PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061692

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061692

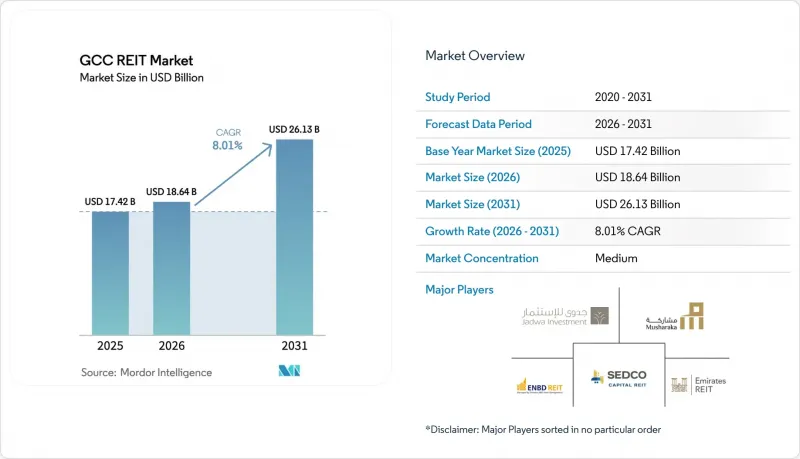

GCC REIT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the gCC rEIT market size was valued at USD 17.42 billion in 2025 and is estimated to grow from USD 18.64 billion in 2026 to reach USD 26.13 billion by 2031, at a CAGR of 8.01% during the forecast period (2026-2031).

This report is Segmented by Sector of Exposure (Retail, Industrial & Logistics, Office, Residential, Diversified, Data Centres, Healthcare, Other Sectors), Bymarket Capitalization (Large-Cap, Mid-Cap, Small-Cap), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, Oman). The Market Forecasts are Provided in Terms of Value (USD).

GCC REIT Market Trends and Insights

Rising Appetite of GCC Sovereign Wealth Funds for Domestic Real-Estate Income Streams

Major Gulf sovereign vehicles have pivoted from overseas trophy assets to domestic yield assets, anchoring several flagship trusts and improving market depth. The Public Investment Fund's 2024 decision to seed a Saudi residential REIT and Abu Dhabi Investment Authority's co-investment in regional logistics portfolios exemplify this repositioning. Warehouse occupancy in Riyadh hit 98% in H1 2025, and rents climbed 16% year-on-year, prompting sovereign sponsors to crystallize gains through listed units. A compulsory 90% income distribution aligns these vehicles with pension and insurance liabilities, providing a predictable cash flow. Domestic redeployment also hedges against Western regulatory scrutiny of Gulf capital, reducing ex-territorial risk. Collectively, these factors reinforce sustained inflows into the GCC REIT market.

Eased Foreign-Ownership Limits in Saudi Arabia and UAE

Regulatory liberalization has carved out attractive channels for external investors. Saudi Arabia now levies a 10% transaction fee on foreigners buying property directly but exempts acquisitions via listed trusts, steering overseas capital into the GCC REIT market. Parallel reforms in Dubai permit leverage up to 50% of gross asset value, enhancing return potential without breaching prudential norms. These measures converge as global allocators seek yield alternatives to softened European offices, positioning Gulf trusts as a compelling blend of growth and dividend income. Early evidence shows passive fund-tracker money increasing allocation weightings after the rule change.

Thin Free-Float and Low Daily Liquidity of Most GCC REITs

Many vehicles still have founding stakes exceeding 60%, keeping daily turnover under USD 2 million and inflating bid-ask spreads. Illiquidity discourages large institutions that need exit pathways, forcing block trades off-exchange and dulling price signals. Kuwait's retail-oriented fund trades sporadically despite a solid dividend track record, revealing the structural hurdle in smaller markets. Absence of mandatory market-making exacerbates the issue during stress events. Until older trusts widen public floats, passive inflows into the GCC REIT market will remain concentrated in a few names.

Other drivers and restraints analyzed in the detailed report include:

- Launch of REIT-Focused Indices on Tadawul and DFM Driving Passive Inflows

- Accelerated Government Privatization of Public Real-Estate Portfolios

- Rising Benchmark Rates Widening Valuation Yield Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Office assets captured 38.5% of GCC REIT market share in 2025, reflecting legacy holdings in Dubai's Business Bay and Riyadh's King Abdullah Financial District. Yet data-center portfolios are forecast to register a 9.11% CAGR through 2031, the quickest pace in the GCC REIT market. Knight Frank logged 98% warehouse occupancy in Riyadh alongside 16% rent growth during H1 2025, igniting sponsor interest in logistics conversions. Super-regional malls remain 95% let but are remixing tenants toward entertainment, driving 12-15% annual rent hikes in prime Dubai locations. Residential trusts are embryonic; Dubai's USD 5.89 billion vehicle launched in 2025 signals a pivot to multifamily securitization. Healthcare and student-housing assets represent untapped lanes as privatization gathers pace.

The GCC REIT market size for office holdings delivered a stable yield in 2025, but yield compression is likely as refinancing costs climb. Conversely, the GCC REIT market size tied to data-center facilities enjoys structured escalators aligned with power-cost pass-throughs, buffering margins. Diversified funds use hospitality and retail to cushion swings, yet specialty vehicles often trade at premium valuations due to scarcity. Investor surveys confirm growing preference for single-theme strategies that can articulate clear operational KPIs such as megawatt utilization or cold-storage throughput.

List of Companies Covered in this Report:

- Jadwa REIT Saudi Fund

- Musharaka REIT

- Sedco Capital REIT

- Emirates REIT (CEIC)

- ENBD REIT

- AlAhli REIT Fund (I)

- Alinma Retail REIT

- Derayah REIT

- Al Ma'athar REIT

- Bonyan REIT

- Al-Khabeer REIT

- Riyad REIT

- Al Rajhi REIT

- Kamco Invest REIT

- Ezdan REIT

- Qatar First Bank REIT

- Manazil REIT

- Tanmia REIT Fund

- Al Salam REIT Bahrain

- SICO Kingdom REIT

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising appetite of GCC sovereign wealth funds for domestic real-estate income streams

- 4.2.2 Eased foreign-ownership limits in Saudi Arabia and UAE

- 4.2.3 Launch of REIT-focused indices on Tadawul and DFM driving passive inflows

- 4.2.4 Accelerated government privatisation of public real-estate portfolios

- 4.2.5 Giga-project pipelines (NEOM, The Line, Lusail etc.) creating institutional-grade inventory

- 4.2.6 Specialised digital-infrastructure & logistics assets fuelling new REIT structures

- 4.3 Market Restraints

- 4.3.1 Thin free-float and low daily liquidity of most GCC REITs

- 4.3.2 Rising benchmark rates widening valuation yield gaps

- 4.3.3 NAV uncertainty from IFRS-16 lease-accounting adoption

- 4.3.4 High inter-emirate and cross-border transaction costs limiting diversification

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Investors

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD billion)

- 5.1 By Sector of Exposure

- 5.1.1 Retail

- 5.1.2 Industrial & Logistics

- 5.1.3 Office

- 5.1.4 Residential

- 5.1.5 Diversified

- 5.1.6 Data Centres

- 5.1.7 Healthcare

- 5.1.8 Other Sectors

- 5.2 By Market Capitalisation

- 5.2.1 Large-Cap

- 5.2.2 Mid-Cap

- 5.2.3 Small-Cap

- 5.3 By Geography

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 Qatar

- 5.3.4 Kuwait

- 5.3.5 Bahrain

- 5.3.6 Oman

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Jadwa REIT Saudi Fund

- 6.4.2 Musharaka REIT

- 6.4.3 Sedco Capital REIT

- 6.4.4 Emirates REIT (CEIC)

- 6.4.5 ENBD REIT

- 6.4.6 AlAhli REIT Fund (I)

- 6.4.7 Alinma Retail REIT

- 6.4.8 Derayah REIT

- 6.4.9 Al Ma'athar REIT

- 6.4.10 Bonyan REIT

- 6.4.11 Al-Khabeer REIT

- 6.4.12 Riyad REIT

- 6.4.13 Al Rajhi REIT

- 6.4.14 Kamco Invest REIT

- 6.4.15 Ezdan REIT

- 6.4.16 Qatar First Bank REIT

- 6.4.17 Manazil REIT

- 6.4.18 Tanmia REIT Fund

- 6.4.19 Al Salam REIT Bahrain

- 6.4.20 SICO Kingdom REIT

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment