PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062147

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062147

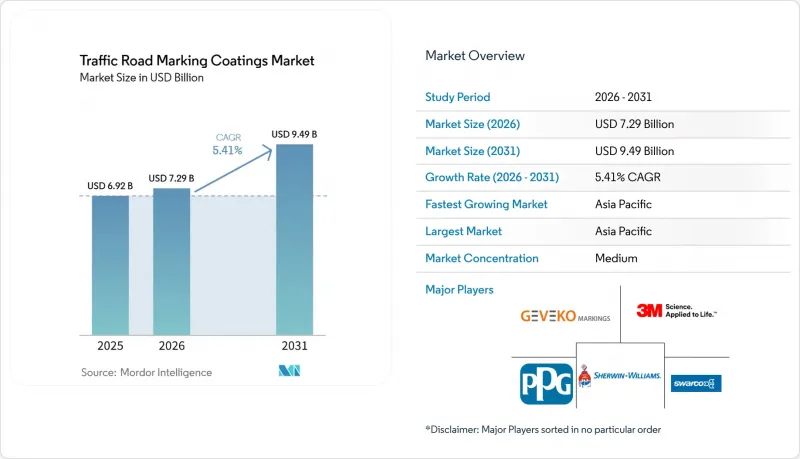

Traffic Road Marking Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

By 2025, Asia-Pacific is expected to represent 41.26% of the global market value and is projected to grow at a CAGR of 6.12% through 2031.

According to Mordor Intelligence, in 2025, the traffic road marking coatings market was valued at USD 6.92 billion. This report is Segmented by Product Type (Water-Based, Solvent-Based, Thermoplastic, and More), Application (Road Lines, Highways, and More), End-User (Municipal, Airport, Highway Contractors, Parking Operators, Industrial), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Traffic Road Marking Coatings Market Trends and Insights

Government Road-Safety Funding Programs (e.g., IIJA-US)

Under the USD 496 billion Infrastructure Investment and Jobs Act, 72.62% of the funds have been allocated. USD 3.5 billion is directed to the FY 2026 Highway Safety Improvement Program, while USD 1 billion remains available for the Safe Streets and Roads for All grants. To meet the March 2026 MUTCD retroreflectivity thresholds, states are moving away from short-life water-based paints. They are now choosing thermoplastic or MMA systems, which have a lifespan of 3-5 years. In India, the Bharatmala initiative has allocated INR 4.72 lakh crore (equivalent to USD 56.5 billion). By February 2026, 22,223 km of the sanctioned 26,425 km had been completed. The remaining portion is planned for completion in FY 2027, driving ongoing demand for durable, high-visibility coatings.

Urban-Traffic Congestion Fueling Lane-Expansion Projects

Eighty-one percent of state DOTs now deploy contrast pavement markings on light-colored substrates to sharpen lane guidance in saturated corridors. The Congestion Relief Grant Program prioritizes advanced striping packages that optimize capacity without full reconstruction, supporting cold-plastic and MMA usage in reversible or managed lanes. With urbanization increasing, Asia-Pacific is experiencing growth in multimodal corridor expansions. In India, the PM Gati Shakti platform integrates 44 ministries on a unified GIS, enabling faster execution of projects like the 1,386 km Delhi-Mumbai Expressway, which is now 82% complete. At the same time, Intelligent Transportation Systems (ITS) in cities such as Warsaw, Singapore, and Lagos are incorporating sensors, driving the demand for machine-vision-compatible markings and supporting the adoption of thermoplastic systems.

Stringent VOC Caps on Solvent-Borne Coatings

The EPA has established a limit of 150 g/L for volatile organic compounds (VOCs) in coatings. Similarly, Canada has implemented the same restriction, although it applies only during the May to October period. These regulatory measures are requiring suppliers to either reformulate their products to comply or withdraw from the market. At the same time, the European Union's REACH proposals regarding per- and polyfluoroalkyl substances (PFAS) are adding to the regulatory challenges faced by the industry. For example, 3M announced its complete exit from PFAS-related operations in 2025. This development highlights how regulatory changes are encouraging a transition towards water-based or methyl methacrylate (MMA) systems.

Other drivers and restraints analyzed in the detailed report include:

- Heightened Focus on Road Safety and Traffic Management

- AV-Ready High-Contrast Marking Demand Surge

- Short Service Life of Legacy Water-Borne Paints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Between 2026 and 2031, cold-plastic MMA coatings are expected to grow at a 5.82% CAGR, exceeding the growth rate of the overall traffic road marking coatings market. In 2025, thermoplastic coatings accounted for 38.11% of the revenue, driven by their durability of 3-5 years. Water-based paints, while leading in volume, contribute to higher lifecycle costs. Solvent-based products face challenges due to strict 150 g/L VOC caps in the United States and seasonal restrictions in Canada. Epoxy coatings are primarily used in high-friction applications such as crosswalks and bridge decks. Nippon Paint, supported by its patent portfolio and the acquisition of AOC, is advancing research and development efforts in low-temperature cures and bio-based binders, which is aiding the adoption of premium MMA coatings. Additionally, improvements in bead technology and the use of anti-icing additives are broadening the applications of these coatings, particularly in Nordic regions and snow-belt states where ice impacts visibility.

In 2025, the thermoplastic traffic road marking coatings market was valued at USD 2.64 billion, with forecasts indicating growth to USD 3.61 billion by 2031. Similarly, MMA's market share is projected to increase from USD 1.62 billion to USD 2.25 billion during the same period. Manufacturers are enhancing retroreflectivity with high-index glass beads and incorporating phase-change materials to reduce ice buildup, improving safety in cold weather conditions.

Geography Analysis

In India, the Bharatmala initiative has completed 22,223 km of highways, with full completion targeted by FY 2027. The Delhi-Mumbai Expressway, approaching its opening, has notable thermoplastic requirements. In China, expressway densification continues, while smart-city projects across ASEAN are implementing ITU-T Y.4232 sensor standards, which require machine-vision-ready markings. Local manufacturing through the PPG and Asian Paints joint venture strengthens supply resilience in the region.

In North America, the USD 496 billion IIJA and the March 2026 MUTCD update are key drivers. The update shifts focus from many water-based products to long-life systems. BABAA's requirement for over 55% domestic content is increasing manufacturing localization, a criterion already met by 3M's plants in Minnesota. In Canada, a seasonal ceiling of 150 g/L VOC is accelerating the transition to cold-plastic alternatives. In Mexico, freight corridors are being upgraded with high-friction surfaces to support USMCA trade routes.

In Europe, stricter VOC thresholds and potential PFAS restrictions are influencing market dynamics. These regulations are driving research and development in water-based acrylics and solvent-free MMAs. Geveko's c-PCR for Environmental Product Declarations is positioning EPD-certified products to align with green procurement initiatives. In Nordic countries, agencies are increasingly using preformed thermoplastics due to their ability to endure freeze-thaw cycles and snow-plow abrasion.

- 3M

- Asian Paints PPG Pvt. Ltd.

- Axalta Coating Systems

- Cinkarna Celje

- Geveko Markings

- JS CHEM CORPORATION

- Nippon Paint Holdings

- PPG Industries, Inc.

- RoadVista

- RPM International Inc.

- SealMaster

- Shaf Sunrise Line Mark Pvt Ltd.

- SWARCO

- The Sherwin-Williams Company

- Tikkurila

- Zhejiang Brother Road Sign Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government road-safety funding programs (e.g., IIJA-US)

- 4.2.2 Urban-traffic congestion fuelling lane-expansion projects

- 4.2.3 Heightened focus on road-safety and traffic management

- 4.2.4 AV-ready high-contrast marking demand surge

- 4.2.5 Mandates for machine-vision-readable thermoplastic markings

- 4.3 Market Restraints

- 4.3.1 Stringent VOC caps on solvent-borne coatings

- 4.3.2 Short service life of legacy water-borne paints

- 4.3.3 Competition from prefabricated tape markings

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Water-based Coatings

- 5.1.2 Solvent-based Coatings

- 5.1.3 Thermoplastic Coatings

- 5.1.4 Cold-Plastic (MMA) Coatings

- 5.1.5 Epoxy-based Coatings

- 5.1.6 Other Product Types

- 5.2 By Application

- 5.2.1 Road Marking Lines

- 5.2.2 Highway Markings

- 5.2.3 Pedestrian Crossings

- 5.2.4 Airports and Runways

- 5.2.5 Parking Lots

- 5.2.6 Anti-Skid Markings

- 5.2.7 Other Applications

- 5.3 By End-User Industry

- 5.3.1 Municipal Authorities

- 5.3.2 Airport Authorities

- 5.3.3 Highway Contractors

- 5.3.4 Commercial Parking Operators

- 5.3.5 Industrial and Warehouse Facilities

- 5.3.6 Other End Users

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 Australia

- 5.4.1.5 South Korea

- 5.4.1.6 ASEAN Countries

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Asian Paints PPG Pvt. Ltd.

- 6.4.3 Axalta Coating Systems

- 6.4.4 Cinkarna Celje

- 6.4.5 Geveko Markings

- 6.4.6 JS CHEM CORPORATION

- 6.4.7 Nippon Paint Holdings

- 6.4.8 PPG Industries, Inc.

- 6.4.9 RoadVista

- 6.4.10 RPM International Inc.

- 6.4.11 SealMaster

- 6.4.12 Shaf Sunrise Line Mark Pvt Ltd.

- 6.4.13 SWARCO

- 6.4.14 The Sherwin-Williams Company

- 6.4.15 Tikkurila

- 6.4.16 Zhejiang Brother Road Sign Co.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment