PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063507

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063507

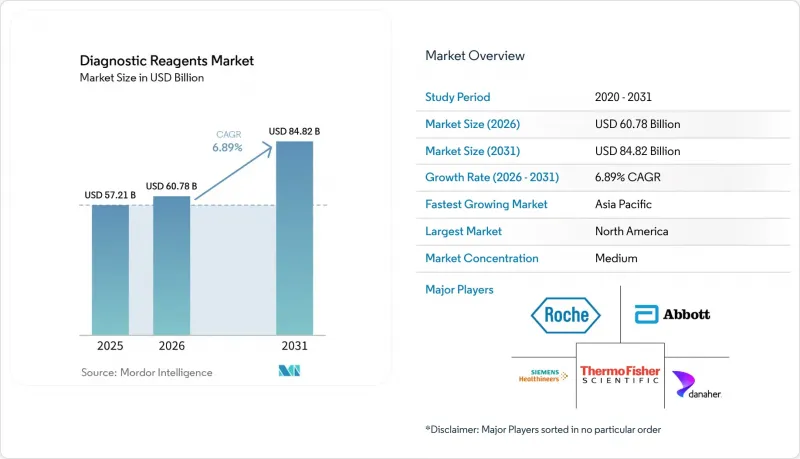

Diagnostic Reagents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the diagnostic reagents market size is expected to increase from USD 57.21 billion in 2025 to USD 60.78 billion in 2026 and reach USD 84.82 billion by 2031, growing at a CAGR of 6.89% over 2026-2031.

This report is Segmented by Technology (Immunoassay, Clinical Chemistry, Molecular Diagnostics, Hematology, Microbiology, Rapid Tests, IHC/ISH, and More), Application (Infectious Diseases, Oncology, Cardiology, and More), End User (Hospital Laboratories, Independent/Reference Laboratories, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts are in Value (USD).

Global Diagnostic Reagents Market Trends and Insights

Aging Population And Chronic Disease Burden Elevate Routine Diagnostics Demand

Demographic aging increases the baseline rate of routine panels for cardiometabolic, oncology, and infectious conditions, which stabilizes recurring test volumes for laboratories and hospital networks. Chronic patients revisit testing on defined clinical intervals, which converts installed analyzers into predictable reagent annuities that cushion revenue variability across seasons. In the diagnostic reagents market, this steady cadence pairs with aligned Medicare fee schedule updates that shape the timing and pricing of run-rate testing across providers. Reagent throughput in high-volume labs benefits from new automated units that lift test density and reduce manual interventions while upholding quality controls.

That same dynamic supports integrated delivery networks that look to consolidate platforms and standardize assay menus for clinical chemistry, immunoassay, and specialized testing. As a result, the diagnostic reagents market sees a consistent mix of hospital, reference lab, and physician office demand anchored by chronic care pathways.

Shift To Point Of Care And Decentralized Testing Accelerates Reagent Throughput

Over-the-counter and CLIA-waived rapid tests continue to migrate testing closer to patients, which raises utilization and changes packaging economics for reagents. The Flowflex Plus 4 in 1 home test for RSV, influenza A and B, and COVID illustrates this shift by delivering a four-target result in minutes without instrumentation, which expands consumer access and supports faster clinical decisions in primary care follow-up.

To supply these decentralized channels at scale, manufacturers are adopting lyophilized or air-dried chemistries that maintain stability at ambient conditions, cutting cold-chain dependence and reducing transport waste. These formats are now table stakes in the diagnostic reagents market, especially as retailers and telehealth models integrate self-collection and home testing into episodic care pathways. Packaging shifts from bottles to single-use cartridges or cassettes increase unit costs, yet they open new distribution lanes such as pharmacy shelves and mail-order fulfillment that lift total test counts.

As decentralized programs scale, vendors that prove reliability in ambient-stable formats capture recurring demand that is less exposed to hospital procurement cycles.

EU IVDR Compliance Burden And Notified Body Bottlenecks Delay Launches, Raise Costs

The IVDR transition requires expanded clinical evidence, unique device identification, and deeper post-market surveillance, which lift documentation and audit workloads for manufacturers. Industry surveys from European trade bodies and professional associations show companies have slowed or deferred EU launches while prioritizing faster review markets, underscoring ongoing Notified Body capacity constraints.

Labs that relied on laboratory-developed tests face stricter conditions under Article 5(5), pushing many to adopt manufacturer-supplied kits that meet IVDR requirements. For reagent makers, IVDR adds time and cost to product lifecycles, which can alter the European launch queue and drive global sequencing trade-offs. This dynamic favors vertically integrated platforms with internal regulatory teams and established QMS maturity that can manage multi-year projects with predictable cadence. The diagnostic reagents market therefore experiences a temporary slowdown in EU rollouts while U.S. and other markets absorb earlier releases.

Other drivers and restraints analyzed in the detailed report include:

- Molecular (PCR/dPCR/NGS) Adoption Expands High Value Assay Pull Through

- Core Lab Consolidation And Total Lab Automation Increase Consumables Velocity

- Reimbursement Cuts And Centralized Tenders Compress Prices And Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Immunoassay and immunochemistry reagents captured 30.29% of 2025 revenue within the diagnostic reagents market, supported by high-frequency testing across hospital networks that run large, integrated analyzers. In parallel, molecular diagnostics reagents spanning PCR, dPCR, and NGS are projected to post an 8.13% CAGR through 2031, lifted by oncology, infectious disease, and pharmacogenomic applications that create durable test menus. Systems-level upgrades on integrated chemistry platforms increase test density, raise uptime, and improve reagent pack efficiency, which accelerates pull-through in consolidated labs.

Automation layers that speed pre-analytical handling further support uninterrupted workflows in metro hubs that process high tube volumes per hour. Vendors that match analyzer throughput with stable, onboard-compatible formulations capture sole-source contracts that secure multi-year annuities, which is a defining feature of the diagnostic reagents market. Menu consolidation also continues in blood safety, where new donor screening assays combine multiple viral targets to reduce per-sample handling and lift per-run value.

Across the diagnostic reagents industry, decentralized rapid tests expand access and shift packaging from bulk bottles to single-use cassettes that preserve shelf life and support mass distribution through retail and home channels. This shift relies on lyophilized or air-dried chemistries that reduce cold-chain burdens and keep unit performance stable under variable transport conditions. Open-platform chemistries in clinical chemistry and hematology remain vital for routine labs, but competitive intensity and procurement consolidation put pressure on prices as labs standardize menus and leverage higher volumes.

Specialty segments such as tissue and cell-based assays keep pace as companion diagnostics expand into new indications, reinforcing the role of regulated kits that meet quality system and evidence requirements. As fleets modernize, buyers value analyzers with automated calibration cycles and predictive maintenance, which extends run time and reduces waste linked to repeat QC. This setup creates a path for vendors that balance equipment innovation with reliable reagent packs to protect share in the diagnostic reagents market.

Geography Analysis

North America held a 41.37% share of diagnostic reagents market size in 2025, supported by strong payer coverage for high-acuity testing, companion diagnostics integration, and IDN consolidation that standardizes analyzer fleets. Medicare fee schedule and laboratory fee updates influence price realization and test utilization, which labs manage through automation and throughput gains that lower per-test costs. The throughput uplift seen with next-generation analytical units supports consolidated sites that run continuous operations and schedule maintenance around predictable workloads.

Europe remains a large installed base with steady demand, but IVDR-related workload and Notified Body capacity constraints have extended certification timelines and altered launch sequencing for many companies. Surveys from professional associations and industry groups indicate that firms have reframed European pipelines to prioritize products with available review capacity, which has reduced the pace of some EU introductions. Article 5(5) implications have also pushed some labs to reduce reliance on LDTs and adopt manufacturer kits that meet IVDR requirements.

Asia-Pacific is projected to grow at a 9.13% CAGR to 2031 in the diagnostic reagents market, with urban centers expanding core-lab capacity and decentralized channels improving access in community settings. In several countries, centralized procurement programs and local manufacturing push drive pricing discipline and faster access to high-volume tests. Tender structures and local content preferences influence supplier selection, which helps domestic firms gain share in closed-system analyzers. International suppliers strengthen positions by pairing menu breadth with localized service, training, and supply chain flexibility.

- Abbott Laboratories

- Agilent (Dako)

- Beckton Dickinson

- bioMerieux

- Bio-Rad Laboratories

- Danaher (Beckman Coulter

- Cepheid)

- DiaSorin

- DiaSys Diagnostic Systems

- F. Hoffmann-La Roche (Roche Diagnostics)

- Hologic

- Meridian Bioscience

- QIAGEN

- QuidelOrtho

- Randox Laboratories

- Revvity (Euroimmun)

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

- Werfen

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging population and chronic disease burden elevate routine diagnostics demand

- 4.2.2 Shift to point-of-care and decentralized testing accelerates reagent throughput

- 4.2.3 Molecular (PCR/dPCR/NGS) adoption expands high-value assay pull-through

- 4.2.4 Core-lab consolidation and total lab automation increase consumables velocity

- 4.2.5 Lyophilized/ambient-stable formats reduce cold-chain costs and enable distributed sites

- 4.2.6 OEM/contract manufacturing of reagents speeds launches and scales capacity

- 4.3 Market Restraints

- 4.3.1 EU IVDR compliance burden and Notified Body bottlenecks delay launches, raise costs

- 4.3.2 Reimbursement cuts and China's VBP/centralized tenders compress prices and margins

- 4.3.3 Fragmented reimbursement and coding slow clinical adoption and scale-up

- 4.3.4 Raw-material scarcity and lot-to-lot variability drive QC bridging and validation overhead

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Immunoassay/Immunochemistry

- 5.1.2 Clinical Chemistry

- 5.1.3 Molecular Diagnostics (PCR, dPCR, NGS)

- 5.1.4 Hematology

- 5.1.5 Coagulation

- 5.1.6 Microbiology (ID/AST)

- 5.1.7 Urinalysis

- 5.1.8 Rapid Tests (Lateral Flow/POC)

- 5.1.9 Tissue & Cell-based (IHC/ISH)

- 5.2 By Application

- 5.2.1 Infectious Diseases

- 5.2.2 Oncology

- 5.2.3 Cardiology

- 5.2.4 Endocrinology/Diabetes

- 5.2.5 Autoimmune & Inflammation

- 5.2.6 Nephrology & Liver Function

- 5.2.7 Women's Health & Prenatal/STD

- 5.3 By End User

- 5.3.1 Hospital Laboratories

- 5.3.2 Independent/Reference Laboratories

- 5.3.3 Point-of-Care/Physician Offices/Urgent Care

- 5.3.4 Homecare/Self-testing

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abbott Diagnostics

- 6.3.2 Agilent (Dako)

- 6.3.3 Becton, Dickinson and Company (BD)

- 6.3.4 bioMerieux

- 6.3.5 Bio-Rad Laboratories

- 6.3.6 Danaher (Beckman Coulter; Cepheid)

- 6.3.7 DiaSorin

- 6.3.8 DiaSys Diagnostic Systems

- 6.3.9 F. Hoffmann-La Roche (Roche Diagnostics)

- 6.3.10 Hologic

- 6.3.11 Meridian Bioscience

- 6.3.12 QIAGEN

- 6.3.13 QuidelOrtho

- 6.3.14 Randox Laboratories

- 6.3.15 Revvity (Euroimmun)

- 6.3.16 Siemens Healthineers

- 6.3.17 Sysmex

- 6.3.18 Thermo Fisher Scientific

- 6.3.19 Werfen

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment