PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062038

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062038

Pet Calming Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

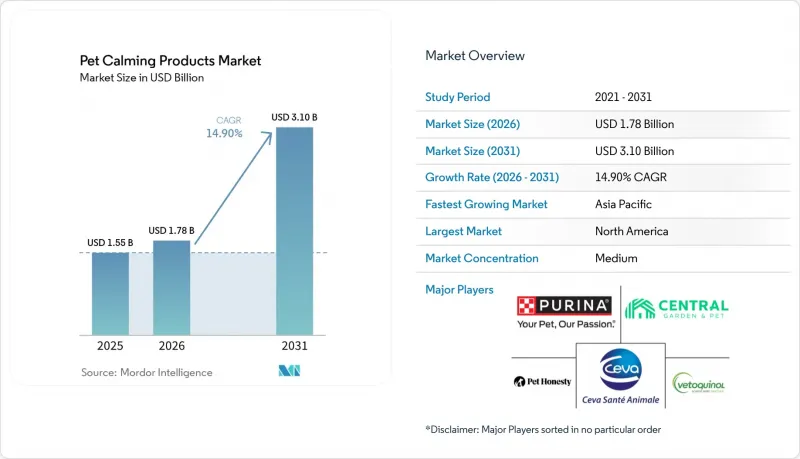

According to Mordor Intelligence, the pet calming products market size is projected to expand from USD 1.55 billion in 2025 and USD 1.78 billion in 2026 to USD 3.10 billion by 2031, registering a CAGR of 14.9% between 2026 and 2031.

This report is Segmented by Product Type (Supplements, Treats, and More), by Pet Type (Dogs, Cats, and More), by Distribution Channel (Online Retail, Specialty Pet Stores, and More), by Form (Edibles, Topicals, and More), by Ingredient Source (Natural and Synthetic), and by Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Pet Calming Products Market Trends and Insights

Rising Pet Anxiety Due to Urban Lifestyles

Urban density exacerbates separation anxiety, noise hypersensitivity, and territorial stress in companion animals, driving consistent demand for calming solutions. The trend toward high-rise living in regions such as Singapore and Hong Kong has reduced outdoor access, confining pet activities to limited spaces and increasing chronic stress indicators. In 2025, research from the Texas A&M College of Veterinary Medicine and Biomedical Sciences (VMBS) revealed that over 99% of dogs in the United States exhibit potentially problematic behaviors, with the most common categories being aggression (55.6%), separation and attachment behaviors (85.9%), and fear and anxiety behaviors (49.9%).

Increasing Humanization of Pets Driving Premium Spend

Pet owners are increasingly allocating discretionary income toward behavioral wellness for their pets, approaching it with the same priority as human healthcare. Anxiety management is now viewed as a preventive measure rather than a reactive one. In 2024, according to the American Pet Products Association (APPA), pet ownership in the United States is experiencing renewed growth, with 94 million households owning at least one pet. Gen Z is notably contributing to a significant rise in multi-pet ownership. Consumer spending patterns in this market parallel trends in the human supplements market, where higher unit costs are accepted for products featuring pharmaceutical-grade botanicals, clinical trial validation, and sustainability certifications.

Regulatory Gray Zones Around Functional Actives

Ambiguous regulatory frameworks for functional ingredients pose compliance risks, delay product launches, and complicate market access strategies. In 2024, the European Food Safety Authority's (EFSA) Panel on Additives and Products or Substances used in Animal Feed (FEEDAP) determined that the additive under assessment is safe for use in complete feed for dogs at a maximum level of 30 mg/kg. This lack of regulatory clarity often leads to conservative labeling practices, which obscure product benefits and reduce conversion rates among pet owners seeking targeted anxiety solutions. In the Asia-Pacific region, regulatory variability is even more pronounced. Companies that invest in regulatory intelligence and maintain adaptable supply chains are better positioned to navigate these complexities. Smaller market entrants often withdraw due to the high costs of compliance.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of E-Commerce Subscription Models

- Adoption of Wearable Biomonitoring Devices

- Limited Double-Blind Clinical Efficacy Studies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Supplements led the largest segment, with 39.0% of pet calming products market share in 2025, this dominance is attributed to consumer preference for easy-to-administer formats such as chews, tablets, and powders, which aid in stress and anxiety relief for pets. These products typically include natural ingredients such as herbs, amino acids, and vitamins, making them a preferred choice for pet owners seeking safe, non-invasive calming solutions. Furthermore, their widespread availability through veterinary channels and retail platforms enhances their market presence.

Pheromone-based products are the fastest-growing segment, projected to advance at an 18.5% CAGR through 2026-2031. These products function by mimicking natural calming signals, effectively reducing stress-related behaviors in pets, particularly dogs and cats. Their growing adoption is driven by increased awareness of behavior-based solutions and endorsements from veterinarians and pet behaviorists. As pet owners increasingly prioritize scientifically supported, non-pharmaceutical approaches, pheromone-based products are gaining significant market traction.

Dogs commanded the largest segment, 62.0% of the pet calming products market share in 2025. This dominance reflects the higher baseline prevalence of anxiety in dogs and the greater willingness of dog owners to invest in behavioral interventions. Factors such as higher global dog ownership rates and increased awareness among dog owners regarding anxiety-related behaviors, including separation anxiety, noise phobia, and travel stress, drive this trend. Additionally, the availability and marketing of a wide range of calming products, such as supplements, chews, collars, and anxiety wraps, further reinforce the leading position of the dog segment.

The cat segment is the fastest-growing, projected to grow at 16.2% CAGR to 2026-2031, attributed to rising cat adoption, particularly in urban areas where cats are often preferred because of their lower maintenance requirements. Increasing awareness of stress-related issues in cats, such as environmental changes and multi-pet households, is also boosting demand for specialized calming solutions. In Asia-Pacific markets, where cats outnumber dogs in urban apartments due to space constraints and landlord restrictions, this trend is particularly pronounced. According to the China Pet Industry Association, the total pet population in China reached 124.1 million in 2024, comprising 52.6 million dogs and 71.5 million cats, reflecting increase of 1.6% and 2.5%, respectively, from 2023.

Geography Analysis

North America led largest region, with 37% pet calming products market share in 2025, this leadership is driven by high pet ownership rates, strong consumer spending on pet wellness, and widespread awareness of stress and anxiety issues in pets. According to the American Pet Products Association (APPA), total United States pet industry expenditures reached USD 152 billion in 2024, reflecting sustained growth and resilience. Well-established retail and e-commerce channels, coupled with a mature veterinary and pet care infrastructure, further support the adoption of a wide range of calming solutions across the region.

Asia-Pacific exhibits the fastest trajectory at 14.9% CAGR through 2026-2031, this rapid growth is fueled by rising pet adoption, increasing disposable incomes, and growing awareness of pet health and wellness. Emerging markets in countries such as China, India, and Southeast Asian nations are witnessing expanding e-commerce penetration and greater availability of innovative calming products, driving accelerated market adoption across the region.

In the European pet calming products market, Germany, France, and the United Kingdom lead regional demand. Specialty pet stores hold stronger market positions in North America than elsewhere, driven by a cultural preference for in-store consultations. Regulatory fragmentation across member states increases compliance costs, benefiting vertically integrated companies with legal teams adept at managing country-specific regulations. This fragmentation often leads to delays in product launches and additional expenses for smaller players, who may lack the resources to effectively address varying compliance requirements.

- Ceva Sant Animale S.A.

- Nestl Purina PetCare Company

- Central Garden & Pet Company

- Vetoquinol S.A. (Soparfin SCA)

- Zoetis Inc.

- Zesty Paws, LLC (H&H Group)

- Spectrum Brands Holdings, Inc.

- Nutramax Laboratories, Inc.

- Radio Systems Corporation

- Swedencare AB

- PetHonesty, LLC

- Virbac S.A.

- Kong Company, LLC

- PetIQ, Inc. (Bansk Group)

- Beaphar B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising pet anxiety due to urban lifestyles

- 4.2.2 Increasing humanization of pets is driving premium spend

- 4.2.3 Surge in veterinarian-led behavioral wellness programs

- 4.2.4 Expansion of e-commerce subscription models

- 4.2.5 Adoption of wearable biomonitoring devices

- 4.2.6 Relaxed hemp-derived Cannabidiol (CBD) regulations in key markets

- 4.3 Market Restraints

- 4.3.1 Regulatory gray zones around functional actives

- 4.3.2 Limited double-blind clinical efficacy studies

- 4.3.3 Pharmaceutical-grade botanical supply constraints

- 4.3.4 Online counterfeits fuel consumer skepticism

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Supplements

- 5.1.2 Treats

- 5.1.3 Pheromone-Based Products

- 5.1.4 Pressure Wraps/Vests

- 5.1.5 Calming Toys

- 5.2 By Pet Type

- 5.2.1 Dogs

- 5.2.2 Cats

- 5.2.3 Other Pet Types

- 5.3 By Distribution Channel

- 5.3.1 Online Retail

- 5.3.2 Specialty Pet Stores

- 5.3.3 Mass Merchandisers/Supermarkets

- 5.3.4 Veterinary Clinics

- 5.4 By Form

- 5.4.1 Edibles

- 5.4.2 Topicals

- 5.4.3 Wearables

- 5.4.4 Devices

- 5.5 By Ingredient Source

- 5.5.1 Natural

- 5.5.2 Synthetic

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 France

- 5.6.2.3 United Kingdom

- 5.6.2.4 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products And Services, And Recent Developments)

- 6.4.1 Ceva Sant Animale S.A.

- 6.4.2 Nestl Purina PetCare Company

- 6.4.3 Central Garden & Pet Company

- 6.4.4 Vetoquinol S.A. (Soparfin SCA)

- 6.4.5 Zoetis Inc.

- 6.4.6 Zesty Paws, LLC (H&H Group)

- 6.4.7 Spectrum Brands Holdings, Inc.

- 6.4.8 Nutramax Laboratories, Inc.

- 6.4.9 Radio Systems Corporation

- 6.4.10 Swedencare AB

- 6.4.11 PetHonesty, LLC

- 6.4.12 Virbac S.A.

- 6.4.13 Kong Company, LLC

- 6.4.14 PetIQ, Inc. (Bansk Group)

- 6.4.15 Beaphar B.V.

7 Market Opportunities and Future Outlook