PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061719

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061719

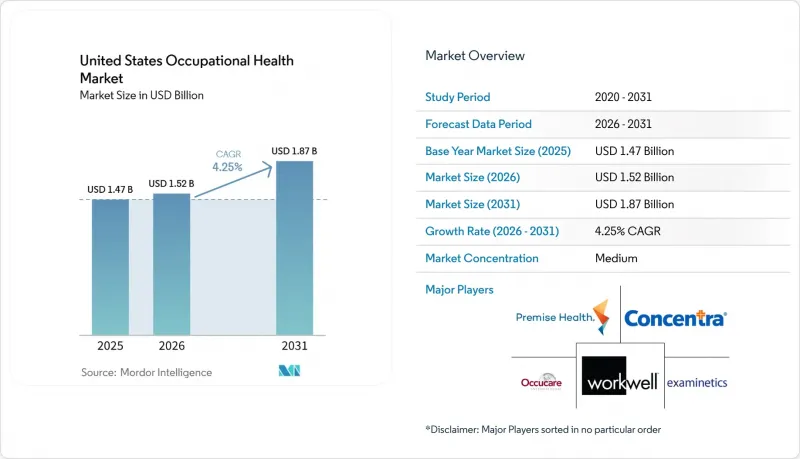

United States Occupational Health - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states occupational health market size was valued at USD 1.47 billion in 2025 and is estimated to grow from USD 1.52 billion in 2026 to reach USD 1.87 billion by 2031, at a CAGR of 4.25% during the forecast period (2026-2031).

This report is Segmented by Service Type (Pre-Employment & Post-Offer Exams, Drug & Alcohol Screening, and More), Health Condition (Work-Induced Stress, Respiratory Diseases, and More), Delivery Setting (On-Site Employer Clinics, and More), End-User Industry (Manufacturing, Construction & Mining and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Occupational Health Market Trends and Insights

Expanding Employer-Sponsored Wellness Benefits

Organizations increasingly view wellness programs as retention tools. A 2024 study reported 12% lower voluntary turnover among companies that bundled biometric screenings, health coaching, and mental-health resources versus peers without such offerings.Provider networks now package preventive screenings with nutrition counseling and stress-management workshops, positioning themselves as population-health partners and offsetting flat workers' compensation premiums in low-risk sectors.

Growth of Remote/Hybrid Workforce Demanding Tele-OccMed Services

Hybrid work dismantles the traditional clinic-centric delivery model. Remote employees can complete fitness-for-duty evaluations by video, submit at-home specimens, and undergo virtual audiometry, accelerating onboarding across multiple states. A 2024 systematic review showed 94% diagnostic concordance between tele-evaluations and in-person visits for non-physical roles. Established clinic operators are therefore acquiring telehealth platforms to protect share within the occupational health market.

Shortage of Board-Certified Occupational Physicians

Fewer than 3,000 certified practitioners are active nationwide, limiting service scope in rural clinics. Operators rely more on nurse practitioners and physician assistants, and expansion slows in underserved regions of the occupational health market.

Other drivers and restraints analyzed in the detailed report include:

- Tight U.S. Labor Market Boosting Pre-Employment Screenings

- Rise in OSHA Citations Prompting Proactive Compliance Programs

- Employer Data-Privacy Concerns Over Continuous Health Monitoring

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pre-Employment & Post-Offer Exams retained a 32.46% occupational health market share in 2025, but growth moderates as automation trims headcount in heavy industry. In contrast, Employee Assistance & Mental-Health Programs grow at a 7.25% CAGR, because burnout-driven absenteeism surpasses injury claims in many white-collar groups. Drug & Alcohol Screening remains a compliance pillar, yet margins tighten with cheaper oral-fluid kits. Rehabilitation services stay stable, aided by insurers that favor early intervention. Ergonomic consulting expands in large warehouses where proactive assessments cut upper-extremity injuries by 23% over two years.

Employers now seek bundled packages instead of individual engagements, forcing providers to diversify offerings or partner with wellness vendors. The occupational health market size for mental-health services is expected to represent an increasing slice of overall revenue by 2031. Tele-based counseling compresses delivery costs and increases session uptake, helping programs reach smaller employers that previously lacked access. Structural growth remains tied to continued recognition of psychosocial hazards as core business costs.

Work-Induced Stress captured 27.57% of the occupational health market size in 2025 and leads growth at 8.05% CAGR, reflecting high turnover and disability costs stemming from anxiety and depression. Musculoskeletal Disorders rank second but their share erodes as lift-assist devices spread on factory floors. Respiratory Disease incidence eases due to improved ventilation systems, yet remains a focus in chemical plants. Heat-stress visits rise 18% in Sun Belt emergency rooms, a trend likely to accelerate under OSHA's new standard.

Providers are expanding behavioral-health capacity and investing in on-staff counselors. Digital tools now triage stress claims before they escalate into leave requests. At the same time, clinics are integrating ergonomic therapy and return-to-work coaching to address cumulative trauma. These service shifts fortify growth prospects inside the broader occupational health market.

List of Companies Covered in this Report:

- AllOne Health Resources

- Axiom Medical

- BioIQ

- Concentra

- Conserve Health

- CorVel Corporation

- Examinetics

- Harness Health Partners

- Intermountain WorkMed

- MediTrax

- Mobile Health

- National Vision Administrators (OccMed division)

- Nova Medical Centers

- OccuSystems

- Praxis Occupational Medicine

- Premise Health

- Total Safety

- U.S. HealthWorks

- WorkCare

- Workplace Safety & Prevention Services

- WorkWell Occupational Medicine

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Employer-Sponsored Wellness Benefits

- 4.2.2 Growth Of Remote / Hybrid Workforce Demanding Tele-Occmed Services

- 4.2.3 Tight U.S. Labor Market Boosting Pre-Employment Screenings

- 4.2.4 Rise In OSHA Citations Prompting Proactive Compliance Programs

- 4.2.5 AI-Enabled Risk-Prediction Reducing Injury Costs

- 4.2.6 Climate-Related Heat-Stress Prevention Services

- 4.3 Market Restraints

- 4.3.1 Automation Reducing Head-Count In Heavy Industry

- 4.3.2 Shrinking Workers? Comp Premiums In Low-Risk Sectors

- 4.3.3 Shortage Of Board-Certified Occupational Physicians

- 4.3.4 Employer Data-Privacy Concerns Over Continuous Health Monitoring

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Service Type

- 5.1.1 Pre-Employment & Post-Offer Exams

- 5.1.2 Drug & Alcohol Screening

- 5.1.3 Immunizations & Travel Medicine

- 5.1.4 Employee Assistance & Mental-Health Programs

- 5.1.5 Rehabilitation & Return-to-Work Services

- 5.1.6 Ergonomic & On-Site Safety Services

- 5.2 By Health Condition

- 5.2.1 Work-Induced Stress

- 5.2.2 Respiratory Diseases

- 5.2.3 Noise-Induced Hearing Loss

- 5.2.4 Chemical & Vibration-Related Disorders

- 5.2.5 Musculoskeletal Disorders

- 5.2.6 Others

- 5.3 By Delivery Setting

- 5.3.1 On-Site Employer Clinics

- 5.3.2 Off-Site Clinics / Stand-Alone Centers

- 5.3.3 Mobile Occupational Health Units

- 5.3.4 Tele-Occupational Health Platforms

- 5.4 By End-User Industry

- 5.4.1 Manufacturing

- 5.4.2 Construction & Mining

- 5.4.3 Healthcare & Social Assistance

- 5.4.4 Government & Public Sector

- 5.4.5 Transportation & Warehousing

- 5.4.6 IT, Finance & Professional Services

- 5.4.7 Retail & Hospitality

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 AllOne Health Resources

- 6.3.2 Axiom Medical

- 6.3.3 BioIQ

- 6.3.4 Concentra

- 6.3.5 Conserve Health

- 6.3.6 CorVel Corporation

- 6.3.7 Examinetics

- 6.3.8 Harness Health Partners

- 6.3.9 Intermountain WorkMed

- 6.3.10 MediTrax

- 6.3.11 Mobile Health

- 6.3.12 National Vision Administrators (OccMed division)

- 6.3.13 Nova Medical Centers

- 6.3.14 OccuSystems

- 6.3.15 Praxis Occupational Medicine

- 6.3.16 Premise Health

- 6.3.17 Total Safety

- 6.3.18 U.S. HealthWorks

- 6.3.19 WorkCare, Inc.

- 6.3.20 Workplace Safety & Prevention Services

- 6.3.21 WorkWell Occupational Medicine

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment