PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061879

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061879

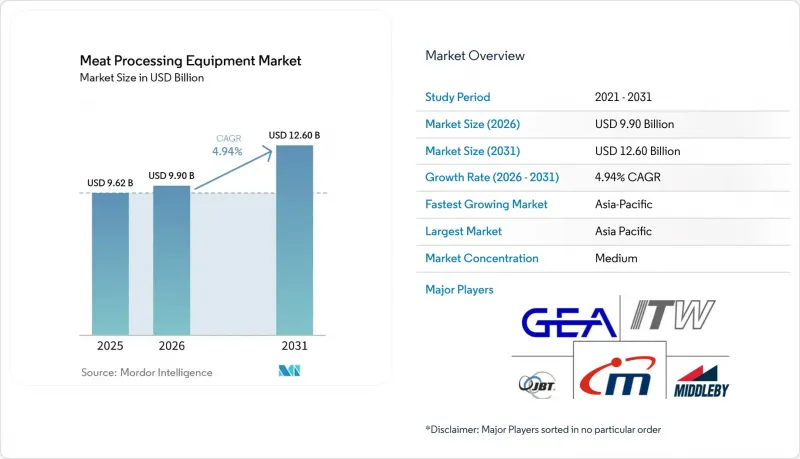

Meat Processing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the meat processing equipment market size is expected to increase from USD 9.62 billion in 2025 to USD 9.90 billion in 2026 and reach USD 12.60 billion by 2031, growing at a CAGR of 4.94% over 2026-2031.

This report is Segmented by Equipment Type (Cutting and Slicing, Grinding and Mixing, and More), Meat Type (Pork, Beef, Poultry, and Mutton), Automation Level (Fully-Automated, Semi-Automated, and Manual/Hand Guided), End User (Industrial, Butcheries, and Horeca), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Meat Processing Equipment Market Trends and Insights

Labor-Scarce Facilities Turn to Automation

In North America and Europe, chronic workforce shortages are hastening the shift from manual tasks like deboning, trimming, and portioning to robotic cells and vision-guided cutting systems. In 2024, Delmarva Poultry Industry revealed that its member processors invested over USD 50 million in automation projects. This move comes in response to the challenge of filling 1,000 open positions in the region, with a goal of achieving a 20% reduction in labor dependency by 2027. While poultry leads the charge, the trend is evident in beef and pork plants too. These facilities are now employing collaborative robots for repetitive tasks, such as belly scoring and primal separation, leading to improved yield consistency and fewer musculoskeletal injuries. Furthermore, automation allows processors to sustain line speeds even during seasonal labor shortages. This capability is crucial, especially when there's consistent year-round consumer demand for portion-controlled products. The momentum is building: as equipment OEMs enhance machine-learning algorithms for tasks like carcass grading and defect detection, the shortened return-on-investment timelines are enticing mid-tier processors to join the automation movement, standing shoulder to shoulder with larger integrators.

Rising Global Meat Consumption in Emerging Asia

Since 1990, meat consumption in Asia has surged, now averaging about 98 pounds per person annually. However, this figure still lags behind North American and European levels, indicating significant growth potential. In 2026, China's per-capita beef consumption dipped by 5% as consumers, facing economic challenges, gravitated towards more affordable pork and poultry. This shift not only boosted activity at poultry and pork processing plants but also heightened the demand for advanced equipment like high-speed evisceration lines, automated cut-up systems, and inline weighing tools. India's poultry industry is witnessing rapid growth, buoyed by increasing incomes and urban migration. Meanwhile, countries in Southeast Asia, including Thailand, Indonesia, and Vietnam, are modernizing their older slaughter facilities. This upgrade aims to align with export certification standards set by Japan, the Middle East, and the European Union. Such regional advancements are advantageous for equipment suppliers offering comprehensive solutions, including integrated cold-chain logistics, traceability software, and halal-compliant processing. As a result, the Asia-Pacific region is on track to be the fastest-growing area, boasting a projected CAGR of 6.02% through 2031.

High Capital Outlay and Lengthy ROI

Investing in advanced processing equipment demands a hefty upfront cost, often deterring smaller and mid-tier processors who operate on tight margins. For instance, installing a spray chiller at a beef plant comes with a USD 2 million price tag, yet it can yield an impressive USD 5 million annually by enhancing yield and minimizing shrinkage. On the other hand, a thermal-management system, costing USD 5 million, promises annual energy savings of USD 2.2 million, translating to a payback period of just 2.3 years, as reported by the Wiley Online Library. Yet, processors lacking access to affordable financing or grappling with uncertain demand often sideline such ambitious projects. Instead, they lean towards incremental upgrades, prolonging the lifespan of their existing equipment. Highlighting the financial intricacies, the Utah State University Meat Processing Center crafted a financial-analysis tool tailored for smaller plants, specifically those processing under 750 heads annually. Their findings underscore the sensitivity of 20-year net-present-value calculations to variables like throughput growth, labor-cost inflation, and equipment residual value. This capital-intensive landscape has led to a divided market: while large integrators, buoyed by robust balance sheets and private-equity support, chase aggressive automation strategies, smaller operators find it challenging to justify investments that risk obsolescence before achieving break-even.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Food-Safety Regulations Drive Equipment Upgrades

- AI-Enabled Predictive-Maintenance Modules Reduce Downtime

- Volatile Livestock Supply and Disease Outbreaks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, grinding and mixing equipment claimed a dominant 33.54% market share, underscoring its crucial role in processed meat production. These systems play a vital role in producing global staples such as sausages, patties, and ground meats. Their versatility across different meat types and scalability make them indispensable for both large processors and smaller niche players. Noteworthy innovations, like Air Products' LIN-IS liquid nitrogen injection system, highlight strides in grinding efficiency and hygiene, ensuring optimal low temperatures during the mixing and grinding processes.

On the other hand, cutting and slicing equipment is emerging as the fastest-growing segment, with a projected CAGR of 5.08% extending to 2031. The increasing demand for portion-controlled and value-added meat products fuels this surge. The industry is leaning towards precision cutting technologies to ensure uniformity, reduce waste, and meet retail presentation standards. For example, Marel's AI-driven cutting systems harness vision and machine learning to enhance speed and accuracy. Meanwhile, blending and marinating machines are in demand due to the booming ready-to-cook segment, while tenderizing, massaging, smoking, and curing systems cater to premium and regional product niches.

In 2025, pork processing equipment secured a commanding 38.69% market share, reinforcing pork's position as the globe's most consumed meat. The diverse range of pork products, from fresh cuts to bacon and sausages, demands specialized equipment, cementing its role in both industrial and regional processing facilities. However, this dominance grapples with challenges posed by shifting consumption trends favoring leaner proteins and sustainability.

Poultry processing equipment is rapidly gaining traction, with forecasts suggesting a 5.67% CAGR through 2031. This surge is driven by rising health awareness, lower production costs, and poultry's reduced environmental impact. Innovations, such as BAADER's ProFlex cut-up solution, boasting the ability to process 7,500 birds per hour with anatomical precision, underscore the segment's rapid evolution. While beef processing equipment sees consistent demand in developed markets, emerging markets are displaying a growing appetite. Mutton processing, albeit niche, holds profound cultural significance in areas like South Asia and the Middle East. The distinct processing needs of each meat type are propelling both equipment innovation and market growth.

Geography Analysis

In 2025, Asia-Pacific dominates the market with a 39.40% share and leads in growth, boasting a 6.02% CAGR projected through 2031. This highlights the region's pivotal role in the global meat processing equipment arena. Countries like China and India are modernizing their meat processing infrastructure, driven by rapid urbanization, surging protein demand, and significant government investments. China is pushing for automation in beef processing, championing intelligent farming initiatives. Meanwhile, India's INR 15,000 crore (USD 1,550 million) infrastructure fund is focused on facility development, aiming to uplift its currently modest meat processing rates.

North America and Europe, though not the quickest to grow, play a crucial role in the market. Their emphasis on food safety, regulatory adherence, and technological advancements keeps them at the forefront. Demand for automation and equipment upgrades is steady in these regions. Compliance mandates, such as the U.S. FSMA 204 traceability requirements, are compelling processors to update their legacy systems. While market saturation poses challenges for rapid growth, there's a notable investment trend towards premium, high-efficiency systems, especially from industrial processors aiming for better yields and reduced labor.

South America and the Middle East and Africa are witnessing gradual growth, fueled by rising domestic meat consumption and slight enhancements in processing capacity. Yet, challenges like currency fluctuations, import tariffs, and restricted capital access often stall equipment upgrades. In Brazil and Gulf nations, meat production driven by exports and food security initiatives bolsters market growth.

- Marel hf.

- GEA Group AG

- JBT Corporation

- Illinois Tool Works Inc.

- The Middleby Corporation

- Buhler Holding AG

- Provisur Technologies Inc.

- BAADER Group GmbH & Co. KG

- Bizerba SE & Co. KG

- Heat and Control Inc.

- Ross Industries Inc.

- Bettcher Industries

- Minerva Omega Group

- Weber Maschinenbau GmbH

- Handtmann Maschinenfabrik

- FPEC Corp.

- Magurit Gefrierschneider GmbH

- Vemag Maschinenbau GmbH

- Promarksvac Corporation

- Nu-Meat Technology Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Labor-scarce facilities turn to automation

- 4.2.2 Rising global meat consumption in emerging Asia

- 4.2.3 Stricter food-safety regulations drive equipment upgrades

- 4.2.4 Shift to ready-to-eat and value-added meat products

- 4.2.5 AI-enabled predictive-maintenance modules reduce downtime

- 4.2.6 Decarbonization pressures driving CO2-efficient thermal systems market

- 4.3 Market Restraints

- 4.3.1 High Capital Outlay and Lengthy ROI

- 4.3.2 Volatile Livestock Supply and Disease Outbreaks

- 4.3.3 Trade-Policy Uncertainty on Meat Exports

- 4.3.4 Limited Skilled Operators for Smart Machinery

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Equipment Type

- 5.1.1 Cutting and Slicing Equipment

- 5.1.2 Grinding and Mixing Equipment

- 5.1.3 Blending and Marinating Equipment

- 5.1.4 Tenderizing and Massaging Equipment

- 5.1.5 Smoking and Curing Chambers

- 5.1.6 Others

- 5.2 Meat Type

- 5.2.1 Pork

- 5.2.2 Beef

- 5.2.3 Poultry

- 5.2.4 Mutton

- 5.3 Automation Level

- 5.3.1 Fully-Automated Lines

- 5.3.2 Semi-Automated Lines

- 5.3.3 Manual/Hand-Guided Equipment

- 5.4 End User

- 5.4.1 Industrial

- 5.4.2 Butcheries

- 5.4.3 HoReCa

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Sweden

- 5.5.2.7 Belgium

- 5.5.2.8 Poland

- 5.5.2.9 Netherlands

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Thailand

- 5.5.3.5 Singapore

- 5.5.3.6 Indonesia

- 5.5.3.7 South Korea

- 5.5.3.8 Australia

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Peru

- 5.5.4.5 Chile

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Positioning Analysis

- 6.4 Company Profiles

- 6.4.1 Marel hf.

- 6.4.2 GEA Group AG

- 6.4.3 JBT Corporation

- 6.4.4 Illinois Tool Works Inc.

- 6.4.5 The Middleby Corporation

- 6.4.6 Buhler Holding AG

- 6.4.7 Provisur Technologies Inc.

- 6.4.8 BAADER Group GmbH & Co. KG

- 6.4.9 Bizerba SE & Co. KG

- 6.4.10 Heat and Control Inc.

- 6.4.11 Ross Industries Inc.

- 6.4.12 Bettcher Industries

- 6.4.13 Minerva Omega Group

- 6.4.14 Weber Maschinenbau GmbH

- 6.4.15 Handtmann Maschinenfabrik

- 6.4.16 FPEC Corp.

- 6.4.17 Magurit Gefrierschneider GmbH

- 6.4.18 Vemag Maschinenbau GmbH

- 6.4.19 Promarksvac Corporation

- 6.4.20 Nu-Meat Technology Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK