PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063549

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063549

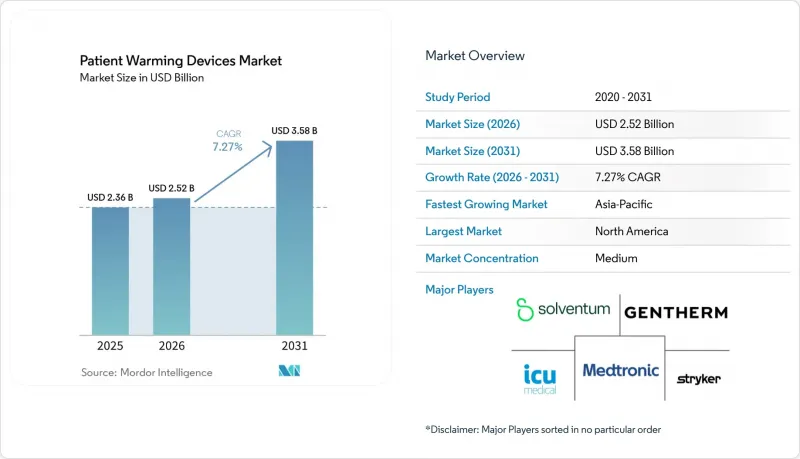

Patient Warming Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the patient warming devices market size is expected to increase from USD 2.36 billion in 2025 to USD 2.52 billion in 2026 and reach USD 3.58 billion by 2031, growing at a CAGR of 7.27% over 2026-2031.

This report is Segmented by Product/Technology (Convective/Forced-air, Conductive/Resistive, Blood & IV Fluid Warmers, and More), Application (Preoperative, Intraoperative, Postoperative, Prehospital/EMS), End User (Hospitals, Ascs, Specialty Clinics, EMS/Military), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Value (USD).

Global Patient Warming Devices Market Trends and Insights

Surgical Volumes and Aging Population Expand Perioperative Warming Demand

China surpassed 210 million citizens aged 65 and older in 2025, a demographic tipping point that, combined with steadily rising minimally invasive procedures, is lifting procedure counts across orthopedics, cardiovascular surgery, and oncology. Elderly patients exhibit impaired thermoregulation, making active warming integral to surgical safety pathways. A 2025 Anesthesiology network meta-analysis confirmed that forced-air blankets heated to 40 °C or higher produced the greatest core-temperature gains in patients over 65. Outcome-based payment models now penalize hypothermia-linked complications, embedding warming devices into essential capital budgets and expanding the patient warming devices market footprint.

Stricter Perioperative Normothermia Guidelines Institutionalize Active Warming

The Association of Perioperative Registered Nurses mandated 30 minutes of prewarming, continuous intra-operative warming, and post-operative monitoring until 36 °C in its 2025 update. Complementary WHO evidence showed a 67% reduction in surgical-site infection when active warming is used over passive insulation. These mandates cascade into accreditation standards and value-based purchasing, making temperature management systems non-negotiable in procurement scoring.

Ongoing FAW Contamination Debate in Laminar-Flow ORs Slows Some Purchases

A 2024 Journal of Hospital Infection study reported that poorly positioned forced-air hoses disrupted ISO 5 airflow and raised particle counts in orthopedic theatres. Despite AORN guidance on correct hose placement, some implant centers pre-emptively switch to conductive or resistive systems, elongating purchase cycles for standard forced-air units.

Other drivers and restraints analyzed in the detailed report include:

- ASC Migration and Same-Day Surgery Protocols Elevate Warming Utilization

- Product Innovation in Convective, Conductive and Fluid Warming Broadens Use Cases

- Burn/Thermal Injury and Misuse Risks Necessitate Training and Limit Protocols

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blood and IV fluid warmers are expanding at an 8.45% CAGR through 2031, outstripping the overall patient warming devices market. In 2025, convective systems still captured 48.90% of revenue, yet rapid-flow fluid devices capable of 41 °C output at 500 mL per minute are becoming standard in U.S. Level I trauma centers. QinFlow's Warrior AC Station exemplifies this, penetrating emergency and military segments not previously served by cabinet-based heaters. On the sustainability front, a 2025 BMJ Open review found 83% of lifecycle analyses favored reusable blankets, positioning conductive and resistive technologies to erode forced-air share over the forecast horizon.

Water-circulating systems remain a niche for cardiac procedures that demand precise temperature control, but their bulky footprints deter ASC adoption. Accessories and disposables principally single-use forced-air blankets face headwinds from EU recyclability rules, prompting Solventum's 2025 move to embed temperature sensors that may revive forced-air growth by mitigating burn risk. The patient warming devices market size for fluid warmers is therefore positioned for the fastest absolute dollar gains through 2031.

Geography Analysis

North America delivered 45.90% of 2025 revenue, buoyed by CMS ASC incentives and the embedding of AORN normothermia metrics into reimbursement frameworks. MedPAC counted 6,308 Medicare-certified ASCs by 2023, with 39 additional centers opening in Q1 2026, reinforcing structural growth. Canada and Mexico remain smaller in absolute terms but benefit from regulatory harmonization under USMCA, which expedites FDA-cleared device entry.

Asia-Pacific is projected to grow at 8.83% into 2031 as China's 210 million-strong senior population boosts surgical demand and governments impose localization quotas that favor domestic suppliers. India's Production-Linked Incentive scheme and Indonesia's 50% domestic content rule are catalyzing regional assembly, while Southeast Asia enjoys 6-10% annual healthcare-spending growth. High per-capita penetration in Japan and South Korea tempers incremental gains but sustains replacement demand.

Europe's trajectory is moderated by MDR certification delays and stringent recyclability mandates under Packaging Regulation 2025/40. The U.K. NHS pledge to cut emissions 80% by 2032 is pivoting purchasing toward reusable resistive pads, accelerating supplier transitions away from single-use forced-air blankets. Middle East growth is concentrated in Gulf Cooperation Council states upgrading surgical infrastructure for medical tourism, while currency volatility continues to weigh on South America, limiting near-term patient warming devices market penetration.

- Augustine Surgical

- Barkey

- Belmont Medical Technologies

- Biegler

- Blickman

- Enthermics Medical Systems

- Gentherm

- ICU Medical

- Medtronic

- MEQU

- Pedigo Products

- Quality In Flow Ltd.

- Skytron

- Solventum

- STERIS

- Stryker

- The Surgical Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surgical Volumes and Aging Population Expand Perioperative Warming Demand

- 4.2.2 Stricter Perioperative Normothermia Guidelines Institutionalize Active Warming

- 4.2.3 ASC Migration and Same-Day Surgery Protocols Elevate Warming Utilization

- 4.2.4 Product Innovation in Convective, Conductive, And Fluid Warming Broadens Use Cases

- 4.2.5 Sustainability-Driven Shift Toward Lower-Waste, Reusable/Resistive Solutions

- 4.2.6 Prehospital And Military Adoption of Portable Fluid/Patient Warmers Accelerates Uptake

- 4.3 Market Restraints

- 4.3.1 Ongoing FAW Contamination Debate in Laminar-Flow Ors Slows Some Purchases

- 4.3.2 Burn/Thermal Injury and Misuse Risks Necessitate Training and Limit Protocols

- 4.3.3 Lifecycle Cost Pressures and Waste Fees Constrain Disposable Blanket Adoption

- 4.3.4 Procurement Decarbonization Targets Restrict High-Waste Single-Use Portfolios

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product/Technology

- 5.1.1 Convective/Forced-air warming systems

- 5.1.2 Conductive fabric/resistive warming systems

- 5.1.3 Blood & IV fluid warmers

- 5.1.4 Water-circulating systems and garments

- 5.1.5 Warming cabinets

- 5.1.6 Accessories & disposables

- 5.2 By Application

- 5.2.1 Preoperative warming

- 5.2.2 Intraoperative warming

- 5.2.3 Postoperative/PACU warming

- 5.2.4 Prehospital/EMS & transport warming

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers (ASCs)

- 5.3.3 Specialty Clinics

- 5.3.4 EMS/Military & Transport Care

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Augustine Surgical

- 6.3.2 Barkey GmbH & Co. KG

- 6.3.3 Belmont Medical Technologies

- 6.3.4 Biegler GmbH

- 6.3.5 Blickman

- 6.3.6 Enthermics Medical Systems

- 6.3.7 Gentherm

- 6.3.8 ICU Medical

- 6.3.9 Medtronic Plc

- 6.3.10 MEQU

- 6.3.11 Pedigo Products

- 6.3.12 Quality In Flow Ltd.

- 6.3.13 Skytron

- 6.3.14 Solventum

- 6.3.15 STERIS

- 6.3.16 Stryker Corporation

- 6.3.17 The Surgical Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment