PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061901

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061901

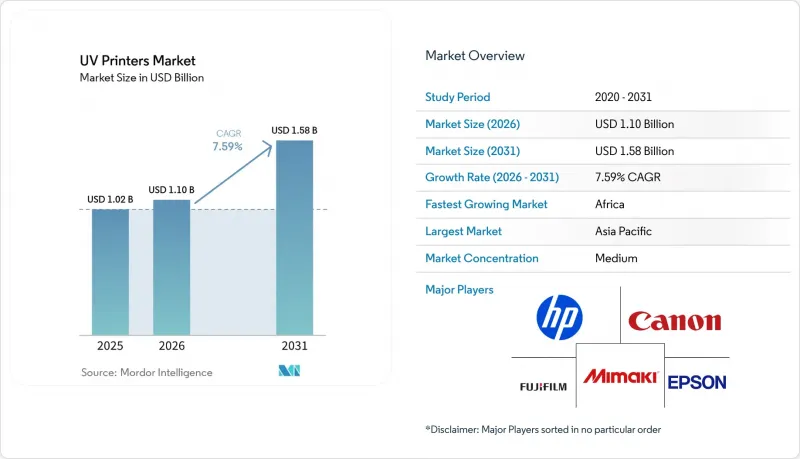

UV Printers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the uV printers market size was valued at USD 1.02 billion in 2025 and is estimated to grow from USD 1.10 billion in 2026 to reach USD 1.58 billion by 2031, at a CAGR of 7.59% during the forecast period (2026-2031).

This report is Segmented by Printer Type (Flatbed, Roll-To-Roll, and Hybrid), Format Size (Small and Medium Format, and More), Ink Source (UV-LED, and More), Application (Sign and Graphics, Packaging and Labels, Industrial Manufacturing, Textile and Soft Signage, and More), End-User Industry (Print Service Providers, In-House, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global UV Printers Market Trends and Insights

Rapid Adoption of UV LED-Curing Technology Reducing Operating Costs

Field measurements at a German print facility in 2024 showed UV LED arrays cutting energy use by 72.5% compared with mercury-arc lamps, with ROI within 18 months despite higher sticker prices. Instant on-off switching removes costly warm-up cycles, while 20,000-hour diode life means bulb changes become irrelevant. The absence of ozone generation eliminates the need for exhaust ducting, which can add USD 5,000-USD 15,000 to a new shop's budget. LED's cooler output protects thin films and foamed plastics from warping, widening the UV printers market into packaging segments once dominated by water-based or EB curing.

Growing Demand for Short-Run Customized Packaging

Plate costs of USD 800-USD 1,200 per SKU make analog flexography uneconomical below 1,000 units, pushing e-commerce brands toward digital UV lines capable of two-week turnarounds. ePac's 2025 deal to install more than ten HP Indigo 200K presses exemplifies the rush to meet limited-edition and regional launch schedules. Variable data, QR codes, and personalized graphics add margin lift that offsets ink cost premiums, fuelling an expanding slice of the UV printers market.

High Initial Capital Expenditure for Wide and Superwide Format Printers

Production-class UV hybrids run USD 80,000-USD 250,000, an outlay that strains SMEs in regions where leasing penetration is below 20%. A 2025 MTU Tech analysis pegged the first-year cash requirement for a mid-range flatbed at USD 70,000, a level many shops earning under USD 200,000 annually cannot absorb. Desktop units under USD 15,000 fill hobby niches but lack throughput, leaving a financing gap that slows the expansion of the ultraviolet (UV) printer market in developing economies.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Industrial Inkjet Printing in Electronics Manufacturing

- Stringent Environmental Regulations Favoring Low-VOC UV Inks

- Limited Substrate Compatibility for Certain UV Ink Formulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid platforms pulled a 7.86% CAGR outlook because they let operators pivot between rigid and roll stock without unbolting media, raising uptime by 30% compared with two single-purpose units. Flatbeds with 45.21% share continued to dominate interiors and industrial decor, where 8-inch Z-clearance accommodates thick substrates, whereas roll-to-roll lines retained speed leadership on flexible banners. The UV printers market for flatbeds remains anchored by promotional products and rigid signage, but hybrids are winning new orders as PSPs retrofit floor plans for multifunction gear. Maintenance complexity does rise, servo-driven roll handlers and vacuum zones add USD 15,000-USD 25,000 to purchase price, yet surveys show faster payback when job mixes swing unpredictably.

The UV printers market also witnessed Turkish firm UVionArt demonstrate flatbeds printing of scratch-resistant architectural glass, highlighting how niche applications sustain demand for dedicated rigs. Conversely, soft-signage specialists still prefer continuous roll feeders for seamless 50-meter banners. A growing subset of packaging prototypers now uses hybrids to print both E-flute carton mock-ups and pressure-sensitive label stock in a single shift, slashing changeovers from 2 hours to 15 minutes. As automation levels climb, hybrids are expected to grab share from single-purpose systems without cannibalizing the high-end flatbed market.

Large-format units measuring 1.5 m or more in width accounted for 70.08% of 2025 sales, driven by transit advertising and building wraps. Yet small and medium formats are growing at 7.65% CAGR, propelled by front-of-house custom gift shops and in-store kiosks adopting desktop UV models that slide through a standard doorway. Roland's LEF2-200 at USD 14,995 exemplifies this democratization, enabling single-operator stores to produce phone cases and trophies without rigging crews. Direct-to-object capacity to decorate 32 tumblers in 10 minutes illustrates why compact rigs monetize high-margin personalization with minimal floor space.

Large-format lines maintain throughput economies, hitting 110 boards per hour on 4x8-foot sheets, keeping the cost per square meter below USD 5 at volumes above 500 m2 per month. Mid-format bridges like Epson's V7000 deliver large-board capability on single-phase power, making them suitable for suburban shops that lack three-phase service. Urban rent pressures tilt demand toward smaller footprints, so format choice increasingly aligns with real estate economics rather than with the application mix alone. Collectively, diversification by size segments keeps the ultraviolet (UV) printers market rolling across enterprise scales.

Geography Analysis

Asia-Pacific generated 38.43% of global revenue in 2025, underpinned by China's UV LED chip foundries, Japan's high-precision printhead research and development, and India's regulatory push against solvent emissions. China's smartphone and automotive clusters value flatbeds that register layers within 100 µm on curved parts, anchoring demand for high-accuracy platforms. Mimaki's May 2026 launch of the UJV200-160 with automatic dot adjustment targets PSPs seeking to widen material menus without adding headcount. Meanwhile, India's Maharashtra and Gujarat states tightened VOC caps, prompting solvent shops to migrate to UV LED workflows free of exhaust ducting.

North America combines robust direct-to-object adoption with a pronounced skills gap; 95% of print shops report difficulty recruiting operators, prompting vendors to embed workflow automation and remote diagnostics. Ricoh's March 2026 alliance with LogoJET leverages that need by bundling small-format DTO units into existing wide-format fleets. Europe's converters prioritize REACH-compliant inks, illustrated by Fotocenter.es installing Agfa's Ciervo H2500 hybrid in January 2026 to future-proof personalized photo output. Canada, facing similar labor shortages, has seen service contracts eclipse hardware margins as suppliers offer uptime guarantees to offset operator deficits.

South America, the Middle East, and Africa deliver the fastest trajectories. Dubai and Abu Dhabi are positioning as exhibition graphics hubs, boosting hybrid printer imports, while South Africa and Egypt shift from solvent to UV to meet occupational exposure rules. Africa's 7.97% CAGR benefits smaller sign shops upgrading to LED units that run on single-phase power, cutting hazardous-waste handling costs. Brazil's flexible packaging lines embraced UV inkjet for food labels, capitalizing on rapid SKU turnover. Financing remains a constraint as equipment leasing penetration averages below 20%, so vendors offering deferred payment or ink-indexed leases are capturing share in the UV printers market.

- HP Inc.

- Canon Inc.

- Fujifilm Holdings Corporation

- Mimaki Engineering Co., Ltd.

- Seiko Epson Corporation

- Roland DG Corporation

- Electronics For Imaging, Inc.

- Durst Group AG

- Agfa-Gevaert NV

- Ricoh Company, Ltd.

- Mutoh Holdings Co., Ltd.

- swissQprint AG

- ColorJet India Ltd.

- Shenzhen Handtop Tech Co., Ltd.

- Inca Digital Printers Ltd.

- Konica Minolta, Inc.

- Vanguard Digital Printing Systems Corp.

- Flora Digital Printing System Tech Co., Ltd.

- CET Color Holdings, LLC

- ColDesi, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of UV LED-Curing Technology Reducing Operating Costs

- 4.2.2 Growing Demand for Short-Run Customized Packaging

- 4.2.3 Expansion of Industrial Inkjet Printing in Electronics Manufacturing

- 4.2.4 Stringent Environmental Regulations Favoring Low-VOC UV Inks

- 4.2.5 Rising Investment in Direct-to-Object Printing for 3D Substrates

- 4.2.6 Accelerated Retail Rebranding Cycles Propelling Signage Replacement Rates

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Expenditure for Wide and Superwide Format Printers

- 4.3.2 Limited Substrate Compatibility for Certain UV Ink Formulations

- 4.3.3 Supply Chain Volatility in UV LED Chips and Photoinitiators

- 4.3.4 Skilled Operator Shortage Hindering Optimal Utilization

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printer Type

- 5.1.1 Flatbed

- 5.1.2 Roll-to-Roll

- 5.1.3 Hybrid

- 5.2 By Format Size

- 5.2.1 Small and Medium Format

- 5.2.2 Large Format

- 5.3 By Ink Source

- 5.3.1 UV-LED

- 5.3.2 Mercury-Arc

- 5.4 By Application

- 5.4.1 Sign and Graphics

- 5.4.2 Packaging and Labels

- 5.4.3 Industrial Manufacturing

- 5.4.4 Textile and Soft Signage

- 5.4.5 Interior Decor

- 5.4.6 Electronics and PCB Prototyping

- 5.5 By End-user Industry

- 5.5.1 Print Service Providers (PSPs)

- 5.5.2 In-house

- 5.5.3 Industrial OEMs

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Israel

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 HP Inc.

- 6.4.2 Canon Inc.

- 6.4.3 Fujifilm Holdings Corporation

- 6.4.4 Mimaki Engineering Co., Ltd.

- 6.4.5 Seiko Epson Corporation

- 6.4.6 Roland DG Corporation

- 6.4.7 Electronics For Imaging, Inc.

- 6.4.8 Durst Group AG

- 6.4.9 Agfa-Gevaert NV

- 6.4.10 Ricoh Company, Ltd.

- 6.4.11 Mutoh Holdings Co., Ltd.

- 6.4.12 swissQprint AG

- 6.4.13 ColorJet India Ltd.

- 6.4.14 Shenzhen Handtop Tech Co., Ltd.

- 6.4.15 Inca Digital Printers Ltd.

- 6.4.16 Konica Minolta, Inc.

- 6.4.17 Vanguard Digital Printing Systems Corp.

- 6.4.18 Flora Digital Printing System Tech Co., Ltd.

- 6.4.19 CET Color Holdings, LLC

- 6.4.20 ColDesi, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment