PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061941

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061941

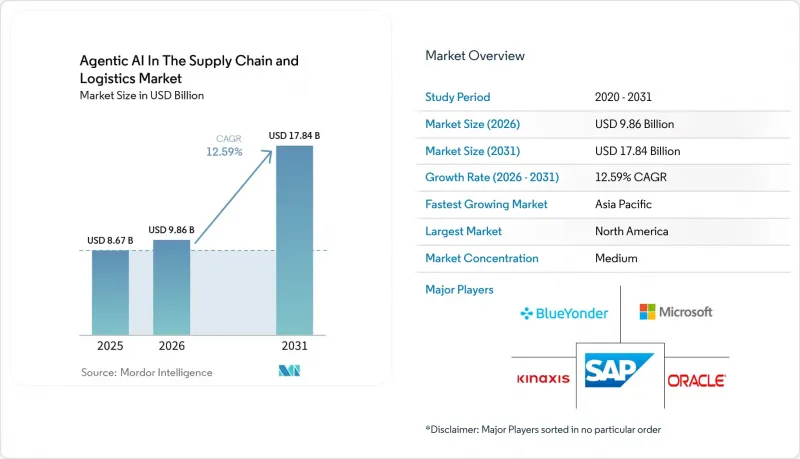

Agentic AI In The Supply Chain And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the agentic AI market in the supply chain and logistics market is expected to grow from USD 9.86 billion in 2026 to USD 17.84 billion by 2031, expanding at a CAGR of 12.59% over the same period.

This report is Segmented by Component (Software Platforms, and More), Application (Demand Forecasting and Planning, Warehouse and Fulfillment Optimization, and More), Industry Vertical (Retail and E-Commerce, Manufacturing, Food and Beverage, and More), Deployment Model (Cloud-Based, On-Premise, and Hybrid), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI In The Supply Chain And Logistics Market Trends and Insights

Rapid Adoption of Cloud-Native SCM Platforms With Embedded AI Agents

Cloud hyperscalers now ship multi-agent tools as part of their supply-chain suites, removing integration friction and cutting decision latency from hours to seconds. Amazon Web Services introduced Connect Decisions in May 2025, while Oracle and SAP followed with embedded agents for demand sensing, freight booking, and customs documentation. Mid-market enterprises lacking in-house AI talent can activate these capabilities through subscription tiers, though platform lock-in risk increases once decision histories accumulate inside proprietary clouds.

Labor Shortages Accelerating Warehouse Automation Investments

Low unemployment and high worker turnover push logistics operators to deploy autonomous mobile robots and humanoid systems controlled by multi-agent frameworks. UPS directed USD 120 million toward AI-driven unloading equipment in 2025, and GXO Logistics reported 22% productivity gains after rolling out Dexterity and Agility Robotics pilots across several sites. Real estate design norms are shifting toward robot-friendly layouts, marginalizing legacy facilities that cannot accommodate automated workflows.

High Integration Costs With Legacy ERP and TMS Systems

Most mid-market operators continue to rely on monolithic databases that use batch updates, which limits their ability to adopt advanced technologies such as event-driven streams for multi-agent AI systems. Transitioning to such systems involves high costs, ranging from USD 5 million to USD 20 million per distribution network, and the implementation process can take up to 3 years. Additionally, each agent platform employs its own proprietary ontologies, necessitating the development of custom middleware solutions. This requirement further complicates the adoption process and exacerbates the productivity disparities between large enterprises, which have the resources to manage such transitions effectively, and smaller enterprises, which often struggle to keep pace.

Other drivers and restraints analyzed in the detailed report include:

- Declining Sensor and Compute Costs Enabling Affordable AI-Enabled Hardware

- Surging Demand for Explainable Agent Governance Frameworks Post EU AI Act

- Data Privacy and Sovereignty Regulations Increasing Compliance Burdens

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AI-driven software captured 57.81% of the total 2025 revenue in the agentic AI market for supply chain and logistics. The agentic AI in the supply chain and logistics market size for hardware is on course to grow faster at 13.19% as edge inference converges with robotics. Falling chip prices and pre-integrated perception stacks shorten payback periods, bringing autonomous forklifts and vision-guided picking within reach of regional carriers. Services revenue scales as integrators retrofit legacy systems, tune vertical agents, and train supervisors. Software suites continue to benefit from consumption pricing and pre-existing cloud relationships, so they remain the entry point for most newcomers.

Enterprises adopt hardware once they trust the orchestration logic resident in their platforms. Jetson-powered robots and Gaudi-based conveyors are bundled with reference agents that slot into leading cloud SCM suites, shrinking integration effort. Hyperscalers thus monetize both subscription software and certified device ecosystems, while robotics vendors differentiate on specialized gripper design, sensor fusion, and safety certifications.

Demand forecasting led 2025 allocation at 35.83% because most retailers and manufacturers already collect the data needed for time-series and causal models. Last-mile orchestration, however, will log the fastest 13.79% CAGR as dense cities, same-day expectations, and labor shortages collide. FedEx pilots achieve 15% reductions in delivery costs when RFID and route-planning agents coordinate vehicles and sidewalk robots. Warehouse optimization remains a core area, as annual U.S. warehouse turnover exceeded 43% and 400,000 vacancies in 2025.

Procurement agents gain traction as benchmark datasets standardize supplier performance, while carbon-aware fleet routing embeds real-time emissions data to satisfy sustainability mandates. Reverse logistics and cross-docking remain niche but rise gradually with e-commerce returns and circular-economy rules. Each sub-segment taps different data modalities, yet all require multi-agent coordination to eliminate manual bottlenecks.

Geography Analysis

North America accounted for 41.83% of 2025 revenue, thanks to mature cloud infrastructure and early adoption by Amazon, UPS, and FedEx. Public-sector incentives for domestic semiconductor fabrication also support the expansion of the edge hardware ecosystem. Europe grows more slowly because the EU AI Act adds documentation overhead, though carbon-aware routing subsidies partially offset compliance costs.

Asia-Pacific is forecast to post the fastest 13.59% CAGR through 2031 as China, India, and Japan channel more than USD 50 billion in sovereign AI funding into domestic hardware and large language models. China's State Council earmarked supply-chain applications, prompting provincial grants for smart ports and bonded-zone logistics. India's startup scene brings agentic procurement tools to small manufacturers, and Japan's aging workforce propels robot adoption in distribution centers.

South America advances as Brazilian e-commerce surpasses half the population, spurring demand for autonomous delivery in Sao Paulo and Rio de Janeiro. Argentina pursues AI-guided freight matching despite macro volatility, while limited broadband in parts of the region slows cloud uptake. The Middle East and Africa remain early-stage, yet the United Arab Emirates and Saudi Arabia fold agentic AI into national logistics corridors aligned with diversification strategies.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Amazon.com Inc.

- IBM Corporation

- NVIDIA Corporation

- Blue Yonder Group Inc.

- Manhattan Associates Inc.

- Kinaxis Inc.

- Coupa Software Inc.

- GXO Logistics Inc.

- Locus Robotics Corp.

- Raft Technologies Ltd.

- OneTrack AI Inc.

- AgentChain Inc.

- Beamup AI Inc.

- Glacis Inc.

- Experidium Inc.

- AGENSTRUM Labs B.V.

- JASCI Software Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Cloud-Native SCM Platforms With Embedded AI Agents

- 4.2.2 Labor Shortages Accelerating Warehouse Automation Investments

- 4.2.3 Declining Sensor and Compute Costs Enabling Affordable AI-Enabled Hardware

- 4.2.4 Surging Demand for Explainable Agent Governance Frameworks Post EU AI Act

- 4.2.5 Rising Usage of Real-Time Emissions Data for Carbon-Aware Routing Incentives

- 4.2.6 Emergence of Autonomous Multi-Agent Benchmark Datasets Standardizing Procurement KPIs

- 4.3 Market Restraints

- 4.3.1 High Integration Costs With Legacy ERP and TMS Systems

- 4.3.2 Data Privacy and Sovereignty Regulations Increasing Compliance Burdens

- 4.3.3 Scarcity of Domain-Specific Simulation Sandboxes Limiting RL Agent Training

- 4.3.4 Enterprise Change-Management Fatigue From Multi-Agent Workflow Overhauls

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 AI-Enabled Hardware Systems

- 5.1.3 Services (Integration and Consulting)

- 5.2 By Application

- 5.2.1 Demand Forecasting and Planning

- 5.2.2 Warehouse and Fulfillment Optimization

- 5.2.3 Transportation Routing and Fleet Management

- 5.2.4 Procurement and Sourcing Automation

- 5.2.5 Last-Mile Delivery Orchestration

- 5.2.6 Other Applications

- 5.3 By Industry Vertical

- 5.3.1 Retail and E-Commerce

- 5.3.2 Manufacturing

- 5.3.3 Food and Beverage

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Automotive

- 5.3.6 Other Industry Verticals

- 5.4 By Deployment Model

- 5.4.1 Cloud-Based

- 5.4.2 On-Premise

- 5.4.3 Hybrid

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Amazon.com Inc.

- 6.4.5 IBM Corporation

- 6.4.6 NVIDIA Corporation

- 6.4.7 Blue Yonder Group Inc.

- 6.4.8 Manhattan Associates Inc.

- 6.4.9 Kinaxis Inc.

- 6.4.10 Coupa Software Inc.

- 6.4.11 GXO Logistics Inc.

- 6.4.12 Locus Robotics Corp.

- 6.4.13 Raft Technologies Ltd.

- 6.4.14 OneTrack AI Inc.

- 6.4.15 AgentChain Inc.

- 6.4.16 Beamup AI Inc.

- 6.4.17 Glacis Inc.

- 6.4.18 Experidium Inc.

- 6.4.19 AGENSTRUM Labs B.V.

- 6.4.20 JASCI Software Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment