PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061758

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061758

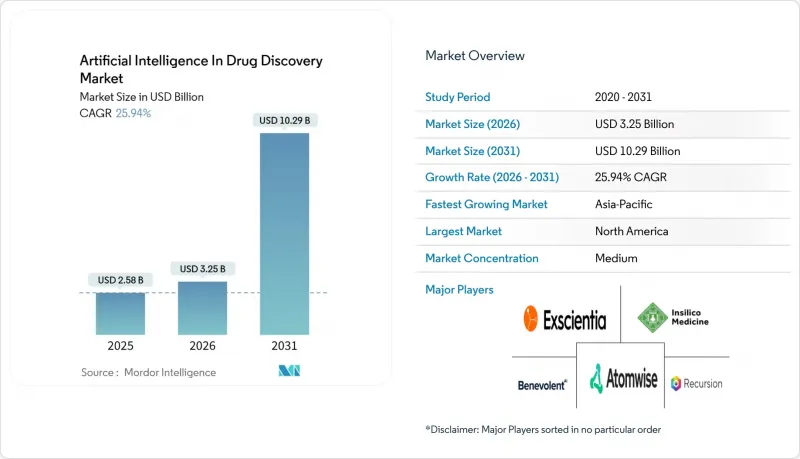

Artificial Intelligence In Drug Discovery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the artificial intelligence in drug discovery market size was valued at USD 2.58 billion in 2025 and is estimated to grow from USD 3.25 billion in 2026 to reach USD 10.29 billion by 2031, at a CAGR of 25.94% during the forecast period (2026-2031).

This report is Segmented by Component (Software and Service), Technology (Machine Learning, and More), Application (Target Identification & Validation, and More), Drug Type (Small Molecule, and More), Deployment (Cloud-Based and On-Premise), End User, and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Artificial Intelligence In Drug Discovery Market Trends and Insights

Rising Biopharmaceutical R&D Cost Pressures

A 40% decline in R&D productivity between 2010 and 2024 prompted executives to fund predictive algorithms that shortened lead-optimization cycles from 18 months to 6 months. Exscientia demonstrated in 2025 that its AI-designed molecules progressed to first-in-human studies inside a single year, evidencing cash-on-cash returns that traditional medicinal-chemistry workflows cannot match. Rare-disease programs stand to gain most because limited patient pools restrict break-even sales. Budget-constrained biotechs increasingly license turnkey AI services, helping explain why services outpace software in compound annual growth. The artificial intelligence in drug discovery market, therefore, functions as a cost-avoidance mechanism rather than an incremental expense line.

Growing Global Disease Burden Across Chronic and Infectious Areas

Chronic illnesses accounted for 74% of worldwide mortality in 2025, yet only a fraction of new molecular entities addressed metabolic or cardiovascular pathways. AI platforms interrogate multi-omic datasets to surface polygenic targets that elude reductionist screening. During the 2024 mpox resurgence, a generative-chemistry engine identified repurposing candidates inside 48 hours, illustrating real-time responsiveness that manual methods lack. Oncology still concentrates 38% of AI projects, but neurodegeneration is the fastest-expanding domain as algorithms merge brain imaging with proteomics to stratify patient subsets. The artificial intelligence in drug discovery market, therefore, scales in direct proportion to the global epidemiological shift toward chronic, multi-factorial conditions.

Regulatory and Clinical Adoption Challenges Related to AI Explainability

FDA's 2025 draft guidance obliges sponsors to document model lineage and decision boundaries, yet most neural networks remain opaque. Without mechanistic rationales, clinical investigators hesitate to enroll patients, slowing trial accrual. The European Medicines Agency formed an AI committee in 2025, but harmonized rules are years away. Attention mechanisms improve interpretability but at the cost of predictive power, creating a trade-off that sponsors must navigate. In the artificial intelligence in drug discovery market, these compliance hurdles translate into longer validation timelines and greater documentation overhead.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Strategic Collaborations Between Pharmaceutical and AI Companies

- Expansion of High-Quality Biomedical Data Assets

- Limited Availability of Integrated Multidisciplinary Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services expanded at a 27.54% CAGR through 2031, outpacing the 62.43% baseline share held by software in 2025. This shift indicates that many companies view algorithmic discovery as an enabling layer rather than a core competency. The artificial intelligence in drug discovery market size for services reached USD 0.79 billion in 2026, reflecting heightened demand for turnkey target-identification pipelines. Contract research organizations now integrate active-learning modules that clients pay for per project, thereby converting fixed costs into variable outlays. Software remains indispensable because it preserves internal IP control over proprietary libraries. However, the spread of per-simulation pricing blurs boundaries, effectively turning license models into usage-based services. Over time, if AI-discovered molecules demonstrate superior Phase III success rates, large pharma may rationalize vendor rosters, dampening service-segment fragmentation.

Pharmaceutical majors, therefore, hedge by maintaining small in-house data-science teams alongside external contracts, ensuring optionality. The service value proposition resonates strongly with seed-stage biotechs that lack capital for a dedicated compute stack. Regulatory demand for validated audit trails further favors specialized vendors offering documentation as a managed service. Consequently, the artificial intelligence in drug discovery market continues to bifurcate between platform providers with recurring subscription revenue and project-based consultancies that monetize depth of therapeutic expertise.

Machine-learning frameworks dominated 46.54% of 2025 spend, but quantum approaches are on track for a 27.65% CAGR to 2031. The artificial intelligence in drug discovery market size attributable to quantum algorithms is projected to surpass USD 1 billion by 2031 if hardware error-correction milestones arrive on schedule. Presently, algorithms such as neural-quantum states simulate under 100 atoms, limiting scope. Natural-language processing, with 18% share, mines 30 million biomedical publications to enrich knowledge graphs. Computer-vision models process 10-terabyte image sets from phenotypic screens, holding 12% share.

Model-foundation trends are converging: several firms fine-tune open-source protein models like ESM-2 rather than train bespoke architectures, cutting data requirements by 80%. Quantum readiness partnerships-for example, IBM and Moderna-signal future scaling paths for complex biologic simulations. Should fault-tolerant qubits become commercially viable, the artificial intelligence in drug discovery market could witness a rapid reweighting toward quantum-native vendors.

Geography Analysis

North America commanded 43.54% share in 2025, supported by FDA guidance that offers early clarity for AI-assisted dossiers. Venture funding in the United States reached USD 4.1 billion in 2025, of which 62% flowed to companies progressing at least one asset into Phase II. Canada's Vector Institute partnered with eight pharmaceutical companies to co-develop protein-engineering foundation models. Mexico's CRO community is onboarding AI modules to compete with Asian peers, yet broadband gaps delay full cloud migration. While the region's share may ease to 40% by 2031, North America will likely remain the cradle for algorithmic advances, propelling the artificial intelligence in the drug discovery market.

London's Life-Sciences Accelerator injected GBP 100 million into 15 start-ups, burnishing the city's status as Europe's leading AI-biotech hub[3]. Germany trails on deployment: only 35% of pharma companies had operational AI pipelines in 2025. Southern Europe's academic clusters-particularly Barcelona and Milan-leverage public funds to build open-science data lakes, creating fertile grounds for spinouts. Europe's projected 24% CAGR ensures it will outpace North America but remain behind APAC in growth velocity.

Asia-Pacific is the fastest-growing region at 26.54% CAGR through 2031. China doubled its global project share to 12% in 2025, spurred by state incentives and sovereign-AI mandates. Insilico Medicine advanced three molecules into trials, the highest count for any APAC firm. India's Syngene shortened lead-optimization cycles to three weeks using AI-enhanced retrosynthesis planning. Japan's Takeda tapped Preferred Networks to auto-design antibodies, a move expected to seed regional know-how spillovers. South Korea and Australia run government-funded initiatives but still lack deep venture ecosystems. Middle East and Africa captured 4% share, while South America secured 3%, constrained by underdeveloped R&D infrastructure and human-capital shortages. APAC's trajectory will determine whether the artificial intelligence in drug discovery market evolves into a tri-polar ecosystem or remains skewed toward the trans-Atlantic corridor.

- Aitia

- Ardigen

- Atomwise Inc.

- Auransa Inc.

- Benevolent AI

- BioXcel Therapeutics

- Cloud Pharmaceuticals

- Cyclica Inc.

- Deep Genomics

- Eagle Genomics

- Evotec

- Exscientia PLC

- Genesis Therapeutics

- Healx

- IBM

- Innoplexus AG

- Insilico Medicine

- Isomorphic Labs (Alphabet)

- Iktos

- Microsoft

- NVIDIA

- Peptilogics

- PostEra

- Recursion Pharmaceuticals Inc.

- Schrodinger Inc.

- Standigm

- Turbine AI

- Valo Health

- Verge Genomics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope Of The Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Biopharmaceutical R&D Cost Pressures

- 4.2.2 Growing Global Disease Burden Across Chronic and Infectious Areas

- 4.2.3 Increasing Strategic Collaborations Between Pharmaceutical and AI Companies

- 4.2.4 Expansion of High-Quality Biomedical Data Assets

- 4.2.5 Advancing Cloud and High-Performance Computing Accessibility

- 4.2.6 Emergence of Next-Generation AI Drug Design Paradigms

- 4.3 Market Restraints

- 4.3.1 Regulatory and Clinical Adoption Challenges Related to AI Explainability

- 4.3.2 Limited Availability of Integrated Multidisciplinary Talent

- 4.3.3 Data Fragmentation and Lack Of Standardization Across Research Silos

- 4.3.4 Intellectual Property and Liability Uncertainties for AI-Generated Molecules

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat Of New Entrants

- 4.7.2 Bargaining Power Of Buyers

- 4.7.3 Bargaining Power Of Suppliers

- 4.7.4 Threat Of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Service

- 5.2 By Technology

- 5.2.1 Machine Learning

- 5.2.2 Natural Language Processing

- 5.2.3 Computer Vision

- 5.2.4 Quantum Machine Learning

- 5.3 By Application

- 5.3.1 Target Identification & Validation

- 5.3.2 Hit Generation & Prioritization

- 5.3.3 Lead Optimization

- 5.3.4 Candidate Screening

- 5.3.5 Drug Repurposing

- 5.3.6 De Novo Drug Design

- 5.3.7 Pre-Clinical Safety & Toxicity Assessment

- 5.4 By Drug Type

- 5.4.1 Small Molecule

- 5.4.2 Biologics

- 5.4.3 Gene And Cell Therapy

- 5.5 By Deployment

- 5.5.1 Cloud-Based

- 5.5.2 On-Premise

- 5.6 By End User

- 5.6.1 Pharmaceutical & Biotechnological Companies

- 5.6.2 Academic & Research Institutes

- 5.6.3 Other End Users

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest Of Europe

- 5.7.3 APAC

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest Of APAC

- 5.7.4 Middle East And Africa

- 5.7.4.1 Middle East

- 5.7.4.1.1 GCC

- 5.7.4.1.2 Turkey

- 5.7.4.1.3 Rest Of Middle East

- 5.7.4.2 Africa

- 5.7.4.2.1 South Africa

- 5.7.4.2.2 Rest Of Africa

- 5.7.4.1 Middle East

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest Of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-Level Overview, Market-Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share For Key Companies, Products & Services, And Recent Developments)

- 6.4.1 Aitia

- 6.4.2 Ardigen

- 6.4.3 Atomwise Inc.

- 6.4.4 Auransa Inc.

- 6.4.5 BenevolentAI

- 6.4.6 BioXcel Therapeutics

- 6.4.7 Cloud Pharmaceuticals Inc.

- 6.4.8 Cyclica Inc.

- 6.4.9 Deep Genomics

- 6.4.10 Eagle Genomics

- 6.4.11 Evotec SE

- 6.4.12 Exscientia PLC

- 6.4.13 Genesis Therapeutics

- 6.4.14 Healx

- 6.4.15 IBM Corporation

- 6.4.16 Innoplexus AG

- 6.4.17 Insilico Medicine Inc.

- 6.4.18 Isomorphic Labs (Alphabet)

- 6.4.19 Iktos

- 6.4.20 Microsoft Corporation

- 6.4.21 NVIDIA Corporation

- 6.4.22 Peptilogics

- 6.4.23 PostEra

- 6.4.24 Recursion Pharmaceuticals Inc.

- 6.4.25 Schrodinger Inc.

- 6.4.26 Standigm

- 6.4.27 Turbine AI

- 6.4.28 Valo Health

- 6.4.29 Verge Genomics

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment