PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062386

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062386

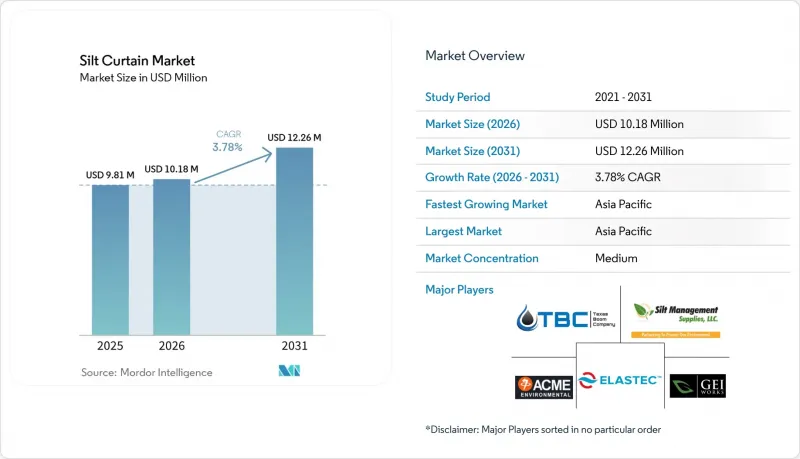

Silt Curtain - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the silt curtain market size is projected to be USD 9.81 million in 2025, USD 10.18 million in 2026, and reach USD 12.26 million by 2031, growing at a CAGR of 3.78% from 2026 to 2031.

This report is Segmented by Type (Type I (Calm Water), Type II (Mild Current), and More), Material (Polyvinyl Chloride, Polyurethane, and More), Application (Dredging, Marine and Coastal Construction, Offshore Energy, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Silt Curtain Market Trends and Insights

Stricter Water-Quality Mandates in Emerging Economies

India's Central Pollution Control Board transitioned from voluntary advisories to mandatory nephelometric thresholds in 2024, requiring dredging contractors to implement real-time monitoring for projects exceeding 10,000 cubic meters. This regulation was first applied to the INR 1,228 million (USD 13.16 million) Paradip maintenance project, scheduled for fiscal 2026-27. In China, the Yangtze River Protection Law was extended to mandate curtain deployment at the Yangshan Phase IV terminal, which added 2.23 million twenty-foot equivalent unit (TEU) capacity in 2025. Thailand's Southern Land Bridge, a USD 28 billion corridor, includes 4.63 kilometers of marine works with mandatory turbidity controls from 2025 to 2030. By the end of 2025, 68% of ports in the region had obtained International Organization for Standardization (ISO) 14001 certification, and bid documents now pre-qualify certain specifications, reducing change-order risks for suppliers.

Surging Offshore Wind Farm Construction Needing Sediment Containment

Monopile driving and cable trenching activities in the North Sea, Yellow Sea, and U.S. Atlantic lease blocks generate sediment plumes that require containment. At Dogger Bank, reinforced polyurethane skirts were mandated during 130 kilometers of cable work due to wave heights exceeding 4 meters. In 2024, Japan's Science Council highlighted typhoon-driven scour risks, prompting project owners to adopt Type III curtains for planned 10 gigawatts (GW) of capacity. South Korea approved 8.2 GW of leases through 2030, incorporating sediment-containment requirements. In the U.S., the Bureau of Ocean Energy Management (BOEM) now delays environmental reviews by an average of nine months if developers fail to demonstrate barrier performance below 40 meters in depth. Manufacturers, including GEI Works, introduced composite-laminate Triton curtains in October 2024 to address these challenges.

Operational Failures in High-Current and Deep-Water Conditions

Standard polyvinyl chloride (PVC) curtains face structural issues, such as bowing or tearing, when exposed to currents exceeding 2 knots or depths beyond 12 meters. In the North Sea, pilots reported anchor pullouts under wave loads of 15 kilonewtons (kN), which doubled mobilization costs for hybrid moorings. Retrofitting weighted ballasts for Five Estuaries wind-farm cables resulted in a 35% cost increase when estuary currents reached 3.2 knots. In the Gulf of Mexico, decommissioning projects in water depths of 60 to 90 meters now require composite laminates with integrated buoyancy chambers. Additionally, fewer than 20% of deployments include real-time turbidity sensors, leading to undetected breaches that extend beyond containment zones.

Other drivers and restraints analyzed in the detailed report include:

- Climate-Adaptation Investments in Beach Nourishment and Mangrove Restoration

- Rise in In-Situ Capping of Contaminated Sediments in Brownfield Ports

- Lengthy Environmental-Permit Delays When Barriers Affect Migratory Species

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type I silt curtains, designed for calm harbor conditions, accounted for 44.11% of the market share in 2025, driven by routine maintenance dredging in protected ports. Meanwhile, Type III curtains are expanding at a compound annual growth rate (CAGR) of 4.41%, supported by applications in North Sea wind farms, Gulf of Mexico decommissioning projects, and Japan's typhoon-prone wind zones. These factors are contributing to higher average selling prices, thereby increasing the overall silt curtain market size. GEI Works' Triton launch introduced a reinforced polyvinyl chloride (PVC) design with a six-foot skirt, rated for five-knot currents, positioning the company to secure contracts for deep-water projects.

The cost disparity between Type I and Type III curtains ranges from USD 60-80 to USD 180-220 per linear meter, reflecting a 30-40% premium due to the inclusion of ballast chains, hybrid anchors, and sensor packages. Deep-water operations beyond 12 meters are driving demand for specialized contractors, reducing addressable volume but increasing profit margins.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 41.11% of global revenue and is projected to grow at a compound annual growth rate (CAGR) of 5.89%. This growth is driven by large-scale port expansions, brownfield remediation projects, and offshore wind allocations. India's hybrid annuity financing model, which allocates 60% of funds during construction and 40% over a 10-year period, enhances cash cycles for domestic barrier manufacturers, thereby increasing the regional silt curtain market share. In China, the 23-port remediation program under the Yangtze Economic Belt prioritizes low-permeability geotextiles. Meanwhile, Thailand's USD 28 billion Southern Land Bridge project ensures six years of consistent demand.

North America's market dynamics are influenced by the Bureau of Ocean Energy Management (BOEM) lease pipeline and state-level beach-resilience budgets. New Jersey's USD 50 million nourishment portfolio and Massachusetts' USD 30 million marsh restoration program contribute to increased near-shore volume. However, Florida's May-October nesting blackout restricts the construction window, leading to higher project insurance costs. Additionally, Canada's Canadian Standards Association (CSA) standard, which differs from the American Society for Testing and Materials (ASTM), complicates import logistics but provides a competitive advantage to local suppliers.

Europe's market growth is primarily driven by offshore wind projects. Leases in areas such as Dogger Bank, Five Estuaries, and the German North Sea require sediment curtains for depths under 30 meters, boosting demand for Type III silt curtain products. The United Kingdom also faces long-term opportunities with the decommissioning of 2,000 offshore platforms, creating a multi-decade growth driver. Incremental opportunities arise from Mediterranean dredging projects in Spain and Italy, as well as Arctic liquefied natural gas (LNG) activities in Russia, though these are constrained by sanctions.

In South America, Brazil's port privatization initiatives are the primary focus of market activity. The Middle East and Africa regions benefit from Saudi Arabia's NEOM coastal developments and South Africa's Durban port deepening projects. Turkey's Kanal Istanbul project remains a potential long-term growth catalyst, pending permit approvals.

- ABASCO

- ACME Environmental

- BMP Supplies Inc.

- BTL

- Clarion Municipal

- Elastec

- Floatex Srl

- Gecko Cleantech

- GEI Works

- JXY Heavy Industry

- Layfield Group

- Silt Management Supplies, LLC.

- Solmax

- Texas Boom Company

- Tritonbuoys

- Water Pollution Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter Water-Quality Mandates in Emerging Economies

- 4.2.2 Surging Offshore Wind Farm Construction Needing Sediment Containment

- 4.2.3 Climate-Adaptation Investments in Beach Nourishment and Mangrove Restoration

- 4.2.4 Rise in In-Situ Capping of Contaminated Sediments in Brownfield Ports

- 4.2.5 Insurance Premium Discounts for Contractors Using Verified Turbidity Controls

- 4.3 Market Restraints

- 4.3.1 Operational Failures in High-Current and Deep-Water Conditions

- 4.3.2 Lengthy Environmental-Permit Delays When Barriers Affect Migratory Species

- 4.3.3 Lack of Universal Testing Standards Causing Procurement Hesitancy

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Type I (Calm Water)

- 5.1.2 Type II (Mild Current)

- 5.1.3 Type III (Strong Current and Offshore)

- 5.2 By Material

- 5.2.1 Polyvinyl Chloride

- 5.2.2 Polyurethane

- 5.2.3 Geotextile Fabric

- 5.2.4 Composite Laminates

- 5.3 By Application

- 5.3.1 Dredging

- 5.3.2 Marine and Coastal Construction

- 5.3.3 Offshore Energy (Oil, Gas, Wind)

- 5.3.4 Environmental Remediation and Habitat Projects

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Australia and New Zealand

- 5.4.1.6 ASEAN Countries

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Turkey

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ABASCO

- 6.4.2 ACME Environmental

- 6.4.3 BMP Supplies Inc.

- 6.4.4 BTL

- 6.4.5 Clarion Municipal

- 6.4.6 Elastec

- 6.4.7 Floatex Srl

- 6.4.8 Gecko Cleantech

- 6.4.9 GEI Works

- 6.4.10 JXY Heavy Industry

- 6.4.11 Layfield Group

- 6.4.12 Silt Management Supplies, LLC.

- 6.4.13 Solmax

- 6.4.14 Texas Boom Company

- 6.4.15 Tritonbuoys

- 6.4.16 Water Pollution Solutions

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment