PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063583

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063583

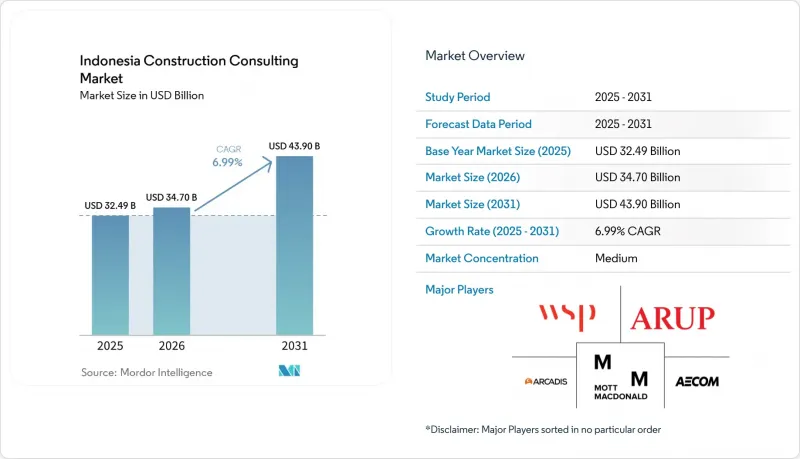

Indonesia Construction Consulting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the indonesia construction consulting market size was valued at USD 32.49 billion in 2025 and is estimated to grow from USD 34.70 billion in 2026 to reach USD 43.90 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031).

This report is Segmented by Service Type (Project Management Consultancy, Feasibility Studies, DPR, Design & Engineering, Master Planning), by Sector (Residential, Commercial, Infrastructure), by Construction Type (New, Renovation), by Investment Source (Public, Private), and by Key Regions (Java, Sumatra, Kalimantan, Sulawesi, Others). Market Forecasts are Provided in Terms of Value (USD).

Indonesia Construction Consulting Market Trends and Insights

Nusantara new-capital megaproject fuelling multi-phase consulting demand

Parliament cleared over 20 Phase II packages across legislative and judicial zones, each valued between USD 760 million and USD 1.27 billion, with completion targeted by 2028. This pipeline guarantees a steady flow of feasibility, detailed design, and project-management contracts even if broader infrastructure budgets soften. The government's mix of direct budget allocations and PPP tranches, USD 3.8 billion to USD 8.2 billion, calls for advisors able to structure risk-sharing agreements. A grant of USD 2.49 million from the U.S. Trade and Development Agency for smart-city studies signals that multilateral sponsors now bake digital-technology requirements into terms of reference, raising capability thresholds for local firms. Because roll-out runs through 2028, Nusantara acts as a counter-cyclical anchor that cushions the Indonesian construction consulting market against spending swings elsewhere.

Building Information Modeling (BIM) and Sistem Pemerintahan Berbasis Elektronik (SPBE) Digital Mandates

Since 2025, state buildings larger than 2,000 m2 and complex infrastructure must use BIM, yet only about one engineer in twenty holds accredited training. Software subscriptions of roughly USD 3,000 per seat match a junior salary, deterring small players. The 2025 SPBE, Electronic-Based Government System regulation now obliges electronic dashboards for real-time cost and schedule tracking, making 4D and 5D integration a de facto requirement. Firms that embraced BIM report tangible savings; pipe waste on the Sepaku water network fell from 3.0% to 1.2%, while laggards risk exclusion from high-profile tenders. Absent a national subsidy, larger enterprises with in-house academies are widening the skills gap.

Lowest-cost (Harga Terendah) tendering bias reducing value-added consulting scope

Most public tenders still hinge on the lowest price, relegating technical quality to a pass-fail filter. This structure compresses fees, discourages investment in BIM or value engineering, and forces mid-sized domestic consultancies into a race to the bottom. Provincial agencies rarely deploy quality-based selection because evaluators lack the capacity to score technical proposals, further entrenching price-only awards. Larger state-owned and foreign firms cope by cross-subsidizing thin-margin studies with higher-margin supervision mandates, but smaller outfits are squeezed, limiting overall innovation in the Indonesia construction consulting market.

Other drivers and restraints analyzed in the detailed report include:

- Public-Private Partnership (PPP) & Sovereign-Fund Co-Investment

- Mandatory AMDAL EIA & PROPER ESG ratings tightening pre-construction due-diligence

- Payment delays & State-Owned Enterprise (SOE) debt overhang squeezing consultant cash-flows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Project management consultancy controlled 54.33% of 2025 revenue, reflecting Indonesia's construction consulting market size leadership in large toll-road and mass-transit programs. Design-and-engineering, however, is forecast to post the quickest expansion at 8.95% CAGR, buoyed by multi-disciplinary scope on Nusantara's judicial and legislative compounds and by complex process-plant layouts in Sulawesi's nickel-EV hubs. Master planning remains a small but strategic niche, especially for new industrial estates that require phasing and utility optimization.

BIM rules are redrawing the competitive map. Only three in ten firms now deliver full 3D-to-5D workflows, and they command premiums of up to 20% over 2D rivals. Foreign players leverage proprietary common-data environments and larger training budgets, while several domestic leaders have responded by launching in-house academies to certify staff and preserve share. As a result, the Indonesia construction consulting market size for high-end design is expanding faster than the overall sector value.

Infrastructure represented 58.55% of 2025 billings, anchored by roads, rail, and water schemes. Nevertheless, commercial assignments are expected to rise at an 8.11% CAGR, topping the sector growth chart. Hyperscale data centers, such as a USD 4.5 billion 500 MW campus outside Jakarta, need specialized MEP, seismic isolation, and liquid-cooling expertise, lifting average fee multipliers.

Office and retail refurbishments add a parallel revenue stream as 2 million m2 of idle 2010s-era space seeks energy-efficient retrofits. Meanwhile, industrial logistics parks benefit from e-commerce tailwinds and regional supply-chain shifts. Within infrastructure, new mandates for climate-resilient drainage and multi-lane free-flow tolling expand the scope for advisory services beyond civil works. Collectively, these trends reinforce commercial momentum but keep infrastructure as the revenue anchor of the Indonesia construction consulting market.

List of Companies Covered in this Report:

- AECOM Indonesia

- Arcadis Indonesia

- WSP Indonesia

- Mott MacDonald Indonesia

- Arup Indonesia

- Jacobs Indonesia

- Stantec Indonesia

- SMEC (Surbana Jurong) Indonesia

- TYPSA Indonesia

- PT Wiratman & Associates

- PT Yodya Karya (Persero) Tbk

- PT Bina Karya (Persero) Tbk

- PT Virama Karya (Persero) Tbk

- PT Indra Karya (Persero) Tbk

- PT Indicon Consultant

- PT Rekayasa Engineering

- PT Saka Energi Consult

- PT Nindya Karya (Engineering & Consultants)

- Nippon Koei Indonesia

- Oriental Consultants Global Indonesia

- Witteveen+Bos Indonesia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Nusantara new-capital megaproject fuelling multi-phase consulting demand

- 4.2.2 Mandatory AMDAL EIA & PROPER ESG ratings tightening pre-construction due-diligence

- 4.2.3 BIM & SPBE digital-construction mandates accelerating digital PMC uptake

- 4.2.4 KPBU PPP reforms & INA sovereign-fund de-risking raising transaction-advisory needs

- 4.2.5 Down-stream nickel-EV industrial parks in Sulawesi spurring specialised infrastructure advisory

- 4.2.6 Green-building (EDGE/Greenship) certification uptake boosting sustainability consulting

- 4.3 Market Restraints

- 4.3.1 Lowest-cost (Harga Terendah) tendering bias reducing value-added consulting scope

- 4.3.2 Payment delays & SOE debt overhang squeezing consultant cash-flows

- 4.3.3 Shortage of certified BIM/PMP professionals constraining capacity

- 4.3.4 Fragmented central-local approvals causing project slippages

- 4.4 Government Initiatives & Consultant Empanelment Frameworks

- 4.5 Value / Supply-Chain Analysis

- 4.5.1 Overview

- 4.5.2 International Consulting Firms - Key Quantitative & Qualitative Insights

- 4.5.3 Domestic/Regional Consulting Firms - Key Quantitative & Qualitative Insights

- 4.5.4 Specialised Niche Consultants - Key Quantitative & Qualitative Insights

- 4.5.5 Technology Platform Providers (BIM, Digital PMC) - Key Quantitative & Qualitative Insights

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Industry Attractiveness - Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Comparison of Consulting-Market Maturity: Indonesia vs. Other ASEAN Countries

5 Market Size & Growth Forecasts (Value, in USD Billion)

- 5.1 By Service Type

- 5.1.1 Project Management Consultancy (PMC)

- 5.1.2 Feasibility Studies

- 5.1.3 Detailed Project Reports (DPR)

- 5.1.4 Design & Engineering Services

- 5.1.5 Master Planning & Other Services

- 5.2 By Sector

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.2.1 Office

- 5.2.2.2 Retail

- 5.2.2.3 Industrial and Logistics

- 5.2.2.4 Data Center

- 5.2.2.5 Others - Institutional, Hospitality etc.

- 5.2.3 Infrastructure/Civil

- 5.2.3.1 Transportation Infrastructure (Roadways, Railways, Airways, others)

- 5.2.3.2 Energy & Utilities

- 5.2.3.3 Social Infrastructure

- 5.2.3.4 Others

- 5.3 By Construction Type

- 5.3.1 New Construction

- 5.3.2 Renovation

- 5.4 By Investment Source

- 5.4.1 Public

- 5.4.2 Private

- 5.5 By Key Region

- 5.5.1 Java

- 5.5.2 Sumatra

- 5.5.3 Kalimatam

- 5.5.4 Sulawesi

- 5.5.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AECOM Indonesia

- 6.4.2 Arcadis Indonesia

- 6.4.3 WSP Indonesia

- 6.4.4 Mott MacDonald Indonesia

- 6.4.5 Arup Indonesia

- 6.4.6 Jacobs Indonesia

- 6.4.7 Stantec Indonesia

- 6.4.8 SMEC (Surbana Jurong) Indonesia

- 6.4.9 TYPSA Indonesia

- 6.4.10 PT Wiratman & Associates

- 6.4.11 PT Yodya Karya (Persero) Tbk

- 6.4.12 PT Bina Karya (Persero) Tbk

- 6.4.13 PT Virama Karya (Persero) Tbk

- 6.4.14 PT Indra Karya (Persero) Tbk

- 6.4.15 PT Indicon Consultant

- 6.4.16 PT Rekayasa Engineering

- 6.4.17 PT Saka Energi Consult

- 6.4.18 PT Nindya Karya (Engineering & Consultants)

- 6.4.19 Nippon Koei Indonesia

- 6.4.20 Oriental Consultants Global Indonesia

- 6.4.21 Witteveen+Bos Indonesia

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

8 Appendix