PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063497

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063497

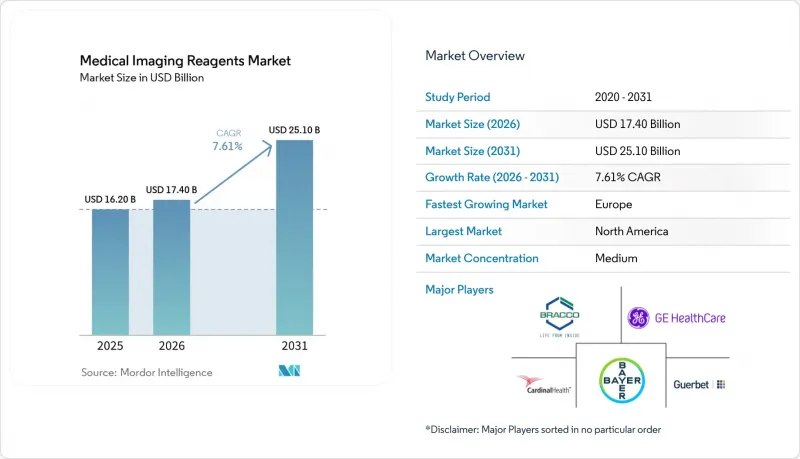

Medical Imaging Reagents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the medical imaging reagents market size is expected to increase from USD 16.20 billion in 2025 to USD 17.40 billion in 2026 and reach USD 25.10 billion by 2031, growing at a CAGR of 7.61% over 2026-2031.

This report is Segmented by Product Type (Contrast Reagents, Radiopharmaceuticals, and More), Modality (X-Ray & CT, MRI, and More), Application (Oncology, Cardiology & Vascular, and More), End User (Hospitals, Diagnostic Imaging Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Medical Imaging Reagents Market Trends and Insights

Rapid Adoption of PSMA-PET Imaging Expanding Tracer Utilization

Ga-68 and F-18 PSMA tracers have moved from niche research tools to mainstream prostate-cancer staging modalities after pivotal trials showed that management changed in 28% of recurrent-disease cases . The U.S. Food and Drug Administration (FDA) cleared Telix's Illuccix in 2024 and broadened Novartis's Pluvicto label in 2025, creating a closed-loop theranostic ecosystem in which PET scans guide lutetium-177 therapy. Revenue from Lantheus's Pylarify hit USD 285 million during the first three quarters of 2024 after Medicare assigned dedicated payment codes that reimburse tracers at rates comparable to fluorodeoxyglucose (FDG). European uptake mirrors the U.S. trajectory; more than 50,000 PSMA-PET scans were logged in Germany in 2025, triple the 2023 volume, after statutory insurers instituted nationwide coverage. Urology groups are therefore investing in on-site cyclotrons and radiopharmacies to secure same-day deliveries, anchoring durable demand for high-specific-activity reagents.

Radiotheranostics Pipeline Boosting Companion Diagnostics

Successes with lutetium-177 therapies have spurred the development of next-generation alpha emitters, such as actinium-225 and lead-212, whose higher linear energy transfer promises deeper tumor control. ITM Isotope Technologies Munich raised EUR 50 million in 2024 to industrialize Ac-225 derived from thorium-229 decay, aiming to produce 10,000 patient doses per year by 2027. Companion diagnostics are compulsory for these trials, making baseline and follow-up PET scans integral to therapeutic approvals under the FDA draft guidance issued in 2025. Vendors have responded by embedding Monte-Carlo dosimetry software directly into hybrid PET/CT consoles, enabling point-of-care absorbed-dose calculations. As a result, diagnostic reagents now function as gatekeepers for trial enrollment, commercial therapy rollout, and payer coverage deliberations.

Iodinated Contrast-Media Supply-Chain Vulnerability

GE HealthCare's 2022-2024 Omnipaque shutdown revealed brittle, single-site manufacturing dependencies that forced hospitals to ration CT studies. Interim American College of Radiology guidelines substituted non-contrast MRI for contrast-enhanced MRI and recommended half-dose protocols, measures that reduced diagnostic confidence and lengthened exam times. Bracco and Guerbet redirected European output to the United States, yet could not entirely bridge the gap. Regulators now require six-month strategic stockpiles and formal risk-management plans, but full compliance will not arrive until 2027. Upstream active-ingredient concentration in China and India remains unresolved, keeping the medical imaging reagents market exposed to geopolitical and pandemic shocks.

Other drivers and restraints analyzed in the detailed report include:

- Asia-Pacific Imaging Capacity Expansion and Access Improvements

- High CT/X-ray Procedure Growth Sustaining Contrast-Media Demand

- GBCA Retention Warnings and EU Linear-Agent Restrictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radiopharmaceuticals are advancing at an 8.05% CAGR, the quickest clip among product classes, as theranostic pathways link diagnostic scans with targeted radionuclide therapy. Contrast reagents nevertheless account for 58.10% of 2025 revenue because iodinated media underpin the bulk of CT procedures, and gadolinium chelates dominate neuro-MRI. Ultrasound microbubble agents occupy a niche in Europe for cardiac perfusion and liver lesion characterization, while optical dyes such as indocyanine green support intraoperative visualization rather than standalone diagnostics.

Within the segment, PSMA tracers illustrate how a single molecule can eclipse legacy agents in value terms: Pylarify booked USD 380 million in 2024 sales after payer coverage expanded, eclipsing several mature contrast lines. New approvals for F-18 flotufolastat are intensifying price competition while lifting aggregate volume. Meanwhile, the fragility of the Tc-99m supply nudges clinicians toward PET alternatives that leverage longer-lived F-18, further tilting demand toward radiopharmaceuticals. As a result, radiopharmaceutical growth continues to outpace the rest of the medical imaging reagents industry.

Hybrid PET/CT, PET/MRI, and SPECT/CT platforms are growing at an 8.10% CAGR, outstripping standalone CT or MRI investment, because they deliver co-registered anatomic and molecular data in a single sitting. X-ray and CT retained a 52.56% share in 2025, thanks to high procedure volumes, but incremental growth is slowing as capital budgets shift toward hybrid scanners.

Total-body PET/CT systems, such as the Biograph Vision Quadra, cover head-to-thigh regions in 3 minutes, enabling dynamic whole-body pharmacokinetics and driving demand for high-specific-activity tracers. PET/MRI remains a premium niche due to price tags of USD 5-7 million and demanding physics, whereas SPECT/CT occupies the value tier for bone scans and sentinel-node mapping. The shift toward hybrid imaging cements a long-term need for both anatomical contrast agents and novel PET isotopes, reinforcing the diversity of the medical imaging reagents market.

Geography Analysis

North America held the largest 39.16% revenue share in 2025, driven by early PSMA-PET and high per-capita imaging. Yet Europe will register the fastest CAGR of 7.93% as regulators subsidize hybrid PET/CT rollouts and enforce macrocyclic gadolinium policies. Germany alone installed more than 200 PET/CT scanners between 2024 and 2025 after nationwide reimbursement began.

Asia-Pacific is bifurcating: high-income city-states mirror Western usage patterns, while emerging economies focus on first-time deployment of modality. China's county-hospital build-out and India's tier-2 PET expansion promise long-run upside but currently trail Europe on per-capita reagent consumption. Middle East & Africa and South America remain import-dependent and vulnerable to currency swings, slowing medical imaging reagents market penetration.

- Ascelia Pharma

- Bayer

- Blue Earth Diagnostics

- Bracco S.p.A

- Cardinal Health

- Curium Pharma

- EczacIbasI Monrol

- FUJIFILM Toyama Chemical

- GE Healthcare

- Guerbet SA

- IRE ELiT

- ITM Isotope Technologies Munich

- Jubilant Radiopharma

- Lantheus

- LI-COR Biosciences

- Nihon Medi-Physics

- NorthStar Medical Radioisotopes

- Novartis

- PharmaLogic

- Revvity

- SOFIE

- Telix Pharmaceuticals

- The Diagnostic Green Company (ICG)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of PSMA PET Imaging Expanding Tracer Utilization

- 4.2.2 Radiotheranostics Pipeline (Lu-177, Alpha-Emitters) Boosting Companion Diagnostics

- 4.2.3 Asia-Pacific Imaging Capacity Expansion and Access Improvements

- 4.2.4 High CT/X-Ray Procedure Growth Sustaining Contrast Media Demand

- 4.2.5 Reimbursement Uplift for High-Cost Diagnostic Radiopharmaceuticals (US OPPS 2025+)

- 4.2.6 Supply Diversification and Reshoring Across Contrast And Isotopes

- 4.3 Market Restraints

- 4.3.1 Iodinated Contrast Media Supply-Chain Vulnerability

- 4.3.2 GBCA Retention Warnings and EU Linear-Agent Restrictions

- 4.3.3 Mo-99/Tc-99m Isotope Supply Fragility

- 4.3.4 Legacy Packaging/Uneven Payer Policies Dampening Diagnostic Radiopharmaceutical Uptake

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Contrast Reagents

- 5.1.2 Radiopharmaceuticals

- 5.1.3 Ultrasound Microbubble Agents

- 5.1.4 Optical Imaging Dyes & Probes

- 5.2 By Modality

- 5.2.1 X-ray & Computed Tomography (CT)

- 5.2.2 Magnetic Resonance Imaging (MRI)

- 5.2.3 Ultrasound (incl. CEUS)

- 5.2.4 Nuclear Imaging (SPECT & PET)

- 5.2.5 Hybrid Modalities (PET/CT, PET/MRI, SPECT/CT)

- 5.3 By Application

- 5.3.1 Oncology

- 5.3.2 Cardiology & Vascular

- 5.3.3 Neurology

- 5.3.4 Gastroenterology & Hepatology

- 5.3.5 Musculoskeletal & Orthopedics

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of MEA

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Ascelia Pharma

- 6.3.2 Bayer AG

- 6.3.3 Blue Earth Diagnostics

- 6.3.4 Bracco S.p.A

- 6.3.5 Cardinal Health

- 6.3.6 Curium Pharma

- 6.3.7 EczacIbasI Monrol

- 6.3.8 FUJIFILM Toyama Chemical

- 6.3.9 GE HealthCare

- 6.3.10 Guerbet SA

- 6.3.11 IRE ELiT

- 6.3.12 ITM Isotope Technologies Munich

- 6.3.13 Jubilant Radiopharma

- 6.3.14 Lantheus

- 6.3.15 LI-COR Biosciences

- 6.3.16 Nihon Medi-Physics

- 6.3.17 NorthStar Medical Radioisotopes

- 6.3.18 Novartis AG

- 6.3.19 PharmaLogic

- 6.3.20 Revvity

- 6.3.21 SOFIE

- 6.3.22 Telix Pharmaceuticals

- 6.3.23 The Diagnostic Green Company (ICG)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment