PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072980

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072980

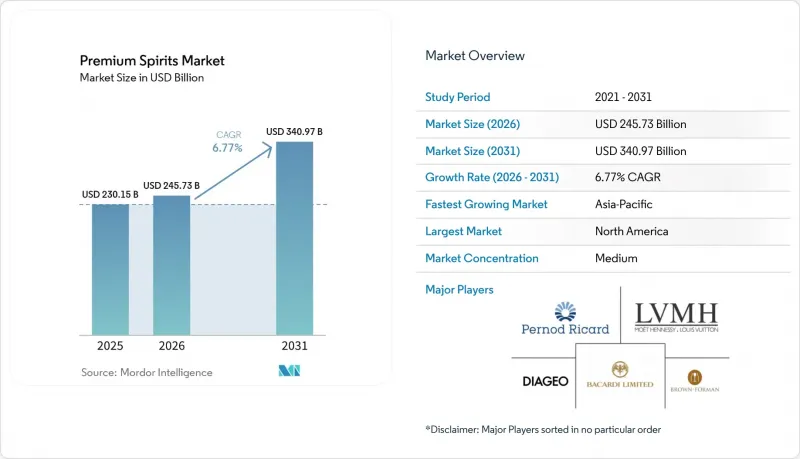

Premium Spirits - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the premium spirits market size is projected to expand from USD 230.2 billion in 2025 to USD 245.7 billion in 2026 and to USD 341 billion by 2031, registering a CAGR of 6.8% between 2026 and 2031.

This report is Segmented by Product Type (Brandy and Cognac, Liqueur, Rum, Tequila and Mezcal, Whiskies, White Spirits, Other Spirit Types), End User (Men, Women), Distribution Channel (On-Trade, Off-Trade), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Premium Spirits Market Trends and Insights

Premiumization And Trading Up Across Core Spirits Occasions

Premiumization remains the clearest value driver in the premium spirits market, but it is now happening in a more selective way than it did during the earlier phase of broad-based price-led expansion. Consumers are still trading up, although they are doing it on fewer occasions and with stronger attention to whether a bottle or serve feels worth the extra spend. That behavior is helping categories with stronger quality cues, clear production stories, and visible serving rituals retain momentum even when the wider alcohol category looks softer. It also means the premium spirits market is becoming less tied to total category volumes and more tied to the quality of the purchase occasion itself. Accessible premium price points are therefore in a stronger position than ultra-luxury tiers, because they meet both aspiration and affordability without forcing consumers to abandon premium participation altogether. This shift is reshaping assortment, channel strategy, and new product planning across the premium spirits market, especially for brands that need repeat purchase rather than one-time prestige demand.

Rising Disposable Income In Emerging Urban Middle Classes

Rising incomes in emerging urban markets continue to provide one of the most durable support layers for the premium spirits market, especially where premium alcohol has historically been underpenetrated outside major cities. India stands out in the source draft as the clearest example, with premium and super-premium spirits demand widening beyond metropolitan centers into Tier 2 and Tier 3 cities as spending power, digital retail access, and social acceptance improve. This change matters because it broadens the addressable base for the premium spirits market from a narrow affluent cohort to a larger group of aspirational consumers making step-up purchases more frequently. It also gives multinational and local producers a stronger reason to build regional distribution, premium education, and entry-premium portfolios rather than rely only on top-city premium sales. The opportunity is not limited to one consumer profile, because the source draft also points to younger, more occasion-driven buying behavior and a wider mix of premium preferences across whisky, rum, vodka, and craft-led categories. Over the forecast period, the premium spirits market is likely to benefit most where income gains are matched by better channel reach and clear product positioning rather than by income growth alone.

Excise Duties and Tax-Driven Shelf Price Inflation

Higher duties are a significant short-term constraint on the premium spirits market. These duties elevate shelf prices just as consumers are willing to trade up, but only within set spending limits. In the UK, the duty increases over the last three years have surpassed 17%. Despite these tax hikes, spirits duty revenue dropped by GBP 94 million (USD 126.9 million) in the fiscal year 2025-26. This decline underscores how pricing pressures can dampen both demand and tax revenues. The impact is particularly severe on the more affordable segment of the premium spirits market. Here, consumers are more sensitive to price changes compared to those at the luxury end. Consequently, brands positioned as 'accessible premium' face a tighter challenge, needing to balance price, perceived value, and sales volume. In markets with intricate local tax systems, the challenge intensifies. Import duties, state levies, and specific markups compound, limiting pricing flexibility. If these fiscal pressures continue, the premium spirits market will increasingly lean towards brands with robust pricing power or those employing a more strategic approach to costs and distribution channels.

Other drivers and restraints analyzed in the detailed report include:

- Cocktail Culture and Premium On-Trade Recovery

- Brand Premiumization Through Heritage, Craft, And Storytelling

- Health, Moderation, And Alcohol Reduction Trends

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, whiskies claimed a 22.9% share of the premium spirits market, solidifying their position as the dominant product type globally. This dominance is bolstered by the global appeal of American bourbon, Scotch single malts, Irish whiskey, Japanese whisky, and Indian whisky. These diverse expressions not only deepen the category's geographic reach but also introduce multiple premium entry points. Whisky's versatility, being suitable for both sipping and cocktails, has fortified its demand in both retail and hospitality sectors. In North America, bourbon holds a special significance. Its cultural familiarity, relevance in gifting, and rich brand heritage ensure premium pricing, even amidst selective broader alcohol spending. The whisky segment in the premium spirits market enjoys a diverse range of price points, enabling consumers to gradually trade up rather than making a significant leap in expenditure.

White spirits are projected to lead the premium spirits market with a 4.1% CAGR through 2031. This growth is attributed to gin's evolution into an artisanal category and vodka's resurgence in premium ready-to-drinks (RTDs) and cocktails. White spirits' versatility allows them to seamlessly transition across social occasions, bar formats, and diverse consumer groups, unlike categories that predominantly focus on neat consumption. Notably, larger producers are strategically investing in craft gin assets, signaling a belief in the long-term significance of premium white spirits in their portfolios. Moving forward, while white spirits may not outright displace whisky, they are poised to capture a larger share of premium occasions and adaptable serving formats.

Complete Report Scope:

- By Product Type

- Brandy and Cognac

- Liqueur

- Rum

- Tequila and Mezcal

- Whiskies

- White Spirits

- Other Spirit Types

- By End User

- Men

- Women

- By Distribution Channel

- On-Trade

- Off-Trade

- Specialty/Liquor Stores

- Other Off Trade Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Belgium

- Sweden

- Poland

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- Morocco

- Nigeria

- Egypt

- Rest of Middle East and Africa

- North America

Geography Analysis

In 2025, North America commanded a dominant 36.9% share of the premium spirits market, solidifying its position as the largest regional player. Anchored by the United States, which boasted a staggering USD 36.4 billion in spirits revenue, the region's strength is evident. While premium bourbon and Tennessee whiskey anchor the domestic base, vodka, tequila, and mezcal diversify offerings for various occasions and consumer types. Both Canada and Mexico bolster the regional profile: Canada fuels demand for premium whisky, and Mexico enhances its standing through domestic consumption and a robust export market for premium agave. Despite challenges such as tariff uncertainties and the complexities of imported spirits in supply chains and pricing, North America's scale, brand recognition, and advanced retail infrastructure ensure its leadership in the premium spirits arena.

Asia-Pacific is set to lead the charge, forecasting a robust 6.2% CAGR growth in the premium spirits market through 2031. India stands out as the primary growth driver, witnessing an uptick in both premium and super-premium segments across a broader array of cities and categories. The region's compelling growth narrative is fueled by rising incomes, urbanization, digital accessibility, and an eagerness to explore both imported and domestic premium spirits. While China remains significant, its trajectory appears uneven: domestic baijiu gifting is stabilizing, while select international channels and export activities are on the rise. Meanwhile, nations like Japan, South Korea, Taiwan, and segments of Southeast Asia enrich the narrative, bolstering demand for premium whisky and travel-linked purchases.

Europe, despite a slower expansion pace compared to Asia-Pacific and facing more stringent policy pressures than North America, remains a pivotal player in the premium spirits market. The region's advantages lie in its rich category heritage, robust on-trade demand bolstered by tourism, and the prominence of markets such as the UK, Germany, France, Italy, and Spain. However, the UK faces challenges: repeated duty hikes are straining consumer affordability and limiting volume growth, even as average selling prices hold steady. While South America and the Middle East and Africa currently operate on a smaller scale, they present emerging opportunities, particularly for premium whisky, rum, and travel retail gifting. The Middle East's travel retail hubs are especially noteworthy, with international departures and a penchant for premium gifting elevating the spirits mix. Collectively, the landscape reveals a premium spirits market led by North America's mature demand, buoyed by Asia-Pacific's rising premium adoption, and influenced by Europe's heritage and tourism, alongside select emerging markets.

- Diageo plc

- Pernod Ricard S.A.

- Bacardi Limited

- Brown-Forman Corporation

- LVMH Mo-t Hennessy Louis Vuitton SE

- Suntory Holdings Limited

- Beam Suntory, Inc.

- Campari Group

- R-my Cointreau

- William Grant and Sons Ltd.

- Edrington Group

- Sazerac Company, Inc.

- Constellation Brands, Inc.

- HiteJinro Co., Ltd.

- Becle, S.A.B. de C.V.

- Kweichow Moutai Co., Ltd.

- Wuliangye Yibin Co., Ltd.

- Kirin Holdings Company, Limited

- Asahi Group Holdings, Ltd.

- Davide Campari-Milano N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization and trading up across core spirits occasions

- 4.2.2 Rising disposable income in emerging urban middle classes

- 4.2.3 Cocktail culture and premium on-trade recovery

- 4.2.4 Brand premiumization through heritage, craft, and storytelling

- 4.2.5 Provenance transparency and traceability as a purchase trigger

- 4.2.6 Duty-free and travel retail recovery supporting premium mix

- 4.3 Market Restraints

- 4.3.1 Excise duties and tax-driven shelf price inflation

- 4.3.2 Health, moderation, and alcohol reduction trends

- 4.3.3 Fragmented licensing and route-to-market complexity

- 4.3.4 Advertising, labeling, and promotion restrictions

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE )

- 5.1 By Product Type

- 5.1.1 Brandy and Cognac

- 5.1.2 Liqueur

- 5.1.3 Rum

- 5.1.4 Tequila and Mezcal

- 5.1.5 Whiskies

- 5.1.6 White Spirits

- 5.1.7 Other Spirit Types

- 5.2 By End User

- 5.2.1 Men

- 5.2.2 Women

- 5.3 By Distribution Channel

- 5.3.1 On-Trade

- 5.3.2 Off-Trade

- 5.3.2.1 Specialty/Liquor Stores

- 5.3.2.2 Other Off Trade Channels

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Belgium

- 5.4.2.8 Sweden

- 5.4.2.9 Poland

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Peru

- 5.4.4.5 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Turkey

- 5.4.5.5 Morocco

- 5.4.5.6 Nigeria

- 5.4.5.7 Egypt

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Diageo plc

- 6.4.2 Pernod Ricard S.A.

- 6.4.3 Bacardi Limited

- 6.4.4 Brown-Forman Corporation

- 6.4.5 LVMH Mo-t Hennessy Louis Vuitton SE

- 6.4.6 Suntory Holdings Limited

- 6.4.7 Beam Suntory, Inc.

- 6.4.8 Campari Group

- 6.4.9 R-my Cointreau

- 6.4.10 William Grant and Sons Ltd.

- 6.4.11 Edrington Group

- 6.4.12 Sazerac Company, Inc.

- 6.4.13 Constellation Brands, Inc.

- 6.4.14 HiteJinro Co., Ltd.

- 6.4.15 Becle, S.A.B. de C.V.

- 6.4.16 Kweichow Moutai Co., Ltd.

- 6.4.17 Wuliangye Yibin Co., Ltd.

- 6.4.18 Kirin Holdings Company, Limited

- 6.4.19 Asahi Group Holdings, Ltd.

- 6.4.20 Davide Campari-Milano N.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK