PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061671

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061671

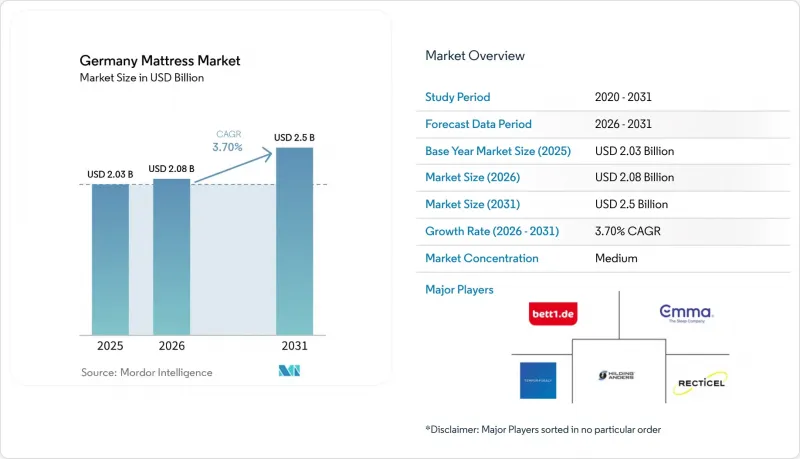

Germany Mattress - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany mattress market size is expected to increase from USD 2.03 billion in 2025 to USD 2.08 billion in 2026 and reach USD 2.5 billion by 2031, growing at a CAGR of 3.70% over 2026-2031.

This report is Segmented by Type (Spring Mattresses, Memory Foam Mattresses, Latex Mattresses, Other Mattresses), Distribution Channel (Online, Offline), End User (Residential, Commercial), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Germany Mattress Market Trends and Insights

Rising consumer focus on sleep-health & premium comfort

Urban professionals increasingly treat restorative sleep as a core pillar of preventive healthcare, prompting a pivot toward mattresses that advertise orthopedic alignment and certified low-VOC materials. Stiftung Warentest's detailed scoring rubrics make performance data widely accessible, accelerating informed decision-making that favors high-spec products. Direct-to-consumer pioneer Bett1.de leveraged this scrutiny by positioning its BODYGUARD line as "anti-cartel" value, a message that resonated across age cohorts and helped shift perceptions about fair pricing. As affluent buyers gravitate to multilayer memory foam systems that modulate micro-climate and relieve pressure points, premium units proliferate in the Germany mattress market. Marketing narratives now foreground quantified benefits such as reduced tossing frequency and improved spinal curvature, translating abstract comfort claims into actionable metrics. This convergence of objective testing, health literacy, and brand storytelling reinforces willingness to pay and sustains the driver's medium-term uplift on market growth.

E-commerce expansion lowers go-to-market costs

Bed-in-box pioneers demonstrated that compressible foam could be shipped safely, thereby removing the showroom bottleneck that long limited category e-commerce penetration. The Germany mattress market benefited from postal codes that receive next-day deliveries and statutory 14-day return rights, both of which shrink perceived risk and fuel repeat purchases. Brands deploy data analytics to refine advertising spend, achieving customer-acquisition costs materially below traditional retail margins and redirecting savings into R&D. Pandemic-era digital habits linger, so even older cohorts now shop for big-ticket items online, elevating basket sizes on web and app interfaces. Brick-and-mortar incumbents responded by launching click-and-collect services and virtual consultation widgets, which reposition floor space as experiential rather than transactional. Consequently, omnichannel frameworks are no longer optional; they are central to defending share as pure online specialists scale. With last-mile carbon footprints under scrutiny, several operators introduced electric-van fleets, combining speed with sustainability to reinforce brand promises.

Market saturation & long replacement cycle

Penetration in mature regions approaches 1 mattress per adult, limiting upside from first-time buyers and shifting competitive focus to replacement frequency. German sleepers traditionally keep mattresses for 8-12 years, a tenure that tempers annual turnover despite population growth. Extended warranties offered by premium brands, while attractive to consumers, also elongate replacement intent and thus drag on volume. Aggressive promotional tactics aimed at accelerating upgrade decisions sometimes erode category value by conditioning shoppers to wait for discounts. Additionally, smaller urban dwellings increasingly opt for convertible sofa-beds, shrinking the addressable unit base in dense metros. The restraint's long-term effect reflects the structural nature of demographic density and cultural frugality, both of which resist quick remediation.

Other drivers and restraints analyzed in the detailed report include:

- Higher disposable income & renovation cycles

- Sustainability regulations are pushing climate-neutral mattresses

- Escalating EU foam/latex input costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spring units continue to dominate with a 41.12% share of the German mattress market in 2025, underscoring consumer comfort with established coil technology. Nevertheless, the memory-foam segment is forecast at a 7.84% CAGR, signaling a premium pivot fuelled by thermal-management gels and zoned support foams that visibly differentiate performance. Latex formats enjoy a loyal following among allergy-sensitive buyers and eco-conscious households, though their higher ticket price constrains mass uptake. Hybrid models that marry pocket springs with viscoelastic layers blur categorical boundaries, allowing legacy manufacturers to defend relevance against foam specialists. Testing frameworks from EUROPUR calibrate resilience and indentation parameters, creating a level field where quality claims can be audited and thus trusted by German shoppers. Marketing narratives now revolve around sleep-stage analytics, presenting memory foam as conducive to prolonged deep-sleep intervals, which enhances daily cognitive performance. Because these health benefits withstand third-party validation, they increasingly command higher average selling prices and lift total revenue despite modest unit share gains in the Germany mattress market.

Memory-foam advancements resonate with e-commerce's box-shipping format, giving digital-native labels cost advantages that play well in Germany's tightly regulated logistics arena. Compression technology permits container densification, lowering per-unit freight emissions, an attribute highlighted in sustainability scorecards. Spring-oriented incumbents respond with micro-coil layers that simulate foam contouring while retaining their legacy know-how, protecting their base amid technological disruption. Meanwhile, latex producers bundle cradle-to-cradle certifications to reinforce green leadership, winning niche yet profitable contracts with boutique hotels that brand themselves eco-neutral. Collectively, the type segmentation showcases how innovation breadth-not just absolute market share-drives brand elevation and margin capture within the Germany mattress market.

List of Companies Covered in this Report:

- Bett1.de GmbH

- Emma Sleep GmbH

- Tempur Sealy International Inc.

- Hilding Anders International AB

- Recticel NV (Schlaraffia)

- Casper Sleep Inc.

- Matratzen Concord GmbH (Beter Bed)

- Breckle GmbH & Co. KG

- Diamona GmbH

- Rummel Matratzen

- Ravensberger Matratzen GmbH

- Hukla Matratzen GmbH

- Badenia Bettcomfort GmbH & Co. KG

- Werkmeister Manufaktur GmbH

- Sembella GmbH

- OTTO Group (Schlafwelt)

- IKEA Deutschland GmbH & Co. KG

- JYSK GmbH

- Schlafkomfort Frankenstolz KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising consumer focus on sleep-health & premium comfort

- 4.2.2 E-commerce expansion lowering go-to-market costs

- 4.2.3 Higher disposable income & renovation cycles

- 4.2.4 Sustainability regulations pushing climate-neutral mattresses

- 4.2.5 Corporate incentives for ergonomic nap areas in offices

- 4.2.6 German Supply-Chain Act Favors Local Sourcing

- 4.3 Market Restraints

- 4.3.1 Market saturation & long replacement cycle

- 4.3.2 Escalating EU foam/latex input costs

- 4.3.3 Strict fire-safety / recyclability compliance costs

- 4.3.4 Urban switch to sofa-beds reducing mattress purchases

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Spring Mattresses

- 5.1.2 Memory Foam Mattresses

- 5.1.3 Latex Mattresses

- 5.1.4 Other Mattresses

- 5.2 By Distribution Channel

- 5.2.1 Online

- 5.2.2 Offline

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Region

- 5.4.1 Baden-Wurttemberg

- 5.4.2 Bavaria

- 5.4.3 Berlin

- 5.4.4 Brandenburg

- 5.4.5 Bremen

- 5.4.6 Hamburg

- 5.4.7 North Rhine-Westphalia

- 5.4.8 Rest of Germany

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Bett1.de GmbH

- 6.4.2 Emma Sleep GmbH

- 6.4.3 Tempur Sealy International Inc.

- 6.4.4 Hilding Anders International AB

- 6.4.5 Recticel NV (Schlaraffia)

- 6.4.6 Casper Sleep Inc.

- 6.4.7 Matratzen Concord GmbH (Beter Bed)

- 6.4.8 Breckle GmbH & Co. KG

- 6.4.9 Diamona GmbH

- 6.4.10 Rummel Matratzen

- 6.4.11 Ravensberger Matratzen GmbH

- 6.4.12 Hukla Matratzen GmbH

- 6.4.13 Badenia Bettcomfort GmbH & Co. KG

- 6.4.14 Werkmeister Manufaktur GmbH

- 6.4.15 Sembella GmbH

- 6.4.16 OTTO Group (Schlafwelt)

- 6.4.17 IKEA Deutschland GmbH & Co. KG

- 6.4.18 JYSK GmbH

- 6.4.19 Schlafkomfort Frankenstolz KG

7 Market Opportunities & Future Outlook

- 7.1 Smart, climate-neutral "sleep-tech" mattresses bundled with energy-efficient bedroom IoT packages

- 7.2 Subscription-based mattress replacement & recycling service targeting urban renters