PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063631

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063631

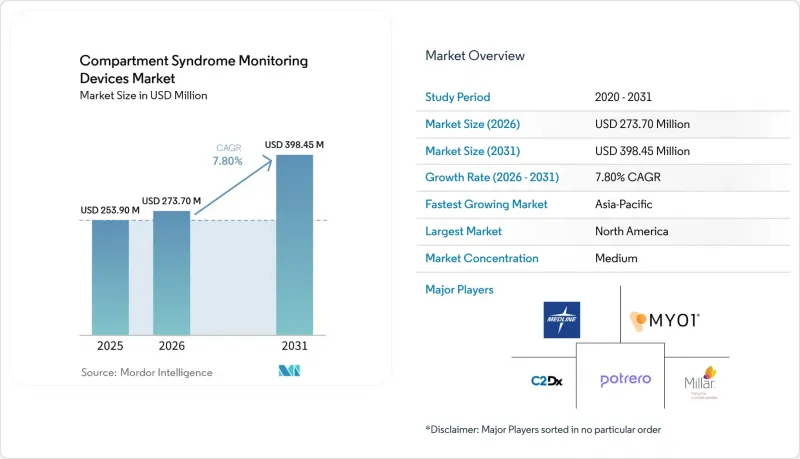

Compartment Syndrome Monitoring Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the compartment syndrome monitoring devices market size is projected to be USD 253.90 million in 2025, USD 273.70 million in 2026, and reach USD 398.45 million by 2031, growing at a CAGR of 7.80% from 2026 to 2031.

This report is Segmented by Product (Equipment, Disposables & Accessories), Technology (Invasive Monitoring Devices, and More), Syndrome Type (Acute Compartment Syndrome, and More), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Compartment Syndrome Monitoring Devices Market Trends and Insights

Rising Incidence of Trauma-Related Injuries

Global road-traffic collisions, sports fractures, and military casualties are driving an increase in acute compartment syndrome (ACS) cases, requiring prompt diagnosis. The U.S. Department of Defense has invested significant funds in its Advanced Medical Monitor program, emphasizing the importance of continuous pressure sensors for battlefield triage. Civilian trauma centers are also addressing this need, with a 2024 multicenter study involving 100 patients showing that continuous monitoring reduced amputation odds to 0.23 compared to intermittent checks. As traffic injury volumes rise in the Asia-Pacific, the demand for reliable monitoring in regional centers is growing.

Growing Clinician Awareness of Early Diagnosis

Professional societies are recommending protocolized monitoring for high-risk fractures. Research shows that performing a fasciotomy within six hours of symptom onset can reduce amputations by two-thirds, but subjective signs often delay surgery. Clinicians are increasingly relying on objective thresholds, such as maintaining a delta pressure below 30 mmHg. In the United States, malpractice insurers consider documented pressure trends as a risk mitigation measure, encouraging hospitals to invest in necessary capital purchases. Simulation training in academic centers is enhancing proficiency, establishing continuous monitoring systems as the emerging standard of care.

High Device & Disposable Costs

Capital units can cost up to USD 25,000, and single-use catheters cost USD 400, putting financial pressure on smaller hospitals. A 2024 analysis identified net 60-day savings of USD 2,789 per patient due to fewer fasciotomies and shorter hospital stays. However, these savings benefit hospital finance teams rather than the departments responsible for funding the equipment, leading to budget misalignment. India's 2024 production linked incentive scheme aims to localize manufacturing, but the benefits are not expected to materialize before 2027.

Other drivers and restraints analyzed in the detailed report include:

- Advances in Continuous & Wireless Monitorin

- AI-Driven Predictive Alert Systems

- Mixed Clinical-Outcome Evidence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Disposables are expected to surpass equipment as hospitals focus on infection-control compliance and predictable cost structures. The preference for single-use catheters aligns with the razor-and-blade model, enhancing profitability for suppliers. Equipment manufacturers are introducing modular consoles that activate premium software through licenses, combining capital affordability with long-term annuity streams. This strategic approach is likely to sustain the growth of the compartment syndrome monitoring devices market even after core capital placements reach saturation.

The shift towards disposables is particularly evident in ambulatory surgical centers, where lower upfront costs outweigh resistance to higher per-case fees. These facilities transfer catheter expenses to payers under fee-for-service rules, supporting a 9.08% compound annual growth rate through 2031 for consumables. Leading orthopedic companies are already reporting double-digit growth in single-use monitoring portfolios, indicating that consumables will play a key role in margin expansion across the compartment syndrome monitoring devices market.

Non-invasive and minimally invasive systems are poised to gain market share as clinicians aim to reduce catheter-related complications. While invasive devices maintained a 54.06% lead in 2025, emerging bioimpedance and near-infrared platforms are growing rapidly at a 9.55% rate, outpacing the overall compartment syndrome monitoring devices market growth. Early-adopter trauma centers are validating the accuracy of these platforms, and regulatory pathways are becoming clearer following positive pilot data linking bioimpedance readings to invasive gold standards.

For community hospitals and sports clinics, non-invasive probes offer faster learning curves and simplified credentialing. Eliminating puncture risks also expands their use in anticoagulated or coagulopathic patients. As manufacturing volumes increase, component costs are expected to decline, narrowing price differences. Combined with AI analytics, contactless monitoring could eventually become the primary approach, relegating catheters to niche high-acuity scenarios.

Geography Analysis

In 2025, North America secured 41.13% of the revenue share, supported by its extensive network of Level I and II trauma centers and the FDA's predictable 510(k) pathway, which expedites market entry. The introduction of the October 2025 Transitional Pass-Through and New Technology Add-on Payments for MY01 established a dedicated reimbursement channel, accelerating hospital adoption and validating premium device pricing. US quality programs have now integrated compartment pressure monitoring into their benchmarks, aligning financial incentives with its adoption.

Asia-Pacific emerges as the fastest-growing region, achieving an 8.80% CAGR, driven by road-traffic injuries and government incentives for local device assembly. MedTech clusters in India have reduced manufacturing costs by up to 40%, promoting domestic production that competes with imports. China's expansion of trauma centers, along with Japan's premium market catering to its aging population, ensures consistent demand. However, US tariffs on Japanese sensors have prompted a shift in some assembly operations to Southeast Asia. While Australia's trauma network is relatively smaller, it serves as a crucial English-language regulatory platform, with many multinationals leveraging it for pilot deployments.

Europe grapples with EU MDR bottlenecks, causing delays in sterilization validations and extending launch cycles compared to North America. Germany is considering a distinct DRG code that could transform the economic landscape, but its implementation is unlikely before 2027. The UK's NICE evaluation of non-invasive devices will play a pivotal role in shaping procurement decisions amidst tight NHS budgets. Southern Europe lags in trauma-center density, resulting in a fragmented adoption curve, where northern markets lead and their southern counterparts trail by three to five years.

- B. Braun

- Beckton Dickinson

- Biometrix Ltd. (3i Group)

- Centurion Medical Products

- Convatec

- Critical Care Diagnostics (C2DX), Inc.

- DePuy Synthes

- Gaeltec Devices Ltd.

- Integra LifeSciences

- Medline Industries

- Millar, Inc.

- MY01, Inc.

- Perimed

- Potrero Medical

- Raumedic

- Smiths Group

- Spiegelberg

- Stryker

- Terumo

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Trauma-Related Injuries

- 4.2.2 Growing Clinician Awareness of Early Diagnosis

- 4.2.3 Advances in Continuous & Wireless Monitoring

- 4.2.4 AI-Driven Predictive Alert Systems

- 4.2.5 Reimbursement Code Updates in Key Markets

- 4.2.6 Military Field-Care Procurement Surge

- 4.3 Market Restraints

- 4.3.1 High Device & Disposable Costs

- 4.3.2 Mixed Clinical-Outcome Evidence

- 4.3.3 EU MDR Sterilization Validation Delays

- 4.3.4 Tariff-Driven Component Cost Volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Equipment

- 5.1.2 Disposables & Accessories

- 5.2 By Technology

- 5.2.1 Invasive Monitoring Devices

- 5.2.2 Non-Invasive / Minimally Invasive Devices

- 5.3 By Syndrome Type

- 5.3.1 Acute Compartment Syndrome

- 5.3.2 Chronic/Exertional Compartment Syndrome

- 5.3.3 Abdominal Compartment Syndrome

- 5.4 By End User

- 5.4.1 Hospitals (Level I/II Trauma)

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Orthopaedic & Sports Medicine Clinics

- 5.4.4 Military & Emergency Medical Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of MEA

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 B. Braun Melsungen AG

- 6.3.2 Becton, Dickinson and Company (BD)

- 6.3.3 Biometrix Ltd. (3i Group)

- 6.3.4 Centurion Medical Products

- 6.3.5 ConvaTec Group PLC

- 6.3.6 Critical Care Diagnostics (C2DX), Inc.

- 6.3.7 DePuy Synthes

- 6.3.8 Gaeltec Devices Ltd.

- 6.3.9 Integra LifeSciences

- 6.3.10 Medline Industries, Inc.

- 6.3.11 Millar, Inc.

- 6.3.12 MY01, Inc.

- 6.3.13 Perimed AB

- 6.3.14 Potrero Medical

- 6.3.15 Raumedic AG

- 6.3.16 Smith & Nephew plc

- 6.3.17 Spiegelberg GmbH & Co. KG

- 6.3.18 Stryker Corporation

- 6.3.19 Terumo Corporation

- 6.3.20 Zimmer Biomet Holdings, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment