PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063340

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063340

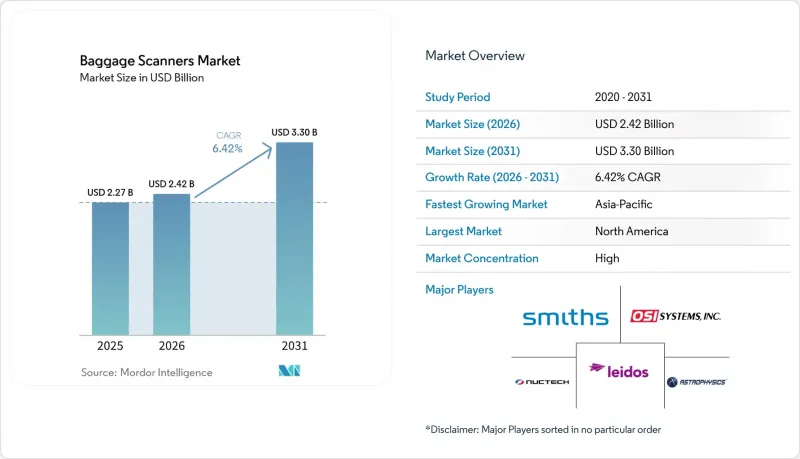

Baggage Scanners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the baggage scanners market size is expected to grow from USD 2.27 billion in 2025 to USD 2.42 billion in 2026 and is forecast to reach USD 3.30 billion by 2031 at 6.42% CAGR over 2026-2031.

This report is Segmented by Technology (X-Ray Single-View, X-Ray Dual-View, Computed Tomography (CT), and More), Scanner Geometry (Less Than 50 Cm Tunnel, 50-100 Cm Tunnel, and More), End-User Industry (Airports, Seaports and Border Crossings, Railway and Metro Stations, and More), Mobility (Fixed Systems, and Portable/Mobile Systems), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Baggage Scanners Market Trends and Insights

Increasing Passenger Throughput At Major Airports

Hub-airport expansion programs are underpinning long-run demand. Dubai International's installation of 140 CT lanes, Mumbai's USD 1 billion Terminal 1 redevelopment, and India's directive for 600 hand-baggage scanners exemplify capacity locks that extend replacement cycles well into the next decade. Mega-projects in Saudi Arabia and the United Arab Emirates embed AI-enabled lanes from day one, giving vendors visibility on multiyear order pipelines.

Mandatory Adoption Of Advanced Imaging Technologies

Regulatory mandates compress adoption curves. The Transportation Security Administration's USD 2.6 billion award to Leidos for 12,000 credential-authentication and explosives-trace units, plus CT lanes, anchors U.S. demand, while the European Civil Aviation Conference Standard 3 positions CT as the de facto cabin-baggage benchmark. Heathrow's GBP 1 billion (USD 1.27 billion) CT retrofit removes the 100 milliliter liquid limit, catalyzing copy-cat projects across European hubs.

High Capital Expenditure And Long Procurement Cycles

CT scanners cost two to three times as much as dual-view units, pushing the return-on-investment horizon farther out for smaller airports. Tender processes in Africa, South America, and secondary Indian metros often exceed 18 months as buyers juggle donor conditions, currency hedges, and local-content clauses, delaying capacity even where throughput is rising.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of E-Commerce Logistics Hubs

- Modernization Of Rail And Metro Stations

- Stringent Data-Privacy Concerns Over 3D Imaging Storage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Computed tomography captured momentum in 2025 and is on track for a 7.85% CAGR during 2026-2031, led by U.S., European, and Gulf regulators permitting passengers to keep electronics and liquids in their bags. The baggage scanners market size for CT platforms is projected to expand sharply as TSA, Heathrow, and Dubai Airports standardize volumetric imaging. Dual-view X-ray systems retained a 43.21% hold because secondary airports, rail stations, and parcel centers value lower capex and established operator familiarity.

Dual-view's entrenched base anchors upgrade services, yet its share erodes where AI engines require richer data streams. Single-view remains confined to mail rooms. Millimeter-wave and terahertz imaging are attracting attention as non-ionizing alternatives compliant with European passenger-screening rules, but component costs and performance standards keep them niche. Smiths Detection's SDX 10080 SCT cargo CT and Leidos-Quadridox diffraction partnership illustrates the race to stretch CT into freight lanes, opening new monetization layers.

Scanners with 50-100 cm openings captured 48.25% share in 2025 due to alignment with International Air Transport Association cabin-bag limits. The baggage scanners market share for mobile cabinet and stand-alone systems will grow rapidly at a 7.70% CAGR, as border posts and event venues prefer compact devices that fit in standard vans. Tunnels less than 50 cm remain relevant for mail and e-commerce parcels, while gantries greater than 100 cm serve seaport and air-freight pallets.

Medium-tunnel CT systems form the heart of TSA's and Heathrow's checkpoint conversions, signaling production scale-up. Mobile cabinets embed AI analytics and can be fielded within hours, extending the vendor's value proposition from hardware to logistics services. Oversized cargo scanners, though lower in unit volume, carry premium pricing tied to container-radiography specifications.

Geography Analysis

North America retained a 32.22% hold in 2025 as the TSA installed 634 CT units and inked a USD 2.6 billion Leidos contract that secures replacement demand through 2033. Canada pilots CT at Toronto Pearson and Vancouver, and U.S. Customs and Border Protection awarded OSI Systems USD 54 million for CertScan drive-through lanes. Mexico, with constrained federal budgets, leans on redeployable portals, giving portable-system vendors an entry point.

Asia-Pacific is the fastest-growing region, with a 7.55% CAGR through 2031. India's Bureau of Civil Aviation Security earmarked INR 1,000 crore (USD 120 million) for 600 baggage units, and metro projects in Delhi, Chennai, and Kolkata specified AI-ready scanners. China's rail upgrades deploy domestic dual-view lines, and Airports Council International surveys indicate CT adoption will double in three years. Southeast Asia and Gulf airports, backed by USD 183 billion in planned capital, further swell the order book.

Europe's CT momentum coexists with stringent privacy mandates that slow the adoption of full-body scanners. Heathrow's GBP 1 billion (USD 1.27 billion) retrofit leads, while smaller states prioritize border-security portals such as Estonia's EUR 3.1 million (USD 3.31 million) Rapiscan Argos. The Middle East channels mega-airport budgets into volumetric imaging, whereas sub-Saharan Africa's capital gaps slow refresh cycles, limiting near-term penetration. South America exhibits episodic buys, typified by Chile's CLP 3.2 billion (USD 3.54 million) Nuctech mobile trailer and Brazil's pilot CT lanes at Guarulhos, where fiscal austerity lengthens tender timelines.

- Smiths Group plc

- OSI Systems Inc.

- Nuctech Company Limited

- Leidos Holdings Inc.

- Astrophysics Inc.

- Gilardoni S.p.A.

- L3Harris Technologies Inc.

- VOTI Detection Inc.

- CEIA SpA

- Teledyne FLIR LLC

- Adani Systems Inc.

- Scanna MSC Ltd.

- Todd Research Ltd.

- Mekitec Group Oy

- Linev Systems US Inc.

- VJ Technologies Inc.

- Westminster Group plc

- Micro-X Limited

- Analogic Corporation

- Optosecurity Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Passenger Throughput at Major Airports

- 4.2.2 Mandatory Adoption of Advanced Imaging Technologies Under Global Aviation Security Norms

- 4.2.3 Expansion of E-Commerce Logistics Hubs Requiring High-Capacity Parcel Scanning

- 4.2.4 Modernization of Rail and Metro Stations in Emerging Economies

- 4.2.5 Integration of Artificial Intelligence for Automated Threat Recognition

- 4.2.6 Rising Deployment of Compact Mobile Scanners for Event Security

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure and Long Procurement Cycles

- 4.3.2 Stringent Data-Privacy Concerns Over 3-D Imaging Storage

- 4.3.3 Limited Infrastructure Funding at Small Regional Airports

- 4.3.4 Supply-Chain Bottlenecks in Specialty X-Ray Components

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 X-ray Single-View

- 5.1.2 X-ray Dual-View

- 5.1.3 Computed Tomography (CT)

- 5.1.4 Millimeter-wave Imaging

- 5.1.5 Terahertz Imaging

- 5.2 By Scanner Geometry

- 5.2.1 Less than 50 cm Tunnel (Small Parcel)

- 5.2.2 50-100 cm Tunnel (Medium Baggage)

- 5.2.3 Greater than 100 cm Tunnel (Large Baggage)

- 5.2.4 Mobile Cabinet / Stand-alone

- 5.3 By End-user Industry

- 5.3.1 Airports

- 5.3.2 Seaports and Border Crossings

- 5.3.3 Railway and Metro Stations

- 5.3.4 Logistics and Parcel Facilities

- 5.3.5 Government Buildings and Courthouses

- 5.3.6 Hotels, Malls and Public Venues

- 5.4 By Mobility

- 5.4.1 Fixed Systems

- 5.4.2 Portable / Mobile Systems

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smiths Group plc

- 6.4.2 OSI Systems Inc.

- 6.4.3 Nuctech Company Limited

- 6.4.4 Leidos Holdings Inc.

- 6.4.5 Astrophysics Inc.

- 6.4.6 Gilardoni S.p.A.

- 6.4.7 L3Harris Technologies Inc.

- 6.4.8 VOTI Detection Inc.

- 6.4.9 CEIA SpA

- 6.4.10 Teledyne FLIR LLC

- 6.4.11 Adani Systems Inc.

- 6.4.12 Scanna MSC Ltd.

- 6.4.13 Todd Research Ltd.

- 6.4.14 Mekitec Group Oy

- 6.4.15 Linev Systems US Inc.

- 6.4.16 VJ Technologies Inc.

- 6.4.17 Westminster Group plc

- 6.4.18 Micro-X Limited

- 6.4.19 Analogic Corporation

- 6.4.20 Optosecurity Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment