PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061735

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061735

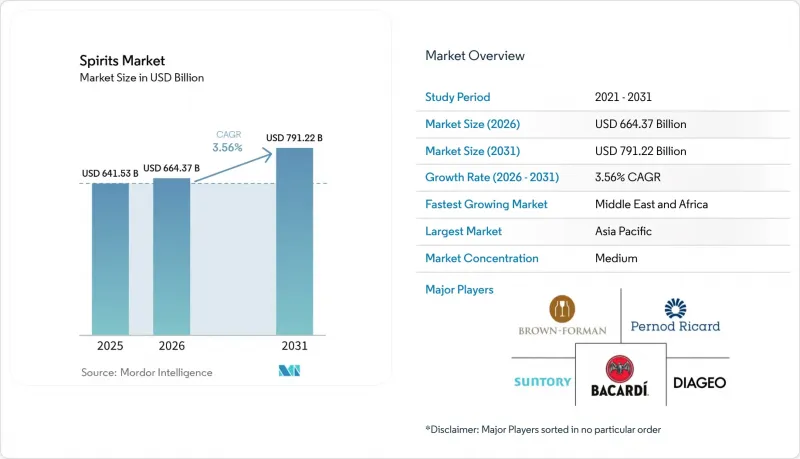

Spirits - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the spirits market was valued at USD 641.53 billion in 2025 and estimated to grow from USD 664.37 billion in 2026 to reach USD 791.22 billion by 2031, at a CAGR of 3.56% during the forecast period (2026-2031).

This report is Segmented by Product Type (Brandy and Cognac, Liqueur, Rum, Tequila and Mezcal, Whiskies, White Spirits, Other Spirit Types), End User (Men and Women), Distribution Channel (On-Trade and Off-Trade), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Spirits Market Trends and Insights

Increasing consumer preference for craft and small-batch spirits

Craft spirits are increasingly capturing consumer interest, driving strong momentum in the global spirits market. This segment is flourishing as demand grows for unique, high-quality beverages with authentic character. Artisanal distilleries, from FEW Spirits in the United States to Sipsmith in the United Kingdom, are gaining popularity with their distinctive flavor profiles across gin, whiskey, vodka, and other categories. By highlighting locally sourced botanicals, heirloom grains, and sustainable production practices, these producers are enhancing the appeal and perceived value of their craft offerings. Highlighting this trend, the American Craft Spirits Association reported a notable 11.5% uptick in active craft distillers in the United States bringing the total to 3,069 in 2023. Developed markets, especially the United States, Germany, and the United Kingdom are witnessing this craft fervor, bolstered by rising disposable incomes that encourage a dive into niche, high-quality spirits. Rising consumer demand for transparency in production methods and authentic brand stories is further reinforcing the appeal of craft spirits. Collaborations between craft distilleries and local businesses are also driving innovation and broadening market exposure. As more consumers shift toward artisanal offerings, both retail shelves and bar menus are experiencing a significant shift, increasingly favoring craft labels over mass-produced alternatives.

Expansion of the tourism and hospitality sector contributing to strong market growth

A burgeoning tourism and hospitality sector is propelling the spirits market. The World Tourism Organization (UNWTO) reported a significant milestone in 2024, with global international tourist arrivals hitting 1.4 billion, underscoring a vigorous rebound in global travel. This resurgence has fueled rising demand for premium and locally crafted spirits, as tourists increasingly seek authentic cultural experiences often expressed through tasting regional specialties such as tequila in Mexico, Scotch in Scotland, or sake in Japan. To capitalize on this trend, governments around the world are investing strategically in tourism development. For example, the Indian government allocated INR 1,900 crore in its 2024-25 Union Budget to strengthen tourism infrastructure and attract both domestic and international visitors. Meanwhile, the United States Travel Association announced that domestic travel expenditures reached USD 1.3 trillion in 2024, indicating a robust recovery in the hospitality sector. Such momentum is translating into heightened spirits consumption across hotels, restaurants, resorts, and bars, especially in sought-after tourist locales. With travel and experiential spending on the upswing, the hospitality industry's appetite for a diverse range of premium spirits is poised to drive the market's expansion. Additionally, the rise of culinary tourism and the growing trend of pairing spirits with local cuisines are further contributing to this demand. The increasing popularity of destination weddings and events is also creating new opportunities for the spirits market.

Tight government controls and compliance requirements

Stringent government regulations continue to pose substantial constraints on the spirits market, as many countries enforce high excise duties and import taxes that raise production costs and drive up retail prices. Nations like Norway and Sweden, which impose some of the world's highest alcohol taxes, often see spirits priced at more than twice the levels found in neighboring European markets. At the same time, strict advertising and marketing rules in key regions such as the European Union and the United States limit brand visibility and promotional flexibility. For instance, the United States Alcoholic Beverage Labeling Act requires health warnings on all packaging, while EU policies prohibit alcohol advertising during children's programming and restrict digital promotions that could appeal to minors. Regulatory complexity is even greater in markets like India, where state-specific rules including full prohibitions in Bihar and Gujarat create significant barriers for producers, and in Saudi Arabia, where alcohol is completely banned. Adding to these challenges is a rising global focus on health and wellness, intensifying scrutiny around alcohol consumption and further constraining market growth.

Other drivers and restraints analyzed in the detailed report include:

- Rising demand for high-end and premium alcoholic beverages

- Greater product differentiation based on raw ingredients and alcohol strength

- Increasing health concerns related to heavy alcohol intake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Whiskies held the largest share of the spirits market in 2025, accounting for 22.89% of total revenue. This strong position reflects the category's deep-rooted popularity among affluent consumers and collectors who value authenticity, craftsmanship, and aged expressions. Premium and super-premium whiskies continue to attract substantial interest due to their perceived exclusivity and investment potential. The segment also benefits from a thriving culture of tastings, limited-edition releases, and brand-led storytelling, all of which enhance consumer engagement. Continued innovation in cask finishes and regional expressions further broadens appeal across diverse demographics. As a result, whiskies remain a cornerstone of the global spirits market and a reliable driver of overall category value.

White spirits are projected to grow at a CAGR of 4.07% through 2031, making them the fastest-expanding product category in the spirits market. This momentum is underpinned by rising interest in versatile and mixable spirits such as vodka, gin, and white rum, which align well with the global cocktail culture. Younger consumers, in particular, are driving experimentation with new flavor profiles, botanical blends, and low-sugar formulations. The category is further boosted by the popularity of ready-to-drink (RTD) beverages, where white spirits often serve as the base. Increasing innovation in premium and craft offerings is also elevating the segment's perception and fueling demand.

Geography Analysis

In 2025, the Asia-Pacific region commands a significant 45.31% share of the global spirits market. This leadership is supported by the region's large population base, rising disposable incomes, and evolving drinking habits. In mature markets like Japan and South Korea, local spirits such as shochu and soju remain central to social traditions and daily consumption. Australia blends long-standing drinking culture with a rapidly expanding craft distillery movement, appealing especially to younger consumers seeking authenticity and locally crafted products. China continues to stand out with strong demand for both domestic offerings like Baijiu and international brands, driven by an emphasis on premiumization and gift-giving culture.

The Middle East and Africa (MEA) region is set for rapid expansion, with a projected CAGR of 5.09% between 2026 and 2031, though it begins from a smaller market base. South Africa leads the region, supported by major players like Diageo South Africa promoting high-end brands such as Johnnie Walker, Tanqueray, and Smirnoff. Growth is further fueled by the country's expanding middle class and their increasing preference for premium spirits. In the United Arab Emirates, a rising expatriate population and gradually shifting cultural attitudes are driving demand for luxury alcohol. Saudi Arabia is also seeing early signs of potential, with recent easing of alcohol rules for foreign visitors indicating new opportunities.

North America and Europe remain mature markets characterized by a strong inclination toward premium and craft spirits. The United States continues to lead in North America, with stable demand for whiskey, vodka, and tequila. This trend is reinforced by ongoing premiumization and the growth of craft distilling, with brands like Tito's Handmade Vodka and Buffalo Trace gaining prominence. In Europe, markets remain anchored by heritage-rich producers in Scotland, Ireland, and France, where globally recognized spirits such as Scotch whisky, Irish whiskey, and French cognac maintain strong international appeal supported by geographic indications.

- Diageo plc

- Pernod Ricard SA

- Bacardi Limited

- Suntory Holdings Limited

- Brown-Forman Corporation

- Remy Cointreau S.A.

- LVMH Moet Hennessy Louis Vuitton SE

- Davide Campari-Milano N.V.

- Constellation Brands Inc.

- William Grant & Sons Ltd

- Edrington Group Limited

- Sazerac Company, Inc.

- Kweichow Moutai Co, Ltd.

- Wuliangye Yibin Co. Ltd.

- Becle S.A.B. de C.V. (Jose Cuervo)

- Allied Blenders & Distillers Pvt Ltd

- John Distilleries Pvt Ltd

- Heaven Hill Distilleries, Inc.

- Mast-Jagermeister SE

- Asahi Group Holdings, Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing consumer preference for craft and small-batch spirits

- 4.2.2 Expansion of the tourism and hospitality sector contributing to strong market growth

- 4.2.3 Rising demand for high-end and premium alcoholic beverages

- 4.2.4 Greater product differentiation based on raw ingredients and alcohol strength

- 4.2.5 Expanding cocktail culture acting as a major driver of market demand

- 4.2.6 Ongoing innovation in flavors and packaging enhancing market growth

- 4.3 Market Restraints

- 4.3.1 Tight government controls and compliance requirements

- 4.3.2 Increasing health concerns related to heavy alcohol intake

- 4.3.3 Growing consumer move toward low- and zero-alcohol options

- 4.3.4 Awareness and advocacy campaigns discouraging alcohol consumption and slowing market growth

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Brandy and Cognac

- 5.1.2 Liqueur

- 5.1.3 Rum

- 5.1.4 Tequilla and Mezcel

- 5.1.5 Whiskies

- 5.1.6 White Spirits

- 5.1.7 Other Spirit Types

- 5.2 By End User

- 5.2.1 Men

- 5.2.2 Women

- 5.3 By Distribution Channel

- 5.3.1 On-Trade

- 5.3.2 Off-Trade

- 5.3.2.1 Specialty/Liquor Stores

- 5.3.2.2 Other Off Trade Channels

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Sweden

- 5.4.2.8 Belgium

- 5.4.2.9 Poland

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Indonesia

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Colombia

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 South Africa

- 5.4.5.3 Saudi Arabia

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Diageo plc

- 6.4.2 Pernod Ricard SA

- 6.4.3 Bacardi Limited

- 6.4.4 Suntory Holdings Limited

- 6.4.5 Brown-Forman Corporation

- 6.4.6 Remy Cointreau S.A.

- 6.4.7 LVMH Moet Hennessy Louis Vuitton SE

- 6.4.8 Davide Campari-Milano N.V.

- 6.4.9 Constellation Brands Inc.

- 6.4.10 William Grant & Sons Ltd

- 6.4.11 Edrington Group Limited

- 6.4.12 Sazerac Company, Inc.

- 6.4.13 Kweichow Moutai Co, Ltd.

- 6.4.14 Wuliangye Yibin Co. Ltd.

- 6.4.15 Becle S.A.B. de C.V. (Jose Cuervo)

- 6.4.16 Allied Blenders & Distillers Pvt Ltd

- 6.4.17 John Distilleries Pvt Ltd

- 6.4.18 Heaven Hill Distilleries, Inc.

- 6.4.19 Mast-Jagermeister SE

- 6.4.20 Asahi Group Holdings, Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK