PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062293

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062293

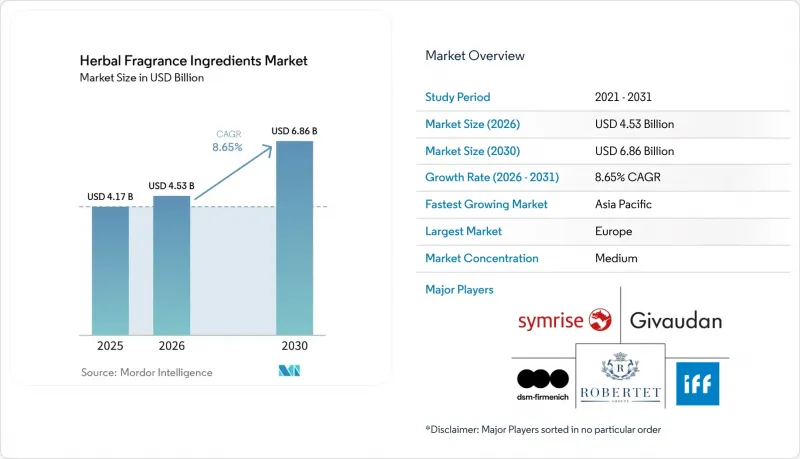

Herbal Fragrance Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the herbal fragrance ingredients market size is expected to grow from USD 4.17 billion in 2025 to USD 4.53 billion in 2026 and is forecast to reach USD 6.86 billion by 2031 at 8.65% CAGR over 2026-2031.

This report is Segmented by Product Type (Lavender, Peppermint, Rosemary, Tea Tree, and More), Form (Liquid, Powder, Others), Application (Fine Fragrances, Personal Care and Cosmetics, Household Care, Aromatherapy and Wellness, Food and Beverages), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Herbal Fragrance Ingredients Market Trends and Insights

Rising consumer preference for natural and plant-based fragrance ingredients

Rising consumer preference for natural and plant-based fragrance ingredients is a key driver of the herbal fragrance ingredients market, as buyers increasingly prioritize clean-label and toxin-free personal care products. Consumers are shifting away from synthetic fragrances and opting for botanical alternatives derived from herbs, flowers, and essential oils due to their perceived safety and wellness benefits. This trend is particularly strong in skincare, perfumes, and home fragrance applications where natural scent profiles are associated with authenticity and sustainability. According to the The Public Health and Safety Organization (NSF) March 2025 report, 74% of consumers consider organic ingredients important in personal care products, highlighting growing demand for clean formulations without harmful additives. The report also noted that 45% of respondents are willing to pay a premium for certified products with organic ingredients, reflecting strong perceived value. This willingness to spend more encourages manufacturers to incorporate herbal fragrance components and emphasize certification claims. Additionally, brands are expanding portfolios with essential oil-based and plant-derived fragrance solutions to meet evolving consumer expectations.

Growing demand for clean-label and chemical-free personal care products

The increasing demand for clean-label and chemical-free personal care products is driving growth in the herbal fragrance ingredients market. Consumers are becoming more conscious of ingredient transparency and are actively seeking formulations free from synthetic fragrances, parabens, and harsh chemicals. This shift is encouraging manufacturers to utilize plant-derived fragrance ingredients sourced from herbs, flowers, and botanical extracts. Herbal fragrance components are perceived as safer and more compatible with sensitive skin, further supporting their adoption in skincare, haircare, and cosmetic products. According to research by CBI Ministry of Foreign Affairs, clean-label products are expected to account for over 70% of product portfolios in 2025 and 2026, rising from 52% in 2021. This significant increase highlights the growing importance of natural and recognizable ingredients across personal care categories. As brands prioritize minimal ingredient lists and chemical-free claims, demand for herbal fragrance ingredients continues to expand.

High cost of natural herbal extracts compared to synthetic alternatives

High cost of natural herbal extracts compared to synthetic alternatives is a key restraint affecting the herbal fragrance ingredients market. The extraction of botanical ingredients such as essential oils and herbal concentrates involves complex processes like steam distillation, solvent extraction, and cold pressing, which significantly increase production costs. Additionally, the yield of active fragrance compounds from natural sources is often low, further elevating overall pricing. Seasonal availability of raw materials and dependence on agricultural output also contribute to supply volatility and cost fluctuations. Compared to synthetic fragrance ingredients, herbal alternatives require higher sourcing, processing, and quality control expenses. This cost disparity limits their adoption, particularly in price-sensitive markets and mass-market personal care products. Manufacturers often face challenges in balancing cost efficiency with consumer demand for natural formulations. As a result, the higher cost structure of herbal extracts continues to restrain broader market penetration despite growing demand for natural ingredients.

Other drivers and restraints analyzed in the detailed report include:

- Increasing use of herbal fragrances in aromatherapy and wellness applications

- Rising awareness regarding adverse effects of synthetic fragrances

- Limited availability and seasonal supply of botanical raw materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Citrus-based ingredients accounted for 28.96% of the herbal fragrance ingredients market in 2025, making them the largest product type segment. Their dominance is primarily driven by widespread use in perfumes, personal care products, home care formulations, and aromatherapy applications. Citrus notes such as lemon, orange, bergamot, and grapefruit are highly preferred for their fresh, clean, and uplifting scent profiles. These ingredients are commonly incorporated into soaps, shampoos, deodorants, and air fresheners due to their refreshing and energizing fragrance characteristics. In addition, citrus-based ingredients are often associated with natural and clean-label positioning, which aligns with growing consumer preference for plant-derived fragrances. Their versatility in blending with floral, woody, and herbal notes further enhances their adoption across multiple fragrance formulations.

Rosemary is projected to register the fastest growth, expanding at a CAGR of 9.12% through 2031. The increasing popularity of herbal and aromatherapy-based fragrance solutions is driving demand for rosemary-derived ingredients. Rosemary offers a distinctive fresh, herbal, and slightly woody aroma, making it suitable for natural perfumes, essential oil blends, and wellness products. The ingredient is also gaining traction in personal care products such as shampoos, skincare formulations, and massage oils due to its perceived therapeutic benefits. Growing consumer interest in stress relief, relaxation, and holistic wellness is further accelerating adoption of rosemary-based fragrances. Additionally, the shift toward natural and plant-based ingredients is encouraging manufacturers to incorporate rosemary into clean-label product formulations.

Geography Analysis

Europe accounted for 33.76% of the herbal fragrance ingredients market revenue in 2025, making it the largest regional segment. The region's leadership is supported by a well-established fragrance and cosmetics industry, particularly in countries such as France, Germany, Italy, and the United Kingdom. Strong consumer preference for natural and botanical-based perfumes and personal care products is driving demand for herbal fragrance ingredients. Additionally, the presence of leading fragrance manufacturers and luxury perfume brands contributes to continuous innovation and product development. Regulatory emphasis on clean-label and sustainable ingredients further encourages the use of plant-derived fragrance components. The growing demand for organic personal care and premium fine fragrances also supports market growth in Europe.

Asia-Pacific is projected to register the fastest growth, expanding at a CAGR of 9.19% through 2031. Rapid urbanization, rising disposable incomes, and expanding middle-class populations are driving demand for personal care and fragrance products across the region. Countries such as China, India, Japan, and South Korea are witnessing increased consumption of herbal and natural fragrance formulations. Growing awareness of wellness, aromatherapy, and traditional botanical ingredients is further supporting market expansion. In addition, local manufacturers are incorporating regionally sourced herbs into perfumes, home fragrances, and personal care applications. The increasing popularity of clean-label cosmetics and natural beauty products is also contributing to strong growth.

North America represents a mature yet steadily growing market, supported by rising demand for clean-label and plant-based fragrance ingredients in cosmetics and home care products. Consumers in the United States and Canada are increasingly adopting aromatherapy, natural perfumes, and wellness-oriented fragrance solutions. South America is witnessing moderate growth, driven by increasing use of botanical ingredients in personal care and home fragrance products, particularly in Brazil and Argentina. Meanwhile, the Middle East and Africa region is gradually expanding due to rising demand for premium perfumes and traditional herbal fragrance oils.

- Givaudan SA

- DSM-Firmenich AG

- International Flavors & Fragrances Inc.

- Symrise AG

- Robertet Group

- Takasago International Corporation

- Mane SA

- Sensient Technologies Corporation

- T. Hasegawa Co., Ltd.

- Bell Flavors & Fragrances

- Frutarom Industries Ltd.

- Huabao International Holdings Ltd.

- Drom Fragrances GmbH & Co. KG

- Aromatech SAS

- Berje Inc.

- Elixens SA

- Ernesto Ventos S.A.

- Phoenix Aromas & Essential Oils LLC

- Alpha Aromatics LLC

- Ungerer & Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising consumer preference for natural and plant-based fragrance ingredients

- 4.2.2 Growing demand for clean-label and chemical-free personal care products

- 4.2.3 Increasing use of herbal fragrances in aromatherapy and wellness applications

- 4.2.4 Expansion of natural cosmetics and organic beauty product launches

- 4.2.5 Rising awareness regarding adverse effects of synthetic fragrances

- 4.2.6 Growing demand from premium and niche perfumery segments

- 4.3 Market Restraints

- 4.3.1 High cost of natural herbal extracts compared to synthetic alternatives

- 4.3.2 Limited availability and seasonal supply of botanical raw materials

- 4.3.3 Shorter shelf life and stability challenges of herbal fragrances

- 4.3.4 Variability in fragrance consistency due to natural ingredient sourcing

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lavender

- 5.1.2 Peppermint

- 5.1.3 Rosemary

- 5.1.4 Tea Tree

- 5.1.5 Citrus-Based (e.g., Orange, Lemon)

- 5.1.6 Others (e.g., Davana, Patchouli)

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Powder

- 5.2.3 Others

- 5.3 By Application

- 5.3.1 Fine Fragrances

- 5.3.2 Personal Care and Cosmetics

- 5.3.3 Household Care

- 5.3.4 Aromatherapy and Wellness

- 5.3.5 Food and Beverages

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Givaudan SA

- 6.4.2 DSM-Firmenich AG

- 6.4.3 International Flavors & Fragrances Inc.

- 6.4.4 Symrise AG

- 6.4.5 Robertet Group

- 6.4.6 Takasago International Corporation

- 6.4.7 Mane SA

- 6.4.8 Sensient Technologies Corporation

- 6.4.9 T. Hasegawa Co., Ltd.

- 6.4.10 Bell Flavors & Fragrances

- 6.4.11 Frutarom Industries Ltd.

- 6.4.12 Huabao International Holdings Ltd.

- 6.4.13 Drom Fragrances GmbH & Co. KG

- 6.4.14 Aromatech SAS

- 6.4.15 Berje Inc.

- 6.4.16 Elixens SA

- 6.4.17 Ernesto Ventos S.A.

- 6.4.18 Phoenix Aromas & Essential Oils LLC

- 6.4.19 Alpha Aromatics LLC

- 6.4.20 Ungerer & Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK