PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061657

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061657

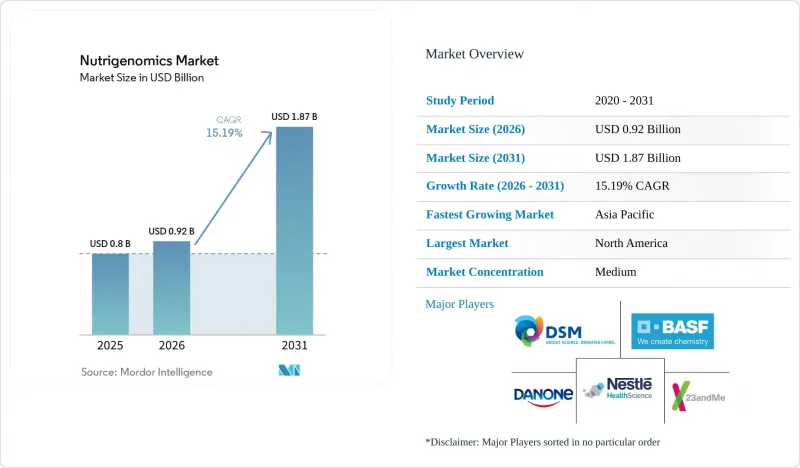

Nutrigenomics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, nutrigenomics market size in 2026 is estimated at USD 0.92 billion, growing from 2025 value of USD 0.80 billion with 2031 projections showing USD 1.87 billion, growing at 15.19% CAGR over 2026-2031.

This report is Segmented by Application (Cardiovascular Diseases, Obesity, and Other Applications), Product (Diagnostic Kits and Reagents, and Nutrition {Vitamins & Minerals, and More}), End-User (Hospitals & Clinics, Research Institutes, and More), Distribution Channel (Direct To Consumer, and More), and Geography (North America, Europe, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Nutrigenomics Market Trends and Insights

Growing Burden of Lifestyle-Related Chronic Diseases

Diet-linked illnesses now command most healthcare budgets, prompting payers to explore prevention. The NIH allocated USD 156 million to a precision-nutrition study covering 10,000 participants to map gene-microbiome interactions. Early findings show FADS1 variants alter omega-3 response, supporting targeted supplementation. Health systems increasingly position the Nutrigenomics market as a scalable tool for delaying diabetes onset in pre-diabetic groups. Employers finance genetic-guided meal plans to reduce absenteeism, while insurers pilot premium discounts tied to personalized nutrition adherence. These initiatives elevate demand for clinically validated platforms that translate gene data into actionable diet protocols.

Declining Costs of Next-Generation Sequencing Technologies

Whole-genome sequencing fell from USD 10,000 to USD 600 within a decade, and industry roadmaps forecast sub-USD 100 tests before 2030. Third-generation instruments yield longer reads and minimize amplification bias, increasing accuracy for genes governing methylation, lipid uptake, and caffeine metabolism. Lower barriers let vendors bundle broad polygenic risk scores into subscription services, expanding the Nutrigenomics market's addressable base beyond fitness enthusiasts to mainstream wellness consumers. Seamless integration with continuous glucose monitors and microbiome assays further differentiates offerings.

Lack Of Harmonized Global Regulatory Framework

Divergent rules force companies to navigate multiple classifications. The FDA requires new dietary ingredient notifications, whereas the EU treats comparable products under food supplement codes. China layers functional-food and health-food dossiers, adding cost and time. Absence of mutual recognition triggers redundant trials, inflating R&D expenses that smaller entrants struggle to absorb. Compliance complexities can delay launches by 18-24 months, trimming the Nutrigenomics market's near-term revenue potential but also rewarding early movers investing in robust governance systems.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Consumer Awareness of Gene-Diet Interactions

- Proliferation Of Digital Health Platforms Integrating Nutrigenomic Data

- Limited Clinical Utility Evidence Supporting Nutrigenomic Recommendations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Obesity applications accounted for 35.10% of the nutrigenomics market share in 2025 as employers sought personalized diet programs to curb healthcare premiums. The segment's sheer volume ensured that the Nutrigenomics market size for weight-management services surpassed USD 0.28 billion in 2025. Precision oncology, though smaller, is expanding at 12.55% CAGR because polygenic risk scores improve tumor-nutrient pathway targeting. Cardiovascular and metabolic disorder portfolios ride on well-validated lipid-gene correlations, while neurological research explores gut-brain mechanisms linking genotype to neurotransmitter synthesis.

Research momentum is moving from single-condition panels toward integrated tests covering obesity, cardiometabolic, and oncologic risks simultaneously. This cross-condition architecture boosts customer lifetime value by offering one report that informs multiple interventions. Evidence from CAPFISH-3 supporting gene-guided omega-3 regimens accelerates oncology-focused adoption among clinicians wary of anecdotal data. As clinical guidelines evolve, application diversification is poised to fortify overall Nutrigenomics market resilience against reimbursement shocks.

Vitamins and minerals led with 30.85% revenue share in 2025, owing to established consumer trust and streamlined regulatory pathways. Segment revenue equated to 38% of the Nutrigenomics market size for finished products. Probiotics and prebiotics capture growth at 12.18% CAGR as metagenomic studies validate gene-microbiome synergies. Protein and amino acid formulations benefit from active-aging trends, whereas phytochemicals gain attention for epigenetic modulation potential.

Product innovation is tilting toward multi-compound blends that address clusters of genetic variants instead of one-nutrient solutions. DSM-Firmenich's Humiome line, which pairs probiotics with postbiotics, exemplifies the shift toward gut-centric personalization. AI formulation engines now optimize micronutrient ratios to match individual polymorphism profiles, creating bespoke supplement schemes shipped monthly. These developments broaden differentiation levels within the Nutrigenomics industry while raising expectations for scientific substantiation.

Geography Analysis

North America contributed 39.10% of 2025 revenue, anchored by clear FDA guidance and high discretionary income. United States operators such as 23andMe leverage a robust telehealth infrastructure to bundle genetic tests with GLP-1 weight-loss memberships, reinforcing recurring revenue loops. Canada emphasizes clinical-grade evidence, nudging vendors toward physician-partnered delivery models, while Mexico's expanding middle class fuels cross-border D2C kit imports.

Asia Pacific recorded the fastest CAGR at 13.42%. China's Healthy China 2030 blueprint funds precision nutrition pilots, and local giants use super-app ecosystems to push gene-driven meal kits at scale. India faces heterogeneous regulations yet shows strong practitioner interest, with nearly all surveyed dietitians keen to integrate genomic insights. Japan leverages its functional-food heritage to market genotype-specific fermented products, whereas South Korea's anti-diabetes campaigns embrace gene-guided menu platforms. Despite regulatory patchwork, regional smartphone penetration and cultural openness to preventive health underpin sustained momentum for the Nutrigenomics market.

Europe presents a mature but meticulous environment. GDPR mandates data-governance thresholds, rewarding firms with transparent consent architectures. Germany and the United Kingdom lead uptake inside clinical settings, whereas Mediterranean countries leverage traditional diet research to contextualize gene advice. Mutual recognition across EU states simplifies product passporting, yet country-specific labeling nuances compel modular packaging strategies. The bloc's insistence on randomized trials prolongs time-to-market but yields high consumer trust once approvals are obtained.

- DSM

- BASF

- Danone

- Nestle

- Unilever

- 23andMe

- Viome

- Metagenics

- Genova Diagnostics

- Nutrigenomix

- GX Sciences

- Xcode Life

- Cell-Logic

- DayTwo

- Prenetics

- Persona Nutrition

- Herbalife Nutrition

- Amway

- Perrigo Company

- CuraLife

- GeneSmart

- Holistic Heal

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden of Lifestyle-Related Chronic Diseases

- 4.2.2 Declining Costs of Next-Generation Sequencing Technologies

- 4.2.3 Expanding Consumer Awareness of Gene-Diet Interactions

- 4.2.4 Proliferation of Digital Health Platforms Integrating Nutrigenomic Data

- 4.2.5 Strategic Alliances Between Nutraceutical, Biotech, And Big-Data Companies

- 4.2.6 Employer And Insurer Adoption of Preventive Nutrition Genomics Programs

- 4.3 Market Restraints

- 4.3.1 Lack of Harmonized Global Regulatory Framework

- 4.3.2 Limited Clinical Utility Evidence Supporting Nutrigenomic Recommendations

- 4.3.3 Rising Data-Privacy and Cybersecurity Concerns Around Genomic Databases

- 4.3.4 Low Physician Awareness and Education in Nutrigenomics Principles

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Cardiovascular Diseases

- 5.1.2 Obesity

- 5.1.3 Cancer Research

- 5.1.4 Metabolic Disorders

- 5.1.5 Neurological Disorders

- 5.1.6 Other Applications

- 5.2 By Product

- 5.2.1 Diagnostic Kits and Reagents

- 5.2.2 Nutrition

- 5.2.2.1 Vitamins & Minerals

- 5.2.2.2 Probiotics & Prebiotics

- 5.2.2.3 Proteins & Amino Acids

- 5.2.2.4 Phytochemicals

- 5.2.2.5 Others

- 5.3 By End-User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Research Institutes & Universities

- 5.3.3 Direct-to-Consumer Companies

- 5.3.4 Pharmaceutical & Biotech Firms

- 5.3.5 Nutrition & Fitness Centers

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Online Platforms

- 5.4.3 Retail Pharmacies

- 5.4.4 Healthcare-Practitioner Sales

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products, and Recent Developments)

- 6.3.1 DSM

- 6.3.2 BASF SE

- 6.3.3 Danone

- 6.3.4 Nestle Health Science

- 6.3.5 Unilever Group

- 6.3.6 23andMe

- 6.3.7 Viome

- 6.3.8 Metagenics Inc.

- 6.3.9 Genova Diagnostics

- 6.3.10 Nutrigenomix Inc.

- 6.3.11 GX Sciences Inc.

- 6.3.12 Xcode Life

- 6.3.13 Cell-Logic

- 6.3.14 DayTwo

- 6.3.15 Prenetics

- 6.3.16 Persona Nutrition

- 6.3.17 Herbalife Nutrition

- 6.3.18 Amway Corporation

- 6.3.19 Perrigo Company

- 6.3.20 CuraLife

- 6.3.21 GeneSmart

- 6.3.22 Holistic Heal

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment