PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062229

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062229

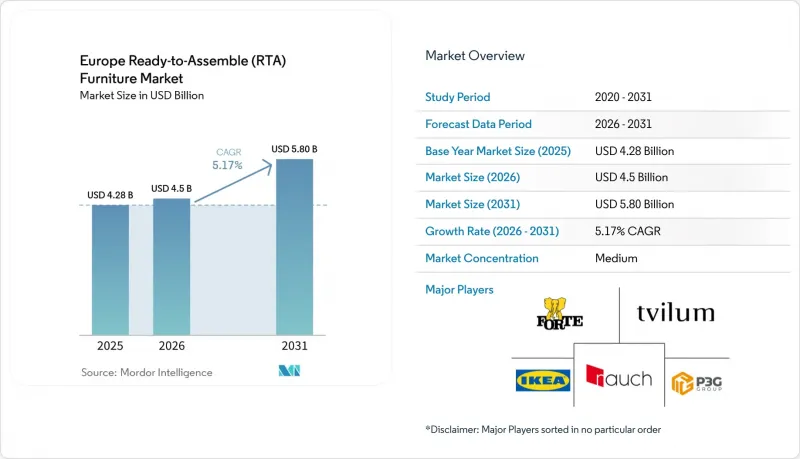

Europe Ready-to-Assemble (RTA) Furniture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe ready-to-Assemble (RTA) furniture market size is expected to increase from USD 4.28 billion in 2025 to USD 4.50 billion in 2026 and reach USD 5.8 billion by 2031, growing at a CAGR of 5.17% over 2026-2031.

This report is Segmented by Product Type (Home Furniture, Office Furniture, Hospitality, Educational, and More), Material (Wood, Metal, Plastic, and More), Distribution Channel (B2C/Retail and B2B / Directly From the Manufacturers), and Geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

Europe Ready-to-Assemble (RTA) Furniture Market Trends and Insights

E-commerce Scaling and Omnichannel Logistics Lower CAC and Last-Mile Costs for Flat-Pack SKUs

The Europe ready-to-assemble furniture market benefits directly from rising digital penetration and improved online conversion driven by richer content and checkout experiences. Leading retailers report growing online engagement alongside stable store footfall, indicating that smaller-format stores, click-and-collect, and parcel-friendly flat-pack SKUs are reinforcing reach without imposing heavy delivery surcharges. The 2025 trading year saw online visits rise, while the online share approached one-third of sales for one of the largest banners, affirming the fit between compact RTA parcels and urban distribution networks. Players like IKEA, with their flat-pack product design, are capitalizing on the surge in online sales of RTA furniture. The compact, modular design of RTA furniture not only fits seamlessly into urban logistics networks but also boosts online sales and simplifies last-mile delivery in crowded urban areas.Rich visualization and augmented-reality workflows are also becoming mainstream as furniture sellers standardize 3D assets and mobile-first pathways, which reduces returns and assembly disputes while enabling confident purchases of higher-ticket flat-pack items. Together, these factors compress cost to serve and reduce customer acquisition cost for the Europe-ready-to-assemble furniture market, as repeatability in the last mile and returns enable scale.

Hybrid Work Sustains Home-Office RTA Demand (Desks, Storage, Ergonomic Add-Ons)

Hybrid work patterns keep a consistent floor of demand for compliant desks, storage, and ergonomic seating, which supports premium RTA configurations priced well above entry-level kits. Within the European ready-to-assemble furniture market, many of these purchases are planned replacements funded by remote work allowances or self-directed investment by professionals who now value ergonomic continuity at home. Demand is also supported by the steady refinement of smart adjustability and cable management, which increasingly comes pre-engineered into mid-range products. Several European suppliers have showcased upgraded mechanisms and digital integration features in the 2025 and 2026 cycles, signaling a broadening of smart benefits into flat-pack. This dynamic is reflected in sustained mid-to-high single-digit growth forecasts for office-oriented lines inside the overall RTA mix through 2031. As a result, the Europe ready-to-assemble furniture market continues to see above-baseline growth in the home-office segment as households finalize permanent workspace setups.

Consumer Pain Points in Assembly and Returns for Complex SKUs

Complex wardrobes, drawer banks, and multi-panel systems can lead to assembly errors and extended installation time, which increases support tickets and the odds of returns. Tool-free mechanisms and improved hinge geometries are being introduced to reduce the reliance on large hardware kits and to simplify alignment in tight spaces. Several 2026 cabinet innovations now target wider opening angles and rotating access to minimize mis-assembly while preserving storage volume. These changes are designed to reduce returns due to missing parts, unclear instructions, or misapplied hardware, and to support reassembly when households relocate. As brands add QR-coded parts catalogs and clearer guidance, they also set the stage for circular take-back and refurbishment services that depend on fast, reliable disassembly. These steps ease friction for the Europe-ready-to-assemble furniture market by lowering service burden and lifting first-time-right outcomes.

Other drivers and restraints analyzed in the detailed report include:

- DIY/Organised Specialist and DIY Retail Push (Private Label Breadth, Price Points)

- EU Circularity Preferences Favor Easy-to-Disassemble, Repairable Designs

- Aggressive Price Investments by Large-Format Retailers Intensify Margin Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Home furniture accounted for 67.85% of 2025 revenue as households completed deferred upgrades and compact-living improvements, while office furniture is forecast to expand at a 6.55% CAGR through 2031 in step with normalized hybrid schedules and sustained ergonomic investment. The Europe-ready-to-assemble furniture market continues to see replacement cycles migrate into 2024 and 2025, with consumers prioritizing functional refreshes that fit smaller footprints and multipurpose use. Within home furniture, modular tables, storage, and beds carry volume, while wardrobes and kitchen fixtures drive value through thicker boards, improved finishes, and better hardware. The Europe-ready-to-assemble furniture market for office-oriented categories is projected to grow more rapidly, as remote professionals invest in compliance-grade chairs and desks to formalize workspace ergonomics. Height presets, cable management, and smarter adjustment are becoming standard in the mid-range, which raises willingness to pay and supports premium cadence in the category. Brands that streamline assembly for these feature-rich products tend to reduce returns and protect margins as they add weight and complexity to higher-tier kits.

The Europe-ready-to-assemble furniture market leverages broad home demand, while office subcategories benefit from durable hybrid behavior. Chairs, desks, and storage that meet recognized ergonomics standards are spreading into price bands reachable by self-funded home offices, which increases the mix value. For home categories, modular units, reconfigurable shelves, and lighting-integrated panels reinforce appeal in small apartments where rooms play multiple roles over a week. Hospitality refresh cycles are also oriented toward modularity and circular take-back, a pattern that supports predictable quality and higher specification consistency over longer contract horizons. Educational and healthcare applications remain smaller within RTA but continue to require durable, wipeable surfaces and safe edges at accessible price points, which depend on efficient flat-pack engineering.

List of Companies Covered in this Report:

- IKEA

- Tvilum A/S

- Fabryki Mebli FORTE S.A.

- Black Red White (BRW)

- Szynaka Meble

- Rauch Mobelwerke GmbH

- Parisot Industrie (P3G Group)

- Demeyere Group (CBA Meubles)

- Alsapan

- Dorel Home (Dorel Industries)

- Nobilia Werke

- Howdens Joinery

- Nobia (incl. Magnet, Gower)

- Keter Group

- VOX (VOX Capital Group)

- Alples d.d.

- Schmidt Groupe

- UAB Freda

- Hulsta-Werke

- Meble Wojcik

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce scaling and omnichannel logistics lower CAC and last-mile costs for flat-pack SKUs

- 4.2.2 Shrinking urban living spaces increase demand for modular, space-saving RTA formats

- 4.2.3 Hybrid work sustains home-office RTA demand (desks, storage, ergonomic add-ons)

- 4.2.4 DIY/organised specialist & DIY retail push (private label breadth, price points)

- 4.2.5 EU circularity preferences favor easy-to-disassemble, repairable designs

- 4.2.6 Nearshored CEE supply clusters (PL/LT/RO) improve lead times and resilience

- 4.3 Market Restraints

- 4.3.1 Tight timber supply and compliance (EUTR/EUDR) raise input and audit costs

- 4.3.2 Consumer pain points in assembly/returns for complex SKUs

- 4.3.3 Aggressive price investments by IKEA intensify margin pressure across Europe

- 4.3.4 Western Europe demand softness and concentration risk in Germany for exporters

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Home Furniture

- 5.1.1.1 Chairs

- 5.1.1.2 Tables (side, coffee, dressing, etc.)

- 5.1.1.3 Beds

- 5.1.1.4 Wardrobes

- 5.1.1.5 Sofas

- 5.1.1.6 Dining Tables / Dining Sets

- 5.1.1.7 Kitchen Cabinets

- 5.1.1.8 Other Home Furniture

- 5.1.2 Office Furniture

- 5.1.2.1 Chairs

- 5.1.2.2 Tables

- 5.1.2.3 Storage Cabinets

- 5.1.2.4 Desks

- 5.1.2.5 Sofas & Other Soft Seating

- 5.1.2.6 Other Office Furniture

- 5.1.3 Hospitality Furniture

- 5.1.4 Educational Furniture

- 5.1.5 Healthcare Furniture

- 5.1.6 Other Applications (public places, retail malls, government offices, etc.)

- 5.1.1 Home Furniture

- 5.2 By Material

- 5.2.1 Wood

- 5.2.2 Metal

- 5.2.3 Plastic

- 5.2.4 Glass

- 5.2.5 Other Materials

- 5.3 By Distribution Channel

- 5.3.1 B2C / Retail

- 5.3.1.1 Home Centers

- 5.3.1.2 Specialty Furniture Stores

- 5.3.1.3 Online

- 5.3.1.4 Other Distribution Channels

- 5.3.2 B2B / Directly from the Manufacturers

- 5.3.1 B2C / Retail

- 5.4 By Geography

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Spain

- 5.4.5 Italy

- 5.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 IKEA

- 6.4.2 Tvilum A/S

- 6.4.3 Fabryki Mebli FORTE S.A.

- 6.4.4 Black Red White (BRW)

- 6.4.5 Szynaka Meble

- 6.4.6 Rauch Mobelwerke GmbH

- 6.4.7 Parisot Industrie (P3G Group)

- 6.4.8 Demeyere Group (CBA Meubles)

- 6.4.9 Alsapan

- 6.4.10 Dorel Home (Dorel Industries)

- 6.4.11 Nobilia Werke

- 6.4.12 Howdens Joinery

- 6.4.13 Nobia (incl. Magnet, Gower)

- 6.4.14 Keter Group

- 6.4.15 VOX (VOX Capital Group)

- 6.4.16 Alples d.d.

- 6.4.17 Schmidt Groupe

- 6.4.18 UAB Freda

- 6.4.19 Hulsta-Werke

- 6.4.20 Meble Wojcik

7 Market Opportunities & Future Outlook

- 7.1 Tool-free, DPP-ready ranges for faster returns processing and recommerce

- 7.2 Hospitality refresh cycles with circular fit-outs (modular, repairable SKUs)