PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063397

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063397

Inhalation CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

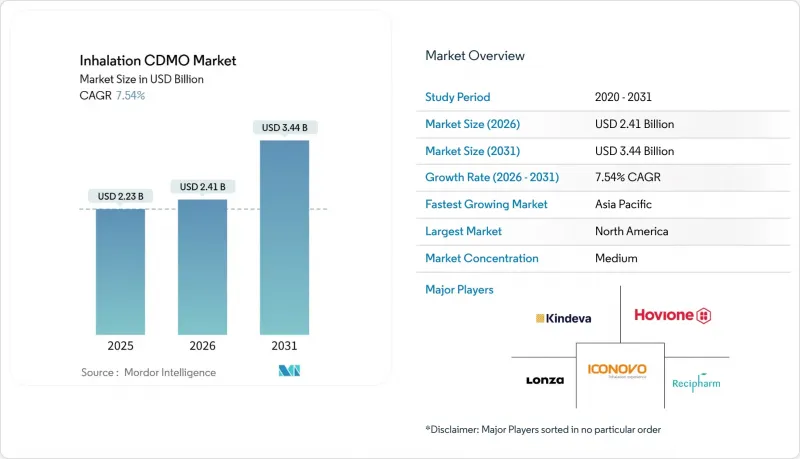

According to Mordor Intelligence, the inhalation cDMO market is expected to grow from USD 2.23 billion in 2025 to USD 2.41 billion in 2026 and is forecasted to reach USD 3.44 billion by 2031 at 7.54% CAGR over 2026-2031.

This report is Segmented by Service Type (Contract Development, Clinical Manufacturing, Commercial Manufacturing, Packaging & Labelling, and Other Services), Product Type (Metered-Dose Inhalers (MDI), Dry-Powder Inhalers (DPI), Nebulized Formulations, and Soft-Mist Inhalers (SMI) & Others), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Inhalation CDMO Market Trends and Insights

Increasing Prevalence of Chronic Respiratory Diseases

WHO's 2024 update recorded 569.2 million prevalent asthma, COPD, and interstitial lung disease cases and 4.2 million related deaths worldwide. Incidence is rising fastest in low-income regions where rapid urbanization degrades air quality, so sponsors are broadening inhaled portfolios beyond bronchodilators into anti-inflammatory biologics and targeted small molecules. CDMOs holding sub-5-micron particle-size capability and high-potency API containment win disproportionate contracts because these exacting specifications exceed many sponsors' internal skill sets. Device penetration remains low in several high-burden countries, indicating underserved demand that could unlock downstream volume as reimbursement schemes mature. Regulators reinforce higher technical standards, which consolidate work among CDMOs with validated analytical methods and multi-jurisdictional dossiers.

Pharmaceutical Outsourcing of Specialized Inhalation Manufacturing

Internal aerosol groups at several large pharmaceutical companies were redeployed toward higher-margin cell and gene therapy programs in 2025, redirecting inhalation budgets to external partners. Maintaining propellant lines, laser-diffraction suites, and aerosol talent for sporadic launches no longer passes internal hurdle rates, especially for mid-sized biotechs. CDMOs in North America and Western Europe capture the bulk of late-stage work because proximity and regulatory familiarity shorten oversight cycles. At the same time, Asia-Pacific providers pick up early-stage studies through cost leadership. Compliance with ISO 13485 and GMP annexes remains the entry ticket, so qualified capacity stays tight, and pricing power remains with established providers.

Stringent, Multi-Region Regulatory Compliance Burden

FDA's 2024 draft guidance layered real-time stability and multi-flow aerodynamic testing across all inhaled products, adding 12-18 months and boosting pre-approval costs by up to 30%. EMA tightened dissolution and pharmacokinetic bridging requirements for device changes, forcing sponsors pursuing global launches to comply with divergent yet overlapping rules. CDMOs maintain parallel quality systems across FDA 21 CFR Part 211, EMA Annex 1, and PMDA, which raise overhead and constrain margins. Smaller providers without dedicated regulatory teams struggle, leading to market consolidation among larger firms that can shoulder evolving compliance demands.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Particle Engineering and Smart Devices

- Growing Adoption of Combination and Smart Inhalers

- High CAPEX for Aerosol Facilities and Clean-Room Integration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, contract development accounted for 37.09% of the inhalation CDMO market revenue, as sponsors prioritized risk reduction during formulation screening and device selection. Clinical manufacturing, however, is registering a 10.23% CAGR to 2031 on the back of an expanding cohort of Phase II and Phase III biologics programs. The inhalation CDMO market size allocated to development services has a higher gross margin profile than routine commercial production, as feasibility studies, analytical method development, and regulatory consulting command 50-60% gross margins.

The inhalation CDMO market sees service-mix value migrating upstream. CDMOs with earlier investments in spray-drying, lyophilization, and single-use bioreactors, such as Lonza, Catalent, and Hovione, capitalize on complex biologic demand. Lower-margin commercial campaigns are increasingly price-pressured by Asian plants offering 20-30% savings, which pushes Western providers to bundle packaging, labeling, and stability into single contracts. Ancillary services, such as post-approval change management, are expanding as sponsors seek to house lifecycle updates with partners who already hold validated dossiers.

Geography Analysis

North America held 44.25% of the inhalation CDMO market revenue in 2025 on the strength of the FDA's streamlined 505(b)(2) pathway, a dense cluster of respiratory biotechs, and mature reimbursement that supports premium triple therapies. Europe remains fragmented yet sizable because EMA's centralized procedure allows multi-country launches. Mexico is emerging as a nearshore commercial hub for Latin American distributors.

Asia-Pacific is projected to post an 11.14% CAGR through 2031, making it the fastest-rising regional contributor to Inhalation CDMO market growth. China's NMPA has accelerated generic inhaler reviews, and India's production-linked incentives now refund up to 8% of incremental sales to qualifying manufacturers. Japan's aging population keeps demand steady, but local sourcing preferences limit foreign CDMO penetration. South Korea and Australia are growing as clinical trial hubs, while the Middle East, Africa, and South America present latent expansion opportunities that hinge on reimbursement modernization and currency stability.

- Aptar

- Arcinova

- Bend Bioscience

- Bespak Limited

- Cambrex

- CordenPharma

- HCmed Innovations Co., Ltd.

- Hovione

- Iconovo

- Kindeva

- Lonza Group

- Nemera

- Novo Holdings A/S (Catalent Inc.)

- Recipharm AB (EQT AB)

- Ritedose

- Sanner GmbH

- Siegfried Holding AG

- Stevanato Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Respiratory Diseases

- 4.2.2 Pharmaceutical Outsourcing of Specialized Inhalation Manufacturing

- 4.2.3 Technological Advances in Particle-Engineering and Smart Devices

- 4.2.4 Growing Adoption of Combination and Smart Inhalers

- 4.2.5 Low-GWP Propellant Transition Favoring Equipped CDMOs

- 4.2.6 Surge in Inhalable Biologics and Peptides Pipelines

- 4.3 Market Restraints

- 4.3.1 Stringent, Multi-Region Regulatory Compliance Burden

- 4.3.2 High CAPEX for Aerosol Facilities and Clean-Room Device Integration

- 4.3.3 Supply Risk for Medical-Grade Propellants During HFC Phase-out

- 4.3.4 Scarcity of Aerosol Characterization Talent and Test Capacity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Contract Development

- 5.1.2 Clinical Manufacturing

- 5.1.3 Commercial Manufacturing

- 5.1.4 Packaging & Labelling

- 5.1.5 Other Services

- 5.2 By Product Type

- 5.2.1 Metered-Dose Inhalers (MDI)

- 5.2.2 Dry-Powder Inhalers (DPI)

- 5.2.3 Nebulized Formulations

- 5.2.4 Soft-Mist Inhalers (SMI) & Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Aptar

- 6.3.2 Arcinova

- 6.3.3 Bend Bioscience

- 6.3.4 Bespak Limited

- 6.3.5 Cambrex Corporation

- 6.3.6 CordenPharma

- 6.3.7 HCmed Innovations Co., Ltd.

- 6.3.8 Hovione

- 6.3.9 Iconovo

- 6.3.10 Kindeva

- 6.3.11 Lonza Group AG

- 6.3.12 Nemera

- 6.3.13 Novo Holdings A/S (Catalent Inc.)

- 6.3.14 Recipharm AB (EQT AB)

- 6.3.15 Ritedose

- 6.3.16 Sanner GmbH

- 6.3.17 Siegfried Holding AG

- 6.3.18 Stevanato Group

- 6.4 Market Opportunities & Future Outlook

- 6.4.1 White-Space & Unmet-Need Assessment