PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061839

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061839

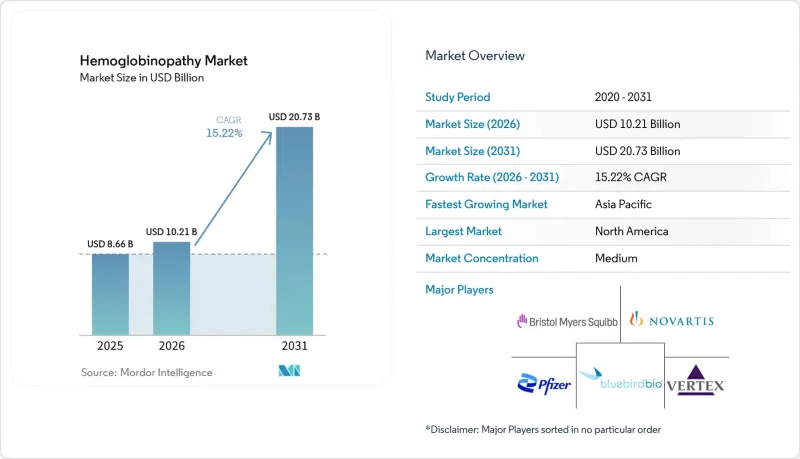

Hemoglobinopathy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the hemoglobinopathy market size is expected to increase from USD 8.66 billion in 2025 to USD 10.21 billion in 2026 and reach USD 20.73 billion by 2031, growing at a CAGR of 15.22% over 2026-2031.

This report is Segmented by Disorder Type (Sickle Cell Disease, Beta-Thalassemia, and More), Product {Therapy Type (Pharmacological Agents, Gene Therapy, and More), Diagnosis Technique (Hemoglobin Electrophoresis, HPLC, and More)}, End User (Hospitals, Specialty Clinics, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Hemoglobinopathy Market Trends and Insights

Rising Prevalence of SCD & Thalassemia

Rising birth rates, migration, and better disease detection keep pushing global hemoglobinopathy numbers upward. Close to 8 million people now live with sickle cell disease, and the toll is heaviest in Sub-Saharan Africa, where more than 500 children die each day for lack of timely care. Population growth in high-burden regions keeps the treatment gap wide even as new screening programs uncover cases that once went unnoticed. For drug makers, this unmet need translates into a sizeable and growing market, especially for therapies that can be delivered in settings with limited resources.

Regulatory Approvals of Disease-Modifying Drugs

Between 2023 and 2024, the U.S. FDA cleared several first-in-class therapies-including CRISPR-based products-that act on the root cause of hemoglobinopathies instead of masking symptoms. Final guidance on genome-editing products, issued in January 2024, gives developers a clearer path to approval. Similar moves by the European Medicines Agency, coupled with orphan-drug and accelerated-review incentives, trim development time and strengthen the business case for niche but high-impact treatments.

Multi-Million-Dollar Therapy Prices Strain Payers

List prices for approved gene therapies fall between USD 2.2 million and USD 3.1 million per patient, a level that many budgets cannot absorb without cutting other services. Faced with such costs, payers often impose strict coverage criteria and multi-step authorization reviews, slowing treatment starts even when the clinical need is urgent. Medicaid bears much of the burden because a large share of sickle-cell patients rely on that program, yet state budgets leave limited room for high-ticket therapies. Outcomes-based contracts help, but hospitals must still finance the full procedure upfront, squeezing cash flows and discouraging additional treatment-center build-outs.

Other drivers and restraints analyzed in the detailed report include:

- Breakthrough Gene-Editing Cures Attract Investment

- Annuity-Based Reimbursement for Gene Therapies

- Weak Hematology Infrastructure in Low- And Middle-Income Countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sickle cell disease held 37.31% hemoglobinopathy market share in 2025, a level supported by the immediate eligibility of this patient group for the first approved CRISPR-based curative therapies. Newborn-screening mandates in high-income countries and large Medicaid pools in the United States sustain demand visibility. At the same time, private-equity-backed programs aim to replicate this model in Latin America and the Caribbean. B-thalassemia, projected to grow at 16.03% CAGR through 2031, benefits from the same therapeutic platforms adapted to different globin-gene mutations, and pilot sites are already onboarding adult patients before expanding to pediatric cohorts. Alpha-thalassemia remains small but attractive for pipeline expansion as diagnostic resolution improves.

Market entrants are building consortia with regional reference laboratories to triage patients directly into clinical sites, a move that compresses referral times and maximizes procedure capacity. Novartis's collaboration with the Bill & Melinda Gates Foundation illustrates further commitment to simplified in-vivo editing intended for low-resource settings, potentially repositioning the company as a gateway provider when large-volume, lower-price opportunities emerge.

Geography Analysis

North America's 29.84% revenue share in 2025 reflects robust Medicaid coverage for sickle cell disease, concentration of certified gene-therapy centers, and a well-established philanthropic ecosystem that subsidizes travel and lodging for eligible patients. Federal support through the Cell and Gene Therapy Access Model lowers payer risk, encouraging additional states to sign outcomes-based contracts and thereby enlarging the treated population.

Europe follows with steady adoption, aided by the European Medicines Agency's conditional approval pathway that allowed earlier market entry for ex vivo gene additions. Budget discipline tempers procedure counts, yet multi-country tender frameworks give manufacturers visibility into volume commitments. Notably, four national health services are piloting annuity payments where budgets are reimbursed over time, replicating the United States model to manage headline prices.

Asia Pacific is advancing at a 17.28% CAGR. India and China together account for the region's bulk demand due to high birth prevalence, government-funded newborn screening, and emergent middle-class willingness to self-pay for premium care. Public-private partnerships are converting tertiary hospitals into specialized editing centers, ensuring future scale. Southeast Asian nations are also adopting AI-enabled carrier-screening to inform family planning, enlarging the catchment for the hemoglobinopathy market.

The Middle East and Africa host the highest disease prevalence yet the lowest procedure penetration. Opportunities exist for modular clean-room suites and mobile apheresis units that can leapfrog legacy infrastructure constraints. Brazil anchors South American growth with a unified hemoglobinopathy registry and a fast-growing transplant network, signaling rising regional demand as regulatory approvals expand.

- Agios Pharmaceuticals

- AstraZeneca

- Bluebird Bio

- Bristol-Myers Squibb

- CRISPR Therapeutic

- Cyclerion Therapeutics

- Editas Medicine

- Emmaus Life Sciences

- Gilead Sciences

- Graphite Bio

- Intellia Therapeutics

- Novartis

- Orchard Therapeutics

- Pfizer

- Regenxbio

- Sanofi

- Sangamo Therapeutics

- Silence Therapeutics

- Takeda Pharmaceuticals

- Vertex Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of SCD & Thalassemia

- 4.2.2 Regulatory Approvals of Disease-Modifying Drugs

- 4.2.3 Breakthrough Gene-Editing Cures Attract Investment

- 4.2.4 Expansion of National Newborn-Screening Programs

- 4.2.5 Annuity-Based Reimbursement for Gene Therapies

- 4.2.6 AI-Enabled Low-Cost Carrier Screening Platforms

- 4.3 Market Restraints

- 4.3.1 Multi-Million-Dollar Therapy Prices Strain Payers

- 4.3.2 Weak Hematology Infrastructure in LMICs

- 4.3.3 Regulatory Uncertainty on Off-Target Edits

- 4.3.4 Cultural Resistance to Genetic Counselling

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Disorder Type

- 5.1.1 Sickle Cell Disease (SCD)

- 5.1.2 Beta-Thalassemia

- 5.1.3 Alpha-Thalassemia

- 5.1.4 Other Hb Variants (Hb C, Hb E, etc.)

- 5.2 By Product

- 5.2.1 Therapy Type

- 5.2.1.1 Pharmacological Agents

- 5.2.1.2 Gene Therapy

- 5.2.1.3 Bone-Marrow / Stem-Cell Transplant

- 5.2.1.4 Blood Transfusion & Iron Chelation

- 5.2.2 Diagnosis Technique

- 5.2.2.1 Hemoglobin Electrophoresis

- 5.2.2.2 High-Performance Liquid Chromatography (HPLC)

- 5.2.2.3 Molecular Genetic Testing (PCR / NGS)

- 5.2.2.4 Point-of-Care Rapid Tests

- 5.2.2.5 Others

- 5.2.1 Therapy Type

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Clinics & Transfusion Centers

- 5.3.3 Diagnostic Laboratories

- 5.3.4 Academic & Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Agios Pharmaceuticals

- 6.3.2 AstraZeneca

- 6.3.3 Bluebird Bio

- 6.3.4 Bristol Myers Squibb

- 6.3.5 CRISPR Therapeutics

- 6.3.6 Cyclerion Therapeutics

- 6.3.7 Editas Medicine

- 6.3.8 Emmaus Life Sciences

- 6.3.9 Gilead Sciences

- 6.3.10 Graphite Bio

- 6.3.11 Intellia Therapeutics

- 6.3.12 Novartis AG

- 6.3.13 Orchard Therapeutics

- 6.3.14 Pfizer Inc.

- 6.3.15 Regenxbio

- 6.3.16 Sanofi

- 6.3.17 Sangamo Therapeutics

- 6.3.18 Silence Therapeutics

- 6.3.19 Takeda Pharmaceutical

- 6.3.20 Vertex Pharmaceuticals

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment