PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061906

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061906

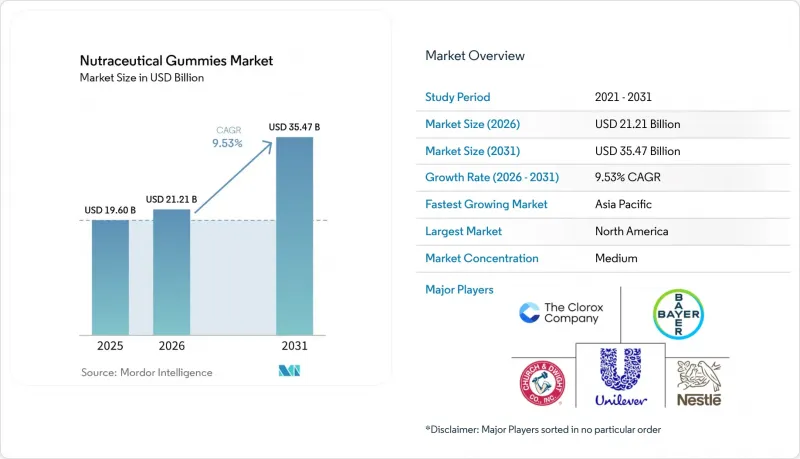

Nutraceutical Gummies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the nutraceutical gummies market size is projected to expand from USD 19.60 billion in 2025 and USD 21.21 billion in 2026 to USD 35.47 billion by 2031, registering a CAGR of 9.53% between 2026 to 2031.

This report is Segmented by Product Type (Digestive, Immunity Support, Beauty and Skin Health, Brain and Cognitive Health, Sleep and Stress Management, Weight Management, and More), End User (Kids and Adults), Distribution Channel (Supermarkets and Hypermarkets, Pharmacies and Health Stores, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Nutraceutical Gummies Market Trends and Insights

Growing Interest in Functional Nutrition

Functional nutrition has shifted from niche wellness circles to mainstream consumer behavior, with gummy formats emerging as a key avenue for ingredient experimentation. A 2025 study published in the Journal of Functional Foods indicated that 62% of consumers in the U.S. and Germany now prioritize bioactive compounds, such as omega-3 fatty acids, adaptogens, and nootropics, over basic vitamins. This represents a significant 19 percentage-point increase compared to 2020. Social media influencers have further driven this change by presenting supplementation as a proactive lifestyle choice rather than a reactive health measure. Gummy supplements leverage this trend by incorporating functional ingredients into a format that minimizes the cognitive resistance associated with pill-swallowing. This approach reduces barriers to both initial trials and repeat purchases. The takeaway is clear: brands that can credibly highlight ingredient origins and clinical validation are well-positioned to capture a larger share of health-conscious consumers.

Convenient and Palatable Supplement Format

Palatability remains the decisive competitive advantage for gummy supplements, particularly as taste preferences diverge across age groups and geographies. Kerry Group's 2026 Taste Charts revealed that gummy formats accounted for 23.4% of the global supplement market, up from 18.1% in 2023, with flavor innovation, such as elderberry, turmeric-ginger blends, and tropical fruit combinations, driving trial among skeptical consumers. Convenience extends beyond taste; single-serving packaging and shelf-stable formulations align with on-the-go consumption patterns, especially among working professionals and parents managing pediatric nutrition. This format advantage is particularly pronounced in the Asia Pacific, where traditional supplement forms like powders and tonics face cultural resistance among younger urban populations. The strategic takeaway is that convenience is not merely a feature but a category-defining attribute that justifies premium pricing and enables cross-category expansion into beauty, sleep, and cognitive health.

Competition from Alternative Formats

Gummy supplements face persistent competition from capsules, tablets, powders, and liquid formats, each offering distinct advantages in bioavailability, dosing precision, or cost efficiency. Capsules and tablets dominate in clinical and pharmacy settings due to standardized dosing and longer shelf life, while powders appeal to fitness enthusiasts seeking customizable serving sizes and rapid absorption. The Council for Responsible Nutrition (CRN) reported in 2025 that capsules and tablets still accounted for 54% of the U.S. dietary supplement market by volume, with gummies capturing 23%, indicating that format preference remains fragmented[3]. Liquid supplements, particularly in single-serve sachets, are gaining traction in Asia Pacific markets where on-the-go consumption patterns favor portability over palatability. The competitive implication is that gummy manufacturers must continuously innovate on texture, flavor, and functional ingredient loading to justify price premiums, while also defending against private-label encroachment in mass retail channels.

Other drivers and restraints analyzed in the detailed report include:

- Rising Consumer Awareness of Probiotics and Gut Health

- Product Innovation: Sugar-Free, Organic, Vegan

- Sugar Content Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, digestive gummies secured a dominant 48.42% share of the nutraceutical gummies market, establishing their leadership with clinically validated multi-strain probiotic blends. This growth reflects increasing consumer awareness of the microbiome's critical role in immunity and mental health. As retailers prioritize gut-health products with prime shelf placement and physicians recommend probiotic gummies for patients who avoid capsules, the market for digestive nutraceutical gummies is expected to expand further. Manufacturers are differentiating their offerings by focusing on strain specificity, ensuring CFU transparency, and adding prebiotic fibers, thereby increasing switching costs for brand-loyal consumers.

Bone and joint health gummies are projected to grow at a faster rate than the overall category, with an anticipated 11.48% CAGR. These formulations, enriched with collagen peptides, vitamin D3, and calcium, appeal to aging populations aiming to preserve mobility. A 2024 randomized trial demonstrated a 4.2% improvement in bone mineral density after 12 months of collagen supplementation. Brands are highlighting clean-label collagen sources, with premium claims such as grass-fed or marine origins. Retailers are integrating bone-health gummies into active-aging displays, driving larger shopper basket sizes.

Geography Analysis

North America held 43.21% nutraceutical gummies market share in 2025, anchored by stringent FDA cGMP oversight, which elevates perceived quality. U.S. brands like Vitafusion and L'il Critters generated USD 637 million in revenue in 2024, underlining continued household penetration. Canadian consumption rises alongside government nutrition campaigns, while Mexico benefits from cross-border e-commerce imports. Market maturity slows unit growth but lifts premiumization, as consumers trade up to vegan or organic lines.

Asia Pacific is forecast to register a 10.46% CAGR during 2026-2031, the fastest globally. Rising disposable incomes in China and India intersect with broader preventive-health narratives. Chinese SAMR labeling reforms enacted in 2024 have increased compliance expense yet boosted consumer confidence. Japan's aging society values bone-health and cognitive gummies, while Australia's well-established pharmacy networks stock immunity and beauty SKUs. Southeast Asian climates magnify stability hurdles, spurring demand for microencapsulated formulas.

Europe ranks third by value, driven by Germany, the United Kingdom, and France, where organic and vegan designations sway purchase decisions. The Netherlands and Sweden show above-average growth as e-pharmacies gain traction. The EU's mooted sugar labeling regulation could trigger regional reformulations, elevating R&D costs but differentiating low-sugar pioneers. South America's expansion clusters around Brazil and Argentina, though currency volatility remains a risk. The Middle East and Africa offer nascent but high-potential opportunities in the United Arab Emirates, Saudi Arabia, and South Africa; fragmented regulations and supply-chain constraints require local partnerships.

- Church And Dwight Co. Inc. (Vitafusion)

- The Bountiful Company (Nature's Bounty)

- Unilever Plc (OllY)

- The Clorox Company (SmartyPants)

- Hero Nutritionals LLC

- Nature's Way (Schwabe)

- Jamieson Wellness Inc.

- Bayer AG (One A Day)

- Pharmavite LLC (Nature Made)

- Nestle S.A. (Garden Of Life)

- Zarbee's Inc. (J&J)

- Goli Nutrition Inc.

- Nature's Truth (Piping Rock)

- Better Nutritionals LLC

- Nordic Naturals

- VitaCup Inc.

- CBDfx

- Charlotte's Web Holdings Inc.

- Vitakem Nutraceutical Inc.

- NutraStar Manufacturing LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Interest In Functional Nutrition

- 4.2.2 Convenient And Palatable Supplement Format

- 4.2.3 Rising Consumer Awareness Of Probiotics And Gut Health

- 4.2.4 Product Innovation Sugar-Free Organic Vegan

- 4.2.5 Increasing Focus On Immunity Post-Pandemic

- 4.2.6 Health And Wellness Focus

- 4.3 Market Restraints

- 4.3.1 Sugar Content Concerns

- 4.3.2 Competition From Alternative Formats

- 4.3.3 Stability And Shelf-Life Issues

- 4.3.4 Allergen And Ingredient Restrictions

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Digestive Gummies

- 5.1.2 Immunity Support Gummies

- 5.1.3 Beauty and Skin Health Gummies

- 5.1.4 Brain and Cognitive Health Gummies

- 5.1.5 Sleep and Stress Management Gummies

- 5.1.6 Weight Management Gummies

- 5.1.7 Bone and Joint Health Gummies

- 5.1.8 Heart Health Gummies

- 5.1.9 Others

- 5.2 By End User

- 5.2.1 Kids

- 5.2.2 Adults

- 5.3 By Distribution Channel

- 5.3.1 Supermarkets And Hypermarkets

- 5.3.2 Pharmacies and Health Stores

- 5.3.3 Online Retail Stores

- 5.3.4 Other Distribution Channels

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Sweden

- 5.4.2.8 Poland

- 5.4.2.9 Belgium

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Vietnam

- 5.4.3.7 Indonesia

- 5.4.3.8 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Peru

- 5.4.4.5 Colombia

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Church And Dwight Co. Inc. (Vitafusion)

- 6.4.2 The Bountiful Company (Nature's Bounty)

- 6.4.3 Unilever Plc (OllY)

- 6.4.4 The Clorox Company (SmartyPants)

- 6.4.5 Hero Nutritionals LLC

- 6.4.6 Nature's Way (Schwabe)

- 6.4.7 Jamieson Wellness Inc.

- 6.4.8 Bayer AG (One A Day)

- 6.4.9 Pharmavite LLC (Nature Made)

- 6.4.10 Nestle S.A. (Garden Of Life)

- 6.4.11 Zarbee's Inc. (J&J)

- 6.4.12 Goli Nutrition Inc.

- 6.4.13 Nature's Truth (Piping Rock)

- 6.4.14 Better Nutritionals LLC

- 6.4.15 Nordic Naturals

- 6.4.16 VitaCup Inc.

- 6.4.17 CBDfx

- 6.4.18 Charlotte's Web Holdings Inc.

- 6.4.19 Vitakem Nutraceutical Inc.

- 6.4.20 NutraStar Manufacturing LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK