PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065539

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065539

United States Patient Temperature Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

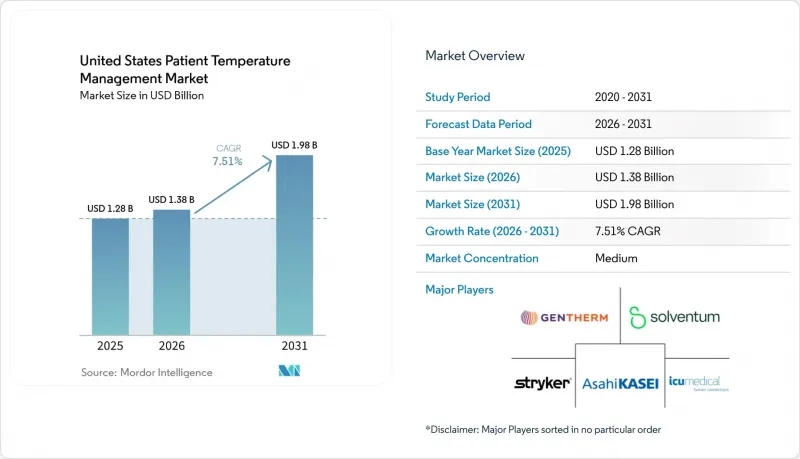

According to Mordor Intelligence, the united states patient temperature management market size was valued at USD 1.28 billion in 2025 and is estimated to grow from USD 1.38 billion in 2026 to reach USD 1.98 billion by 2031, at a CAGR of 7.51% during the forecast period (2026-2031).

This report is Segmented by Product Type (Patient Warming Systems, Patient Cooling Systems, Accessories & Disposables), Application (Perioperative Care, Cardiac Arrest and Critical Care, Neurology and Neurocritical Care, and More), and End User (Hospitals, Ambulatory Surgical Centers, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Patient Temperature Management Market Trends and Insights

Rising Surgical Volumes And Perioperative Normothermia Protocols

The US patient temperature management market is seeing broad support from rising surgical activity in outpatient settings, where portable and rapid-cycle warming systems are easier to deploy than fixed hospital-style equipment. Outpatient facilities now handle more than 80% of surgical procedures in the United States, which has shifted a larger share of device demand toward smaller footprints and faster room turnover. MedPAC reported that ASC procedure volume per Medicare beneficiary grew 3.4% in 2024, which was well above the 2019-2023 average annual rate of 1.0%. That migration is changing procurement behavior because many ASC locations now weigh per-case cost and operational simplicity more heavily than feature density. AORN reported in 2025 that 90.35% of outpatient facility respondents used forced-air warming systems, which shows how deeply warming devices are embedded in perioperative workflows even amid litigation noise. The US patient temperature management market is also gaining from stronger compliance pressure around perioperative temperature control, which supports recurring disposable demand as much as capital equipment placement.

Higher Cardiac-Arrest And Neurocritical-Care Temperature-Control Use

The US patient temperature management market is also being lifted by updated post-resuscitation guidance that requires active fever prevention after cardiac arrest rather than simple observation. The 2025 American Heart Association guidance recommends preventing fever at or below 37.5°C for at least 72 hours in adults who remain comatose after return of spontaneous circulation. European guidance published in Intensive Care Medicine in 2025 aligns with that approach, which keeps device demand intact even as the clinical focus shifts away from routine deep hypothermia. In neurocritical care, updated consensus recommendations continue to favor automated feedback-controlled temperature management for intracerebral hemorrhage, subarachnoid hemorrhage, and acute ischemic stroke patients who require ICU admission. Severe traumatic brain injury care is following the same pattern, with controlled normothermia recognized as a therapeutic option in advanced ICU protocols. This widens the addressable pool for the US patient temperature management market beyond surgical warming and ties growth more closely to critical care pathways.

High Capital And Disposable Costs

Capital intensity remains a real brake on the US patient temperature management market, especially for dual-mode and closed-loop platforms that require a larger up-front commitment. Smaller hospitals and independent ASCs have to balance those capital costs against narrower budgets and lower qualifying case volumes. The burden does not stop at the controller because intravascular catheters, gel pads, warming blankets, and fluid-warming sets create recurring spend with every case. That pressure is harder to absorb when facilities are paid through bundled outpatient structures instead of separate reimbursement for temperature-control products. Independent ASC operators are especially price sensitive, which often pushes them toward single-vendor disposable contracts and slows adoption of newer systems from smaller suppliers. Leasing and subscription models help in some cases, but uptake has been uneven, so cost remains a clear restraint on the US patient temperature management market.

Other drivers and restraints analyzed in the detailed report include:

- Closed-Loop And Dual-Mode Platform Upgrades

- NICU Thermoregulation Monitoring Upgrades

- Recalls And Fluid-Warmer Safety Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Patient Warming Systems held 62.31% of the US patient temperature management market share in 2025, and the segment is also projected to grow at an 8.38% CAGR through 2031. That combination shows that warming remains the operational backbone of the US patient temperature management market across perioperative care, critical care, and neonatal use. The installed base is expanding in 2 ways at the same time, with higher disposable pull-through at existing accounts and new placements in ASCs and specialty clinics. Forced-air warming remains the most common modality by installed base, supported by the 2025 AORN survey showing use in 90.35% of outpatient facilities. Conductive and resistive warming systems are also gaining traction where infection-control concerns are changing preference in orthopedic operating rooms, and a 2026 study in Scientific Reports found conductive warming could achieve outcomes comparable to forced-air warming when pre-warming was used.

Blood and IV-fluid warmers continue to serve a separate but important role in delivering normothermic fluids to hemorrhage and hypothermia-risk patients. That niche is supported by military trauma guidance that specifies warmed blood products at 38-42°C in battlefield and prehospital resuscitation scenarios. Neonatal warmers and hybrid incubator-warmer platforms are also benefiting from the broader NICU quality push, which is expanding the US patient temperature management industry into more integrated thermoregulation workflows. On the cooling side, patient cooling systems remain smaller by revenue, but they are gaining value in cardiac arrest and neurocritical care because precision servo-control and multimodality treatment are becoming more important in ICU practice.

List of Companies Covered in this Report:

- Augustine Surgical

- AVAcore Technologies, Inc.

- Barkey

- Beckton Dickinson

- Belmont Medical Technologies

- Cincinnati Sub-Zero Products (Gentherm legacy brand)

- Dragerwerk

- Enthermics Medical Systems

- Gentherm

- Inspiration Healthcare Group plc

- Medline Industries

- Medtronic

- QinFlow, Inc.

- Smiths Group

- Solventum Corporation

- Stryker

- TSC Life

- ZOLL Medical Corporation (Asahi Kasei Corporation)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Surgical Volumes and Perioperative Normothermia Protocols

- 4.2.2 Higher Cardiac-Arrest and Neurocritical-Care Temperature-Control Use

- 4.2.3 Closed-Loop and Dual-Mode Platform Upgrades

- 4.2.4 NICU Thermoregulation Monitoring Upgrades

- 4.2.5 ASC Migration Favoring Compact Rapid-Turnover Warming Workflows

- 4.2.6 Portable Blood and Fluid Warming in EMS and Military Transport

- 4.3 Market Restraints

- 4.3.1 High Capital and Disposable Costs

- 4.3.2 Recalls and Fluid-Warmer Safety Risks

- 4.3.3 Forced-Air Infection-Control Litigation in Implant-Heavy ORs

- 4.3.4 Legacy Controller Footprints and Service Complexity

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Patient Warming Systems

- 5.1.1.1 Forced-air Warming Systems

- 5.1.1.2 Conductive and Resistive Warming Systems

- 5.1.1.3 Blood and IV-Fluid Warmers

- 5.1.1.4 Neonatal Warmers and Hybrid Incubator-Warmer Platforms

- 5.1.1.5 Integrated Table-based and Dual-mode Warming Systems

- 5.1.2 Patient Cooling Systems

- 5.1.2.1 Surface Cooling Systems

- 5.1.2.2 Intravascular Cooling Systems

- 5.1.2.3 Selective and Targeted Cooling Systems

- 5.1.3 Accessories & Disposables

- 5.1.1 Patient Warming Systems

- 5.2 By Application

- 5.2.1 Perioperative Care

- 5.2.2 Cardiac Arrest and Critical Care

- 5.2.3 Neurology and Neurocritical Care

- 5.2.4 Neonatal and Pediatric Care

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics

- 5.3.4 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Augustine Surgical

- 6.3.2 AVAcore Technologies, Inc.

- 6.3.3 Barkey GmbH & Co. KG

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Belmont Medical Technologies

- 6.3.6 Cincinnati Sub-Zero Products (Gentherm legacy brand)

- 6.3.7 Dragerwerk AG & Co. KGaA

- 6.3.8 Enthermics Medical Systems

- 6.3.9 Gentherm Incorporated

- 6.3.10 Inspiration Healthcare Group plc

- 6.3.11 Medline Industries, LP

- 6.3.12 Medtronic plc

- 6.3.13 QinFlow, Inc.

- 6.3.14 Smiths Medical (ICU Medical)

- 6.3.15 Solventum Corporation

- 6.3.16 Stryker Corporation

- 6.3.17 TSC Life

- 6.3.18 ZOLL Medical Corporation (Asahi Kasei Corporation)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment