PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061655

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061655

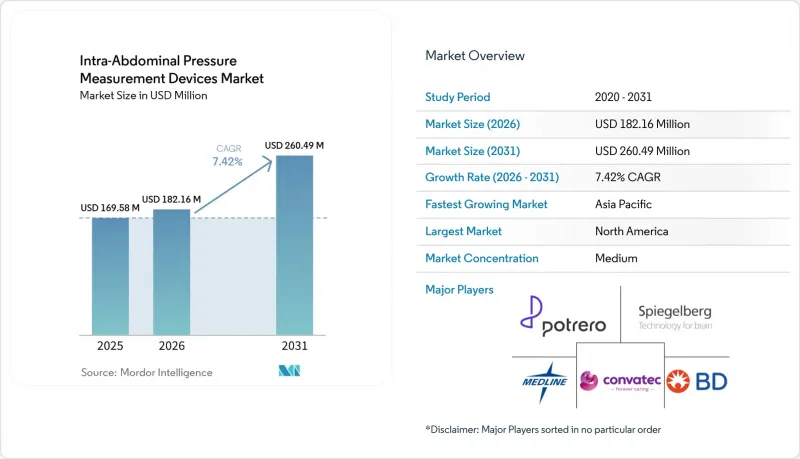

Intra-Abdominal Pressure Measurement Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the intra-Abdominal pressure measurement devices market size is projected to expand from USD 169.58 million in 2025 and USD 182.16 million in 2026 to USD 260.49 million by 2031, registering a CAGR of 7.42% between 2026 to 2031.

This report is Segmented by Product (Disposables, Equipment), Measurement Mode (Intermittent, Continuous), Measurement Technique (Indirect, Direct), Application (Intra-Abdominal Hypertension, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

Global Intra-Abdominal Pressure Measurement Devices Market Trends and Insights

Rising Prevalence Of Intra-Abdominal Hypertension & Abdominal Compartment Syndrome

Elevated pressure affects 23.7% of ICU admissions and remains an independent predictor of death, prompting intensive-care societies to mandate routine monitoring. Clinical guidelines issued by the World Society of the Abdominal Compartment Syndrome require serial readings, driving standardized purchasing in trauma, sepsis and post-operative units. Adoption is accelerating because earlier detection enables decompression before multi-organ failure develops, which aligns with hospital quality-improvement metrics. The clinical push, combined with hospital accreditation criteria and payer emphasis on outcomes, keeps the intra-abdominal pressure measurement devices market on a firm expansion path. Device makers that supply intuitive interfaces and EMR integration are positioned to benefit as protocol adherence rises across surgical and medical ICUs.

Growing ICU Bed Capacity & Critical-Care Expenditure

Asia-Pacific governments are scaling critical-care infrastructure via flagship programs such as India's Ayushman Bharat, which finances ICU beds and technology upgrades . Brazil's Tele-ICU initiative treated 5,471 patients across 15 hospitals, demonstrating how remote monitoring extends intensivist expertise to underserved regions. Capital allocations coincide with low-cost, cloud-connected monitors priced under USD 300 per bed, enabling rapid scale-up in secondary cities. As emerging markets close critical-care capacity gaps, procurement officers prioritize interoperable devices that deliver predictive analytics, a trend that favors full-suite vendors active in the intra-abdominal pressure measurement devices market. Rising public-sector outlays are therefore expected to underpin volume growth well beyond mature economies.

Under-Utilization In General Surgery; Intermittent False-Negatives

International surveys reveal that only 59% of surgeons are aware of guideline-recommended thresholds, and inconsistent timing can mask clinically significant pressure spikes. False-negative results erode confidence, discouraging routine adoption in elective cases despite evidence of improved recovery. Training gaps are pronounced in ambulatory centers where staff rotate frequently, limiting experience with bladder-based measurement technique. Surgical societies are rolling out e-learning modules, but progress remains uneven, slowing the intra-abdominal pressure measurement devices market uptake in non-ICU environments. Vendors offering sensor kits with step-by-step prompts and video tutorials can help overcome this educational barrier.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Device Miniaturization & Digital Connectivity

- Shift Toward Continuous, Non-Invasive Sensors

- Supply-Chain Constraints For MEMS Pressure Sensors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Disposables generated the largest share of revenue at USD 108.19 million in 2025, equal to 63.78% of the intra-abdominal pressure measurement devices market size, because single-use catheters align with infection-control policies in tertiary ICUs. Equipment sales climbed at 8.88% CAGR thanks to platforms that bundle pressure, cardiac output and tissue-oxygen readings for integrated hemodynamic oversight. Hospitals value disposables for predictable per-procedure cost and rapid turnover, while CFOs allocate capital budgets to smart consoles that interoperate with existing monitors. The intra-abdominal pressure measurement devices market is expected to maintain a disposables bias because regulatory bodies increasingly discourage multi-patient devices.

Equipment vendors counter by offering subscription models that amortize hardware over multi-year service contracts, thereby lowering upfront cost for mid-tier hospitals. Next-generation consoles host machine-learning-based early-warning scores that synthesize pressure readings with lactate and urine output to forecast organ dysfunction. As remote-upgrade capability becomes a purchasing criterion, companies with secure firmware pipelines and FDA-cleared analytics will capture incremental revenue share through 2031, gradually lifting equipment's contribution within the intra-abdominal pressure measurement devices market.

Intermittent measurement retained 71.40% share in 2025 as many ICUs still rely on manual bladder manometry three times daily. However, continuous systems are forecast to expand at an 8.41% CAGR, adding USD 30.3 million to the intra-abdominal pressure measurement devices market size by 2031. Clinical teams report that real-time curves reveal transient spikes during proning, pneumoperitoneum and dialysis cycles that intermittent checks overlook. Cost barriers are narrowing because consumable-per-day pricing for continuous sensors approaches that of legacy catheters.

As enhanced recovery protocols push surgeons to mobilize patients within 24 hours, the convenience of wearable sensors drives adoption beyond the operating theater into surgical wards. Policy makers evaluating bundled payment models favor technologies that shorten ICU length of stay, providing an economic tailwind. The intra-abdominal pressure measurement devices market therefore faces a gradual but durable shift as evidence and economics converge in favor of continuous data streams.

Geography Analysis

North America recorded 42.95% of global revenue in 2025 on the back of CPT-code reimbursement (e.g., 49420 and 49062) and broad ICU availability. The region benefits from early access to breakthrough devices and multi-center trials that validate AI-driven decision support. Mergers such as BD-Edwards consolidate intellectual property and national distribution, reinforcing U.S. leadership. Adoption momentum is sustained by hospital-quality metrics that link early pressure detection to reduced ventilator days, ensuring budgets for incremental sensor spending within the intra-abdominal pressure measurement devices market.

Europe commands a mature but regulation-heavy landscape shaped by MDR 2017/745, which tightens clinical-evidence demands and post-market audits. Larger corporates absorb compliance cost and gain share as smaller firms exit. Clinical societies integrate pressure monitoring into guidelines for vascular, hernia and bariatric surgery, further institutionalizing demand. Economically, pay-for-performance models in Germany and the Nordics reward early complication detection, thereby anchoring stable revenue trajectories for the intra-abdominal pressure measurement devices market across the continent.

Asia-Pacific is projected to be the fastest-growing region at 9.15% CAGR thanks to public-sector ICU expansion, domestic device manufacturing incentives and digital-health pilots that embed monitoring into smart-hospital programs. India is retrofitting municipal hospitals with cloud dashboards that pull data from low-power Bluetooth pressure probes, bridging intensivist shortages. China accelerates local production to reduce import dependency, while Japan's national AI roadmap spurs investment in algorithm-compatible sensors . Collectively, these initiatives widen addressable volumes and elevate Asia-Pacific's strategic importance within the intra-abdominal pressure measurement devices market over the forecast horizon.

- Stryker

- Convatec

- Becton, Dickinson & Co. (C. R. Bard)

- Potrero Medical Inc.

- C2DX Inc.

- Medline Industries

- Biometrix Ltd.

- Holtech Medical

- Spiegelberg

- Delta Med SpA

- FutureMed Sensors

- Affluent Medical SA

- Boston Scientific

- Teleflex

- SAM Medical Products

- Laborie Medical Technologies

- Verathon

- ICU Medical

- Getinge

- Hillrom/Baxter

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Of Intra-Abdominal Hypertension & Abdominal Compartment Syndrome

- 4.2.2 Growing ICU Bed Capacity & Critical-Care Expenditure

- 4.2.3 Rapid Device Miniaturisation & Digital Connectivity

- 4.2.4 Shift Toward Continuous, Non-Invasive Sensors

- 4.2.5 Emerging Reimbursement Codes For IAP Monitoring In US & EU

- 4.3 Market Restraints

- 4.3.1 Under-Utilisation In General Surgery; Intermittent False-Negatives

- 4.3.2 Risk Of Catheter-Associated Urinary-Tract Infections

- 4.3.3 Lack Of Global Standardisation & Training Outside Critical-Care Units

- 4.3.4 Supply-Chain Constraints For Mems Pressure Sensors

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Disposables

- 5.1.2 Equipment

- 5.2 By Measurement Mode

- 5.2.1 Intermittent

- 5.2.2 Continuous

- 5.3 By Measurement Technique

- 5.3.1 Indirect

- 5.3.2 Direct

- 5.4 By Application

- 5.4.1 Intra-abdominal Hypertension

- 5.4.2 Abdominal Compartment Syndrome

- 5.4.3 Trauma & Emergency Care

- 5.4.4 Post-surgical Monitoring

- 5.4.5 Sepsis & Multi-organ Failure

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgical Centres

- 5.5.3 Other End Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Rest of World

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Stryker Corporation

- 6.3.2 ConvaTec Group PLC

- 6.3.3 Becton, Dickinson & Co. (C. R. Bard)

- 6.3.4 Potrero Medical Inc.

- 6.3.5 C2DX Inc.

- 6.3.6 Medline Industries LP

- 6.3.7 Biometrix Ltd.

- 6.3.8 Holtech Medical

- 6.3.9 Spiegelberg GmbH

- 6.3.10 Delta Med SpA

- 6.3.11 FutureMed Sensors

- 6.3.12 Affluent Medical SA

- 6.3.13 Boston Scientific Corp.

- 6.3.14 Teleflex Inc.

- 6.3.15 SAM Medical Products

- 6.3.16 Laborie Medical Technologies

- 6.3.17 Verathon Inc.

- 6.3.18 ICU Medical Inc.

- 6.3.19 Getinge AB

- 6.3.20 Hillrom/Baxter

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment