains familiar for replacement purchases across mature markets, with regional suppliers catering to tight budgets and high turn ratios. Latex products are positioned on support, breathability, and allergen resistance, and they benefit from circular economy messaging in urban buyers who emphasize durable and recyclable builds. Hybrid constructions blend coils with latex or gel foams to create targeted responsiveness and airflow, and they continue to anchor new premium launches across brand portfolios. The result is a type of mix where entry price points lean on innerspring volume while higher tiers expand variety through latex-forward and hybrid options that defend premium price realization.

Latex is the fastest-growing segment at a CAGR of 9.87% through 2031, as consumers link firmness profiles and orthopedic benefits to better daily comfort and long-term posture management in the mattress market. Durability and ventilation resonate in humid climates, and dust-mite resistance carries additional weight in Indian metros with prolonged warm seasons. The value proposition supports above-average trade-up rates in urban channels as shoppers move from foam or basic spring builds to latex or hybrid designs. Suppliers strengthen the narrative with clearer material disclosures and independent certifications where feasible, which support trust at checkout. As education improves and test-lie opportunities widen, latex and hybrids continue to capture new-to-premium demand without displacing entrenched innerspring volume at the mass end.

Queen-size held 48.35% of the market in 2025, a function of room dimensions in standard apartments and the balance between surface area and footprint in the mattress market. The format remains the chief choice in mid-market master bedrooms and in new flat sales where developers design for queen footprints. Trading up to king-size has gained momentum as owners prioritize personal space, co-sleeping accommodations, and overall sleep comfort in core living spaces. Hospitality specifications also favor larger formats in suites and premium rooms, which influence consumer preference after stay experiences. Retailers reflect this mix with deeper queen assortments and targeted king expansions in metros and suburbs with larger average bedrooms.

King-size records the fastest growth rate at 8.64% through 2031 as post-2020 home layouts and discretionary comfort improvements remain in focus in affluent cohorts. The pattern shows up in India's premium residential towers and independent housing, where bedroom layouts support bigger frames. As renovation cycles advance in upper mid-income households, larger mattresses migrate from aspiration to planned purchase in multi-year home budgets. Hospitality pipelines that specify premium bedding keep r egular volume flowing in king sizes, which sustains manufacturing runs and scale. With room-by-room planning and higher awareness of ergonomic benefits, larger formats hold share gains even as queen-size remains the anchor of the consumer stack for the mattress market.

Geography Analysis

North America accounted for 36.39% of the mattress market in 2025, but shipments declined as replacement cycles lengthened and consumers shifted spending toward experiences. Extended Producer Responsibility programs and environmental fees are impacting pricing and margins for budget models. Brands are strengthening omnichannel strategies, using physical stores to boost online conversions through local fulfillment and test-and-try models. Larger players continue vertical integration, aligning foam capacity, retail banners, and brand portfolios to maintain service levels and working capital efficiency. In contrast, Asia-Pacific is the fastest-growing region at an 8.54% CAGR through 2031, driven by rising incomes, urbanization, and construction activity that fuels new households and hotels.

China's secondary urban centers are adopting hybrid and gel-cooled mattresses, while tier-1 buyers focus on performance and brand trust. India's organized retail is expanding into tier-2 and tier-3 cities, with delivery networks and payment options enabling first-time buyers. Southeast Asia and India face latex supply dynamics, with potential shortfalls prompting attention to sourcing alternatives. Consumers across the region increasingly differentiate by cooling, orthopedic support, and material transparency, boosting premium segment growth. Rising urban populations and disposable incomes further support demand for mid- and high-tier mattresses.

Europe is seeing growth in sustainability-focused mattresses, especially in Germany, Sweden, and the Netherlands, where digital product passports improve traceability and recycling readiness. Circular initiatives, such as foam-to-foam recycling, are reducing emissions and returning materials to furniture production, while mature EPR programs in France, Belgium, and the Netherlands are raising compliance requirements for manufacturers. In South America, trends are mixed; Brazil benefits from urban housing programs, but inflation is limiting purchasing power and extending replacement cycles. Chile, Peru, and Argentina are gradually adopting e-commerce, though logistics and payment challenges remain. Local manufacturers are leveraging cotton, wool, and eucalyptus to compete on price with imported foam and latex, while export-oriented producers pursue ISO and OEKO-TEX certifications for hospitality markets.

- Tempur Sealy International Inc.

- Serta Simmons Bedding LLC

- Sleep Number Corporation

- Casper Sleep Inc.

- Purple Innovation Inc.

- KING KOIL Inc.

- Kingsdown Inc.

- Southerland Bedding Co.

- Spring Air Company

- Sealy Corporation

- Emma Sleep GmbH

- Saatva Inc.

- Sheela Foam Ltd (Sleepwell)

- Kurl-On Enterprises Ltd

- Leggett & Platt Incorporated

- IKEA

- Paramount Bed Holdings Co. Ltd

- Eight Sleep Inc.

- ReST Performance Mattress

- Airweave Inc.

- Dunlopillo GmbH

- Hastens

- Nectar Sleep

- Simba Sleep

- DreamCloud

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened sleep-health consciousness and shift toward premium spending

- 4.2.2 Expansion of direct-to-consumer (DTC) e-commerce channels

- 4.2.3 Global hospitality and real-estate construction growth

- 4.2.4 Advances in cooling, pressure-relief, and adaptive mattress materials

- 4.2.5 Regulatory encouragement for circular, organic, and sustainable inputs

- 4.2.6 Rising adoption of AI- and IoT-enabled smart mattresses

- 4.3 Market Restraints

- 4.3.1 Volatility in raw material costs (petro-foam, coils, latex)

- 4.3.2 Lengthening replacement cycles in mature markets

- 4.3.3 Higher compliance and disposal costs due to extended producer responsibility (EPR) regulations

- 4.3.4 Limited availability of certified bio-latex and natural fiber inputs

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Mattress Type

- 5.1.1 Innerspring Mattresses

- 5.1.2 Foam Mattresses (including memory foam)

- 5.1.3 Latex Mattresses

- 5.1.4 Hybrid Mattresses

- 5.1.5 Gel Mattresses

- 5.1.6 Other Mattresses

- 5.2 By Size

- 5.2.1 Single-size

- 5.2.2 Double-size

- 5.2.3 Queen-size

- 5.2.4 King-size

- 5.2.5 Other Sizes

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Distribution Channel

- 5.4.1 B2B/Directly from the Manufacturers

- 5.4.2 B2C/Retail Channels

- 5.4.2.1 Specialty Bedding and Mattress Stores

- 5.4.2.2 Multi-brand Stores/Home Centers

- 5.4.2.3 Online

- 5.4.2.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East And Africa

- 5.5.5.1 United Arab of Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Tempur Sealy International Inc.

- 6.4.2 Serta Simmons Bedding LLC

- 6.4.3 Sleep Number Corporation

- 6.4.4 Casper Sleep Inc.

- 6.4.5 Purple Innovation Inc.

- 6.4.6 KING KOIL Inc.

- 6.4.7 Kingsdown Inc.

- 6.4.8 Southerland Bedding Co.

- 6.4.9 Spring Air Company

- 6.4.10 Sealy Corporation

- 6.4.11 Emma Sleep GmbH

- 6.4.12 Saatva Inc.

- 6.4.13 Sheela Foam Ltd (Sleepwell)

- 6.4.14 Kurl-On Enterprises Ltd

- 6.4.15 Leggett & Platt Incorporated

- 6.4.16 IKEA

- 6.4.17 Paramount Bed Holdings Co. Ltd

- 6.4.18 Eight Sleep Inc.

- 6.4.19 ReST Performance Mattress

- 6.4.20 Airweave Inc.

- 6.4.21 Dunlopillo GmbH

- 6.4.22 Hastens

- 6.4.23 Nectar Sleep

- 6.4.24 Simba Sleep

- 6.4.25 DreamCloud

7 Market Opportunities & Future Outlook

- 7.1 Rising demand for customized and digitally enabled mattresses