PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064422

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064422

Fragrance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

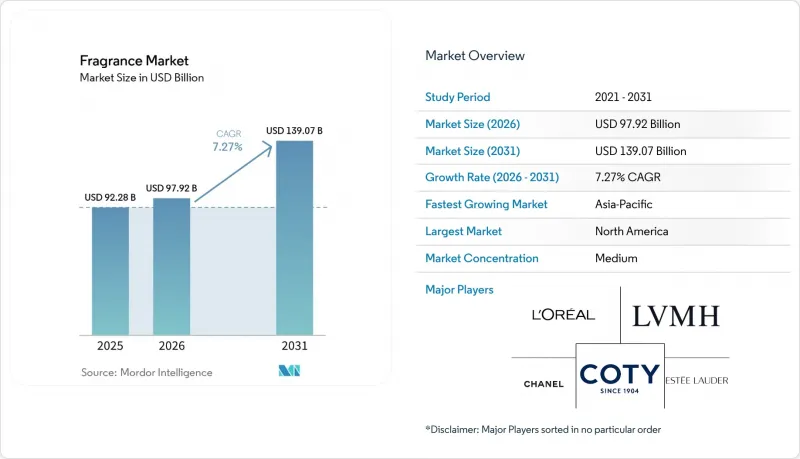

According to Mordor Intelligence, the fragrance market size is expected to increase from USD 92.28 billion in 2025 to USD 97.92 billion in 2026 and reach USD 139.07 billion by 2031, growing at a CAGR of 7.27% over 2026-2031.

This report is Segmented by Product Type (Body Fragrances, Home Fragrances), Category (Organic, Conventional), Price (Mass, Premium/Luxury), Distribution Channel (Hypermarkets/Supermarkets, Specialty Stores, Convenience Stores, Online Retail), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Fragrance Market Trends and Insights

Shift toward natural, clean-label, and sustainable fragrance formulations

Consumer demand for transparency has converted fragrance labeling from a marketing asset into a supply-chain imperative. IFRA's updated Transparency List, now covering over 3,000 ingredients, compels brands to disclose formulation contents at a granularity previously confined to pharmaceutical packaging, effectively raising the competitive floor for ingredient integrity. Ingredient companies are meeting this shift with biotechnology-derived alternatives: Lallemand's Hevani bio-fermented vanillin, commercialized in 2025, offers a supply-chain-stable, crop-independent route to vanilla notes without the yield volatility of conventional Bourbon sourcing. IFF's LMR Naturals unveiled the Tonka Bean CO2 Absolute in February 2026, a 100% natural, traceable ingredient positioned to replace synthetic coumarin in luxury formulations, signaling that green chemistry is now commercially viable at prestige concentrations. Brands that cannot retrofit their ingredient portfolios within the next three to five years face a real risk of shelf exclusion from European and North American premium retail as retailer-led clean-chemistry standards tighten.

Growing demand for niche, artisanal, and bespoke fragrances

The niche segment is redefining value perception at both ends of the price spectrum and forcing mainstream houses to recalibrate their competitive reference points. Amouage delivered double-digit revenue growth in 2025 by expanding directly operated retail while maintaining strict allocation controls in wholesale, demonstrating that scarcity management and channel discipline are as important as product quality in sustaining niche premiums. Parfums de Marly surpassed USD 400 million in retail sales for fiscal 2025, reinforcing the commercial viability of independent houses that combine olfactory storytelling with selective distribution rather than broad wholesale coverage. These results are compelling global conglomerates to acquire or incubate niche properties as a defensive move, not just to access brand equity but to understand the direct-community relationships that niche brands build more efficiently than legacy wholesale models. Olfactory NYC's expansion into Texas in 2025 signals that multi-brand niche fragrance retail is scaling beyond coastal US origins into secondary markets, indicating a structural broadening of the addressable consumer base.

Rising penetration of counterfeit and grey-market fragrances

Counterfeit fragrances represent a supply-side threat that conventional brand-protection investments have consistently struggled to contain at scale. In 2025, Bangkok police seized 34,000 counterfeit perfume units in a single enforcement operation, while Ho Chi Minh City authorities dismantled a counterfeit ring producing replica luxury products with near-authentic packaging quality. France's customs agency confiscated approximately 20,000 counterfeit perfumes at a single checkpoint in 2025, evidence that the problem is not confined to emerging markets and that established European entry points remain vulnerable. The grey market introduces a legally ambiguous dimension: parallel imports diverted from lower-priced regions undercut authorized retailers without triggering traditional enforcement mechanisms, eroding both revenue and the price architecture. Michigan Attorney General Nessel's 2025 felony charges against a domestic counterfeit fragrance network indicate that US enforcement is intensifying, yet the fragmented jurisdictional responses across markets limit systematic global deterrence.

Other drivers and restraints analyzed in the detailed report include:

- Social media influence and celebrity-led brand collaborations

- Premiumization and rising demand for luxury fragrance offerings

- Tightening VOC compliance standards restricting product formulation options

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Body fragrances accounted for 84.6% of value in 2025 and remained the core of the fragrance market, as deodorants are widely used and perfume continues to trade consumers up. Deodorants maintain household penetration across income bands, while perfume formats such as eau de parfum and eau de toilette deliver higher value per unit and support margins. This balance between scale and premium mix explains why body fragrances still anchor the fragrance market even as consumer preferences continue to widen. Home fragrance is projected to grow at a 8.2% CAGR through 2031, making it the fastest-growing product segment as consumers spend more on domestic comfort, wellness routines, and decorative scenting. That momentum also reflects the way the fragrance market now reaches into home aesthetics, where candles, diffusers, and room sprays are purchased for mood, gifting, and everyday use.

Body fragrances still define the revenue base of the category, but home fragrance is closing the gap by capturing spending from consumers who want scent in more than one setting. The product mix is therefore becoming more balanced, with personal scent driving scale and home scent driving incremental premiumization and more frequent experimentation. Room sprays and other ambient formats also function as lower-ticket entry points into premium names, which helps brands recruit new users without relying only on fine fragrance. As this gap narrows, the fragrance market is likely to reward companies that can present a coherent portfolio across both personal and residential use occasions.

Conventional products captured 76.3% of global value in 2025, so they still defined the volume center of the fragrance market. That position reflected the still-limited penetration of organic formulations in mass deodorant and mainstream fine fragrance lines. Organic products are projected to grow at a 9.3% CAGR through 2031, making them the fastest-growing category in the fragrance market as cleaner-label expectations move beyond niche positioning and into broader retail standards. A 2025 study in Frontiers in Toxicology added clinical weight to concerns about dermal sensitization linked to certain synthetic musks, keeping reformulation pressure high for brands that depend on conventional ingredient systems. The result is a category structure in which conventional products still dominate current sales, but the organic tier is setting the direction for future product development.

Organic formulations have a stronger growth profile in the fragrance market, but scaling them requires stable access to traceable natural and biotech-enabled ingredients. The segment is also split between certified organic offerings at the premium end and broader natural or free-from claims at accessible price points, which means brand positioning has to stay precise rather than generic. IFRA's recent standards work has tightened the safety and usage framework around fragrance ingredients, which raises the bar for formulas that want to present as natural while still performing consistently. That shift is resetting cost structures and compressing the gap between conventional and cleaner propositions across the fragrance market.

Geography Analysis

North America accounted for 46.7% of global value in 2025 and remained the largest regional market due to high per-capita spending, broad prestige participation, and a mature specialty retail base. The United States continues to influence launch sequencing and prestige pricing, which gives the region an outsized role in shaping value expectations across the fragrance market. Canada adds room for accessible luxury and cleaner-label premiumization, while Mexico expands the base through mass deodorants and growing mid-tier adoption among younger urban consumers. Europe remains the historical center of fine fragrance, supported by deep production roots, heritage houses, and a consumer base that is comfortable with both luxury and artisanal formats. Regulatory tightening on ingredient safety and disclosure keeps Europe central to formulation review and compliance, reinforcing its importance as a standard-setting region for the fragrance market.

Asia-Pacific is projected to grow at 9.8% CAGR through 2031, the fastest regional pace in the fragrance market, as rising incomes and changing beauty habits widen the consumer base. China still has lower fragrance penetration than mature Western markets, which means even moderate adoption gains can translate into meaningful revenue growth over the forecast period. India is moving along a similar path, with more organized retail helping urban consumers trade up from body sprays into premium fragrance formats. Japan and South Korea support premium demand through a preference for subtler scent profiles, and that preference is influencing product development outside the region as global brands adapt to softer olfactory styles. South America remains important as well because Brazil anchors high-frequency fragrance use, while Colombia, Chile, Argentina, and Peru continue to build a more formal mix of specialty retail and premium demand.

The Middle East and Africa remained a smaller but strategically important part of the fragrance market, with the Gulf states standing out for high spending on oud-led, layered, and bespoke offerings. That demand attracts both global luxury houses and regional specialists, which makes the premium end of the fragrance market especially dynamic in the UAE and Saudi Arabia. Turkey adds manufacturing relevance as well as consumption potential, while South Africa, Nigeria, Egypt, and Morocco represent earlier-stage formalization markets where brand-building today can support stronger loyalty later. Across regions, the fragrance market is increasingly shaped by a split between mature premium centers that set pricing and faster-growth adoption markets that will set the next wave of volume.

- Chanel SA

- The Estee Lauder Companies Inc.

- LVMH Moet Hennessy Louis Vuitton SE

- Coty Inc.

- L'Oreal SA

- Shiseido Company Limited

- Natura and Co.

- Hermes International SA

- Revlon Inc.

- Bath and Body Works Inc.

- Beiersdorf AG

- Inter Parfums, Inc.

- Henkel AG and Co. KGaA

- Unilever Plc

- The Procter and Gamble Company

- Clarins Group

- Puig SL

- Groupe Yves Rocher

- Kao Corporation

- SC Johnson & Sons Inc.

- Reckitt Benckiser Group plc

- Godrej Consumer Products Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift toward natural, clean-label, and sustainable fragrance formulations

- 4.2.2 Growing demand for niche, artisanal, and bespoke fragrances

- 4.2.3 Increasing consumer focus on home aesthetics and wellness-driven lifestyles

- 4.2.4 Social media influence and celebrity-led brand collaborations

- 4.2.5 Premiumization and rising demand for luxury fragrance offerings

- 4.2.6 Growing demand for personalized fragrances

- 4.3 Market Restraints

- 4.3.1 Rising penetration of counterfeit and grey-market fragrances

- 4.3.2 Heightened consumer concerns over synthetic and allergenic ingredients

- 4.3.3 Tightening volatile organic compounds compliance standards restricting product formulation options

- 4.3.4 Regulatory restrictions complicate formulations

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Body Fragrances

- 5.1.1.1 Perfumes

- 5.1.1.2 Deodorants

- 5.1.1.3 Others

- 5.1.2 Home Fragrances

- 5.1.2.1 Candles

- 5.1.2.2 Diffusers

- 5.1.2.3 Room Sprays

- 5.1.2.4 Others

- 5.1.1 Body Fragrances

- 5.2 By Category

- 5.2.1 Organic

- 5.2.2 Conventional

- 5.3 By Price

- 5.3.1 Mass

- 5.3.2 Premium/Luxury

- 5.4 By Distribution Channel

- 5.4.1 Hypermarkets/Supermarkets

- 5.4.2 Specialty Stores

- 5.4.3 Convience Stores

- 5.4.4 Online Retail Stores

- 5.4.5 Other Distribution Channel

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Indonesia

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Turkey

- 5.5.5.5 Nigeria

- 5.5.5.6 Egypt

- 5.5.5.7 Morocco

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Chanel SA

- 6.4.2 The Estee Lauder Companies Inc.

- 6.4.3 LVMH Moet Hennessy Louis Vuitton SE

- 6.4.4 Coty Inc.

- 6.4.5 L'Oreal SA

- 6.4.6 Shiseido Company Limited

- 6.4.7 Natura and Co.

- 6.4.8 Hermes International SA

- 6.4.9 Revlon Inc.

- 6.4.10 Bath and Body Works Inc.

- 6.4.11 Beiersdorf AG

- 6.4.12 Inter Parfums, Inc.

- 6.4.13 Henkel AG and Co. KGaA

- 6.4.14 Unilever Plc

- 6.4.15 The Procter and Gamble Company

- 6.4.16 Clarins Group

- 6.4.17 Puig SL

- 6.4.18 Groupe Yves Rocher

- 6.4.19 Kao Corporation

- 6.4.20 SC Johnson & Sons Inc.

- 6.4.21 Reckitt Benckiser Group plc

- 6.4.22 Godrej Consumer Products Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS